Gareth Rumsey of Experian analyses how economic shifts could impact the loanbooks of UK p2p marketplaces lending to SMEs.

UK

Funding Empire Now Offers Asset Backed Loans

![]()

![]() Funding Empire entered a cooperation with the Business Lending Exchange (BLX) to offer asset backed loans on the marketplace. These new asset backed loan investments will be backed by realisable security and go through BLX’s proven and experienced credit assessment process – they will be available to Funding Empire investors from tomorrow.

Funding Empire entered a cooperation with the Business Lending Exchange (BLX) to offer asset backed loans on the marketplace. These new asset backed loan investments will be backed by realisable security and go through BLX’s proven and experienced credit assessment process – they will be available to Funding Empire investors from tomorrow.

Parag Patel is managing director of Funding Empire, a growing peer-to-peer business lending platform. Announcing the new product, he said: ‘This is the first step in an ambitious plan to deliver a number of different peer-to-peer investment products that we have designed to cater for all kinds of investors and their varying risk profiles. Asset finance offers funding for businesses and is a long established traditional finance product backed by tangible security. In this new model our lenders will receive monthly capital and interest repayments, unlike many other asset backed lending repayment structures that defer payment of capital and sometimes also interest, until the end of the loan term. We have had huge demand for a non-property based, asset backed product that provides monthly income – and we’ve responded to that demand.‘

Loans under this model will be for a maximum of 50,000 GBP over a maximum term of 3 years providing monthly capital and interest repayments to lenders. Loan requests will typically last between 5-7 days and will operate as fixed rate auctions. They will end either when the loan request is filled or it expires. Loan parts from this model can be traded as normal on our secondary loan market. Continue reading

10 Years Zopa

Zopa co-founder and CEO Giles Andrews about the company’s journey.

Source: Zopa blog

Seedrs Review – My Experiences Since Joining

![]()

![]() 15 month ago I joined the British platform Seedrs and started to invest in startups I consider interesting. Since then I have built my small portfolio, holding equity stakes in more than a dozen mostly British companies. In this article I share my experiences in the process.

15 month ago I joined the British platform Seedrs and started to invest in startups I consider interesting. Since then I have built my small portfolio, holding equity stakes in more than a dozen mostly British companies. In this article I share my experiences in the process.

What is it about?

On Seedrs startups can pitch to raise money offering investors an equity stake in the company. This is called p2p equity or equity crowdfunding. The startup discloses information about their product, plans (e.g. intended impact, monetisation strategy, use of proceed) and achievements so far to registered users. There is further information about the market they operate in and the team is presented.

The equity share offered is stated (e.g. 5%). This and the amount to be raised (e.g. 75,000 GBP) define the valuation of the startup that the startup has applied (in this example 1,425,000 pre-money, so post-money, that is after completed funding the startup’s valuation would be 1,500,000 GBP and the 5% equity share of the new investors represent 5% of 1,500,000 = 75,000 GBP raised). Note that the valuation is based solely on what the startup deems appropriate. Of course if the startup aims to high it risks that there is not enough investor demand and the funding fails.

How to get started as an investor?

I just signed up online and submitted some documents to verify my identity. The process is pretty straightforward. Seedrs is open to international investors, so investors do not have to be UK residents.

After signing up, investors can browse the pitches that are currently raising money. A pitch is usually open for 60 days, but maybe closed early by the startup if the goal is reached earlier.

Current screenshot showing some of the open pitches

Clicking on any one of the pitches reveals the detailed information. It also shows who has invested and how much. Investors can opt to show their bid as ‘Anonymous’ in order not to disclose thier name to the Seedrs community. When an investor likes a pitch bidding is possible through the “Invest” button. As long as the pitch is below 100% funding an investor can bid first, and pay later (within 7 days of the pitch completing 100% funding). Once the pitch reaches over 100% it is marked as “overfunding” and investors can only bid, if they have already deposited funds available in their account. Payment is possible via bank transfer or credit card.

What happens after the funding

Seedrs completes all the paperwork with the startup. As Seedrs acts as a nominee for investors the individual investor does not have to do anything. The nominee structure means that the startup does not have to deal with each of the many individual investors but rather only with Seedrs as Seedrs represents all of these investors. Seedrs charges the investors a fee of 7.5% on the profits the investors make (note that this is not a fee on the investment amount (example: an investor invests 200 GBP in a pitch. Should there be an exit later where the value of the investors shares is now 300 GBP then Seedrs charges 7.5% of the 100 GBP profit; therefore the investor would be paid back 292.50 GBP). Note that your investment will be illiquid until the exit; as there are restrictions on selling the shares.![]() Continue reading

Continue reading

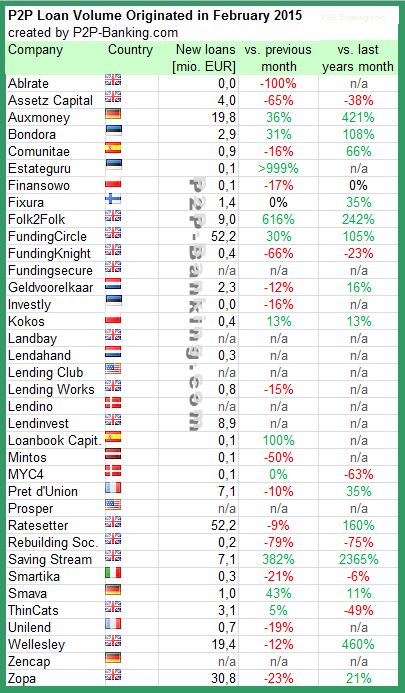

International P2P Lending Services – Loan Volumes February 2015

As February was a shorter month, loan originations fell compared to January with some exceptions. Ratesetter and Funding Circle are in a neck-and-neck race for largest volume figure this month. Prosper and Lending Club no longer publish origination data for the most recent month. I added two more services. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Investors living in markets with no or limited choice of local p2p lending services can check this list of marketplaces open to international investors.

Table: P2P Lending Volumes in February 2015. Source: own research

Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations.

Notice to p2p lending services not listed: Continue reading

Moving Mainstream – The European Alternative Finance Report

The new study ‘Moving Mainstream – The European Alternative Finance Report‘ is available now (free download). The study by the University of Cambridge and EY looks at the development of p2p lending, p2p equity, crowdfunding and other alternative finance offers in Europe and compares it to the development in the UK. The very comprehensive study combined survey results from 205 platforms in 27 European countries with 50 survey responses gathered from UK platforms as part of the Nesta Study.

The new study ‘Moving Mainstream – The European Alternative Finance Report‘ is available now (free download). The study by the University of Cambridge and EY looks at the development of p2p lending, p2p equity, crowdfunding and other alternative finance offers in Europe and compares it to the development in the UK. The very comprehensive study combined survey results from 205 platforms in 27 European countries with 50 survey responses gathered from UK platforms as part of the Nesta Study.

P2P-Banking.com was one of the research partners in this study.

Here are the main findings from the executive summary:

Since the global financial crisis, alternative finance – which includes financial instruments and distributive channels that emerge outside of the traditional financial system – has thrived in the US, the UK and continental Europe. In particular, online alternative finance, from equity-based crowdfunding to peer-to-peer business lending, and from reward-based crowdfunding to debt-based securities, is supplying credit to SMEs, providing venture capital to start-ups, offering more diverse and transparent ways for consumers to invest or borrow money, fostering innovation, generating jobs and funding worthwhile social causes.

Although a number of studies, including those carried out by the University of Cambridge and its research partners, have documented the rise of crowdfunding and peer-to-peer lending in the UK, we actually know very little about the size, growth and diversity of various online platform-based alternative finance markets in key European countries. There is no independent, systematic and reliable research to scientifically benchmark the European alternative finance market, nor to inform policy-makers, brief regulators, update the press and educate the public. It is in this context that the University of Cambridge has partnered with EY and 14 leading national/regional industry associations to collect industry data directly from 255 leading platforms in Europe through a web-based questionnaire, capturing an estimated 85-90% of the European online alternative finance market.

The first pan-European study of its kind, this benchmarking research reveals that the European alternative finance market as a whole grew by 144% last year – from €1,211m in 2013 to €2,957m in 2014. Excluding the UK, the alternative finance market for the rest of Europe increased from €137m in 2012 to €338m in 2013 and reached €620m in 2014, with an average growth rate of 115% over the three years. There are a number of ways to measure performance across the various markets. In terms of total volume by individual countries in 2014, France has the second-largest online alternative finance industry with €154m, following the UK, which is an undisputed leader with a sizeable €2,337m (or £1.78bn). Germany has the third-largest online alternative finance market in Europe overall with €140m, followed by Sweden (€107m), the Netherlands (€78m) and Spain (€62m). However, if ranked on volume per capita, Estonia takes second place in Europe after the UK (€36 per capita), with €22m in total and €16 per capita.

In terms of the alternative finance models, excluding the UK, peer-to-peer consumer lending is the largest market segment in Europe, with €274.62m in 2014; reward-based crowdfunding recorded €120.33m, followed by peer-to-peer business lending (€93.1m) and equity-based crowdfunding (€82.56m). The average growth rates are also high across Europe: peer-to-peer business lending grew by 272% between 2012 and 2014, reward-based crowdfunding grew by 127%, equity-based crowdfunding grew by 116% and peer-to-peer consumer lending grew by 113% in the same period.

Collectively, the European alternative finance market, excluding the UK, is estimated to have provided €385m worth of early-stage, growth and working capital financing to nearly 10,000 European start-ups and SMEs during the last three years, of which €201.43m was funded in 2014 alone. Based on the average growth rates between 2012 and 2014, excluding the UK, the European online alternative finance market is likely to exceed €1,300m in 2015. Including the UK, the overall European alternative industry is on track to grow beyond €7,000m in 2015 if the market fundamentals remain sound and growth continues apace.