Detailed investigations have been undertaken into the Company’s affairs during the period covered by this report, with the assistance of the Joint Administrators’ instructed solicitors Pinsent Masons LLP. The investigations have included carrying out reviews of the Company’s books and records, performing detailed analysis of the Company’s bank statements and reviewing the results of key word searches of the c480,000 Company emails held by the Joint Administrators.

The Joint Administrators have now also carried out interviews with both Liam B.. and Tim G.., the former directors of Lendy. The investigations have been concerned with a number of transactions, most significantly payments of approximately £6.8million that were paid to entities registered in the Marshall Islands for apparent marketing services carried out for Lendy. It is the Administrators’ position, however, that these payments were ultimately for the benefit of Liam B.. and Tim G…

As a result of these investigations, on 1st June 2020 the Joint Administrators made an application to Court for a worldwide freezing injunction to be granted over the assets of Liam B.. and Tim G.., as well as proprietary injunctions on the properties owned by companies linked to the directors, RFP Holdings Limited and LP Alhambra Limited. The Order was granted on the 4 June 2020. Proceedings have now been commenced against Liam B.., Tim G.., RFP Holdings Limited and LP Alhambra Limited. Owing to the nature of these claims, the Joint Administrators are unable to provide further information at this time.

Mintos* will launch a new product offer called Invest & Access tomorrow. It was already unveiled and presented at the P2P Conference in Riga on Friday. Before I write about it watch the video below for about 10 minutes with Mintos CEO Martins Sulte explaining Mintos Invest and Access.

the video should autostart at the right point. If not it is at 2:29:22

The new offer makes it super-easy for investors to invest and automatically diversify through a very wide selection of loans. Mintos does that by investing the money in all loans on the platform that carry a buyback guarantee and are from originators that are at least 6 months on the platform. Mintos promises that investors will be able to cash out easily (subject to market demand) instantly, saying investors don’t need to bother about handling the loan selling on the seondary market. Mintos does that by selling the non-late loans to other investors.

The investor can still see how the portfolio he holds is composed on an overview page. One important aspect for the market dynamics on Mintos marketplace is that Invest & Access will invest before the autoinvests.

Mintos is cleary aiming to make it easy for new investors that don’t want to spend much time thinking about the investment and optmizing yields by giving them the average yield by just one click. The Invest & Acesss page will show the weighted average interest rate, which at the time I saw that page was showed as 11.98%. But the figure will change and update as market conditions fluctate and as the FAQ says it is not guaranteed.

One important point in the FAQ/footnotes is that the ‘instant access’ only applies to current loans. That means if the investors has e.g. 15% late loans, that would mean that he gets only 85% as instant withdrawal and for the remaining 15% has to wait until either the loan is bought back by the buyback or becomes current again (I suppose in that case the investor could trigger another cashout).

Investors can runs both Mintos Invest & Access as well as the existing autoinvests, should they which, but in that case Invest & Access would use any available cash the investor has first, therefore I would guess that there are rarely any funds left for the autoinvests to use.

My Opinion on Mintos Invest and Access

Mintos clearly offers a product that makes it as easy as possible, lowering the entry hurdles especially for new investors. And as Bondora Go&Grow* shows there is a high demand by investors for simplified products. Statistics published by Bondora show that in April 2019 63% of the new investments in that month where conducted via the Go&Grow product, which is constantly gaining over the other investment methods Bondora offers. Other examples are the Access products offered by British Assetz Capital*.

Looking at it from the perspective of an investor that is a little more experienced and willing to spend a little time Invest & Access does not seem an attractive offer. By definition it offers the weighted average interest rate.

By setting up own autoinvests at Mintos, keeping a good diversification and foregoing the highest risk, investors can currently achieve about 13-14% yield on Mintos. So if they would instead use the new product they would have about 2-3% lower yield, and have actually less control on which originators they invest in. An important point to consider, is that the value Mintos shows you, is the average interest rate, NOT the expected average yield. The yield will be significantly lower than the interest rate as Mintos will include buyback loans from originators with long grace periods or originators that do not pay interest income on delayed payment. Excatly those are typically avoided when investors configure their own autoinvests.

And concerning the argument of liquidity. Mintos is very liquid anyway. Without using the new product it is no problem to liquidate a portfolio within a few minutes to a few hours it just depends on the price. Sure you might have to offer a discount. Maybe depending 0.2%-0.6% on average. But that is a small price if you had the higher yields before.

So would I recommend using Invest & Access over the ‘traditional’ way of setting up own autoinvest? There is one use-case I would. If an investor wants to invest very short-time (for whatever reason ‘parking’ money) for less than say 120 days, than it is worth considering.

In my opinion on why Mintos launched the new product, there are actually two reasons:

there is demand for a simplified product and this new product shall satisfy that

the new product will help on the sales site for attracting and onboarding new orignators. Originators that can only offer rates that are below the average interest rate on the Mintos platform so far were hard to sell. With Invest & Access they will be just part of the bundle and automatically sold (once the originator has been on the platform 6 month)

That brings us to an interesting point. How will Mintos Invest & Access the market dynamics? The big factor here is that Mintos Invest & Access happens BEFORE autoinvest and manual investment. There are already (even before launch) speculations and fears of investors that it might bring down interest rates or ‘force’ them to use the new product to avoid cash drag, but I think it is much to early to make any prediction what might be the outcome. But I sure am curious what this will do to the activity on the Mintos marketplace.

What are your opinions on the new product? Please share them in the comments. Thx.

P.S.: The following interview with the Mintos CEO was recorded just before the announcement of the new product, therefore it does not cover Invest and Access – but it has a lot of information on the current state of Mintos.

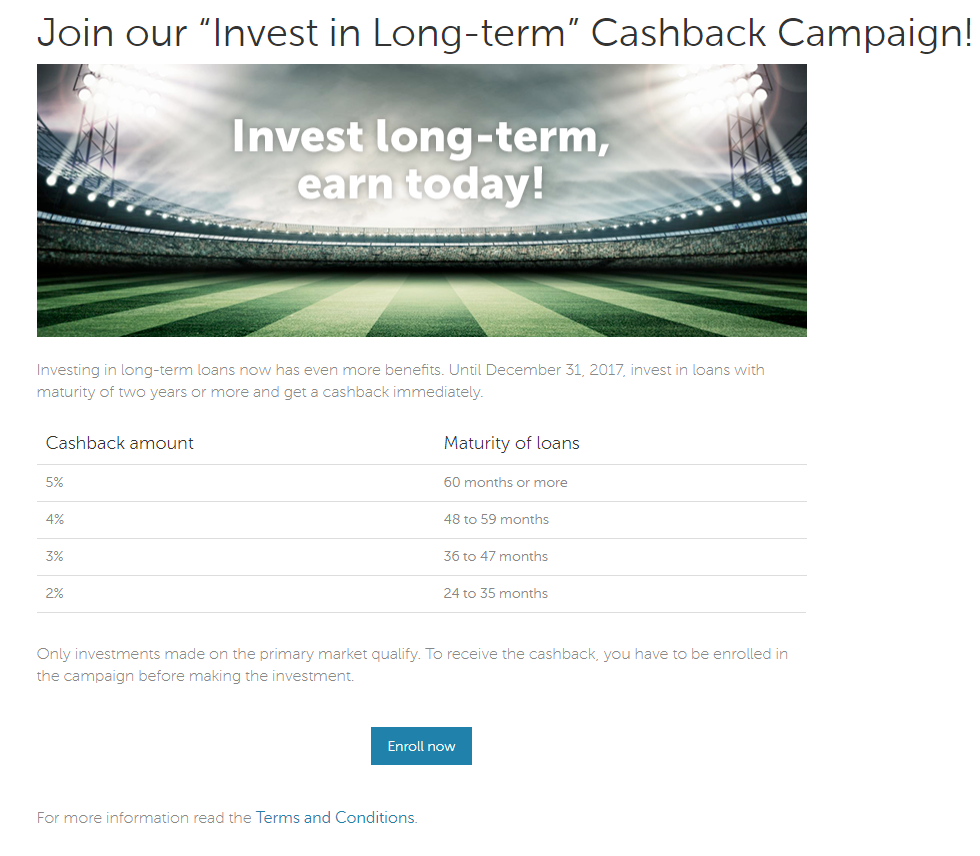

Lativan p2p lending marketplace Mintos just launched a cashback campaign running for the remainder of December. Investors investing in new loans with a term of at least 24 months on the primary market will receive a cashback of 2% to 5% depending on term length. The cashback will be credited within 6 days says Mintos.

This is a big bonus that goes on top of the 12 to 14% interest rate that these longer term loans at Mintos typically carry.

Important: To be eligable an investor needs to enroll once for the campaign by clicking on the promotion banner inside the Mintos dashboard.

New investors can even get an additional 1% cashback on all investments made within the first 90 days of registration (credited monthly) by registering via this link,

Most loans on Mintos are in EUR currency, but other currencies are available, too. Only recently Mintos started listing loans in GBP currency too.

“Investing long-term has many benefits. Loans with a maturity of two years and more on average have higher interest rates. As the maturity of these loans is longer, these higher rates can be locked-in for longer as well, thus avoiding cash drag effect. Also, investing in long-term loans allows for a better diversification, because this way investors can access types of loans and borrowers that have a different profile than the average short-term loan takers. We hope that in combination with our cashback campaign, all of these benefits will help our investors reach their investment goals in a more efficient and rewarding way,†says Martins Sulte, CEO and co-founder of Mintos.

Peer-to-peer lending platform Fellow Finance is now open for borrowers in Germany. Wirecard Bank supports the Finnish FinTech company Fellow Finance to enter and provide a digital infrastructure for the German financial market. Wirecard Bank will place their German full banking license at the Fellow Finance’s disposal and in addition enabling a completely digital credit process.

Under German regulation (KWG) only banks are all allowed to make loans, meaning all p2p lending platforms need to partner with a transaction bank.

It is not a full p2p lending offering as investors cannot invest into the German loans on the platform. And Fellow Finance states in their TOC that they do not advise borrowers regarding the loans. So it looks to be an attempt to capitalize on the reach of the brand. The website for the German market is running on the national domain Fellowfinance.de. Update: While the German website explicitly states that retail investors cannot invest, the wording might be misleading and actually might mean only that investors need to go through the Finnish site in order to invest. On the Finnish site the ability to filter for German consumer loans and to set up allocators (autoinvest) for German loans is present.

Jouni Hintikka, CEO at Fellow Finance, says: “We are looking forward to working with advanced Wirecard Bank as a co-operation partner in the future. We are proud of the entry into the German market after having already proven our business model in Finland and Poland. This is again one step of making Fellow Finance the biggest consumer and business lending platform in Europe and proves the scalability and flexibility of our platform.â€

Thorsten Holten, Executive Vice President Sales Financial Institution and FinTech Europe, adds: “Gaining Fellow Finance as a customer means that we can expand on our collaboration in the area of alternative lending with the aid of an international partner. With our expertise in the areas of banking and regulations, we help FinTech companies such as Fellow Finance to enter the market in the best way possible as well as to quickly and easily internationalise their business.â€

In future, Wirecard Bank will support Fellow Finance in the scoring of potential borrowers and carrying out payment transactions. This means that end consumers in Germany will be able to quickly apply and raise a loan in competitive interest rate.

The German market is very competitive and so far p2p lending marketplaces have found out it is not easy to compete with the banks. In Germany Auxmoney is the largest p2p lending marketplace offering consumer loans.

After months and years of announcements and waiting Funding Circle Germany yesterday published loan book performance figures. Data reported is on all loans since launch on March 30th, 2014 (at that time Zencap) and as of June 30th, 2017. In total there were 920 loans.

Figures:

Total loan origination volume 66,560,800 EURÂ 100% Repaid loan volume 26,859,284 EUR 40.35% Loan volume in default (more than 90 days overdue): 3,988,632 EUR 5.99% Outstanding principal: 35,712,885 EUR 53.65% Total interest paid to investors: 4,578,552 EUR

The outstanding principal of 35,712,885 EUR (100%) is further categorized: Current: 33,293,583 EUR 93.23% Loans that are less than 30 days overdue: 1,664,005 EUR 4,66% Loans that are 30 to 60 days overdue: 421,902 EUR 1.18% Loans that are 60 to 90 days overdue: 333,394 EUR 0.93%

Average weighted interest rate: 8.41%

I would have linked to the source here, but Funding Circle pulled the figures within hours after publication and the page now returns a 404 error (I did save a screen shot before they were pulled). I reached out via email to Funding Circle asking for the reasons, but have not received a reply up to the point of publication of this article. Update: I received a reply from Funding Circle stating that the figures were not correct and did not match Funding Circle’s global reporting format. An example given was that payments made by defaulted loans were omitted. Funding Circle strives to publish the corrected figures asap. 2nd update July 13th: Funding Circle has now published updated figures in changes format. They are online here.

Phrasing it differently one could say that 9.6% (6,4M/66,6) of all issued loans are currently overdue or in default.

In my view the figures give a very bleak – but correct picture of the state of Funding Circle Germany’s loan book. Overdue and default figures are high. With nearly 6% of the loan amount in default and more than another 6% of the remaining loans overdue, there is a very high probability that many investors will incur (after tax) losses. Usually German investors cannot offset default losses against interest earned.

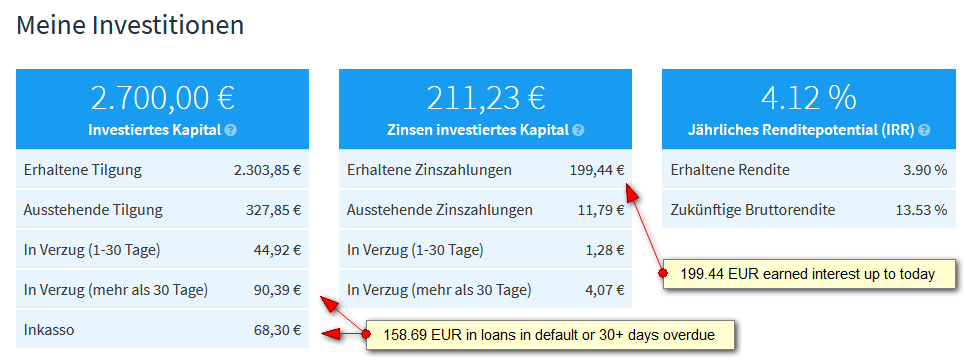

My portfolio

I invested into 27 loans with 100 EUR each (the minimum bid). I stopped investing already in February 2015, after only 10 month, when it became clear to me that Funding Circle Germany had higher overdue figures than expected. However as there is no secondary market at Funding Circle Germany I was stuck with the loans until maturity.

Of my 27 loans the status today is: – 22 repaid – 4 overdue (2 of them for 256 days !) – 1 default (in collection)

I already received back 2,303 EUR of the principal, so there is only about 15% of my investment amount still outstanding. I might get away with a return around zero, as my defaults + overdues are still lower than the interest paid, but it will be close as I have to pay taxes on the full interest earned regardless of defaults. My dashboard still claims 4.12% yield for my portfolio, which does not reflect reality as I see it. The only chance for that to happen would be full recovery of defaults and overdues, which is an unlikely scenario.

My own portfolio at Funding Circle Germany

Investor sentiment towards Funding Circle Germany seems to have turned mostly negative to sarcastic in the past two years if you look at the massive critic on the Funding Circle forum at P2P-Kredite.com. Funding Circle Germany no longer publishes statistics regularly on new monthly loan volumes.

On the majority of p2p lending marketplaces that accept non-resident international investors, the necessary process to comply with ‘Know Your Customer’ (KYC) rules involves multiple manual steps both on the side of the investor and on the side of the marketplace. After filling in details in forms the investor typically needs to submit scans (or photos) of an ID or a passport. As an investor I balk at the very few marketplaces that ask me to submit these via unsecured email. The better ones offer an upload inside the SSL secured website after login. The British marketplace typically also require a recent utility bill to confirm address.

Video ident

In continental Europe a few marketplaces are doing video ident. Recently when I registered at Paskoluklubas, aside from entering details in forms I needed to schedule a Skype video call in which I answered several questions and had to show my ID live. While it was straightforward, it is not more time efficient (both for investor and for marketplace). And I was lost for words for a split second when asked for my zodiac. How many non-native-english speakers can answer that question without hesitating for the right word (luckily mine is easy to translate). So there may be a higher drop off in conversion than in the document upload version.

I learned from Paskolulubas that they used video ident not to optimize the process but rather to fulfill Lithuanian regulation requirements: ‘In the end of last year in Lithuania … [a law was passed] which legalized digital identification …. There are just two legal methods to identify clients through digital technologies. The first one is to use special programs, applications or other measures to ensure that the photos execution process is continuous and that the photos transfer in non-real time would be impossible. The second one is video identification when [the] company directly could record customer and his ID document. We chose … [the latter] method because of the following reasons: a. easier control of quality with in house team and b. faster start’.

So Paskolulubas uses inhouse staff to conduct the video ident process.

Outsourcing KYC

In Germany video ident is also an allowed method of identification. And it slowly replaces the traditional Postident process, a longtime German proprietary solution, since it avoids media discontinuity. But usually the video ident process, while integrated in the website is outsourced to a specialized service provider.

Another example of outsoucing is the process Lenndy uses. When registering, all an investor is asked by Lenndy is his email address, nothing else. Then the investor is required to link an Paysera account with at least level 3. Either an existing one or a newly setup one. Paysera is a E-money institution with over 5 million customers. Lendy then imports the customer data, which have been verified by Paysera with the consent of the the customer. While this solution is elegant for Lenndy, Paysera receives mixed reviews by several German investors in p2p lending. But as the search for ‘Paysera’ in the last link shows, actually several p2p lending platforms use Paysera processes to some degree.

All of the above still require mainly manual labor for checking, even if some of the work is outsourced.

Automating KYC for international investors

Last week British Relendex moved from a manual document upload process to an automated process for investors of 7 countries; Australia, Canada, Denmark, Germany, Sweden, Switzerland. Relendex uses the Call Validate solution and checks (in case of Germany) first , middle, last name, gender, phone, address, city and postal code with the data coming from three different data sources and which Relendex says has high match accuracy. Relendex’s criteria was that the data available should be of equal quality and accuracy to that of the UK database.

A Relendex representative told P2P-Banking: ‘With the new process, international lenders from the nine countries could see their account be approved in a matter of minutes. Where previous manual checking could take a couple of days, the automated KYC process is much more efficient.’

Of course there are other solutions. I reached out to other companies for comment. But those who have automated are tight-lipped about details citing proprietary technology and competitive advantages.

Marketplaces that also use automation are welcome to comment and add to this story.