The P2P platform Mintos* has significantly expanded its product range today. Over 1,000 ETFs from well-known fund providers—such as iShares, Vanguard, VanEck, UBS, and others—are now available for trading. The highlight here is that there are no transaction or custody fees. The only costs involved are the management fees (TER/Total Expense Ratio) inherent to the ETFs themselves. Additionally, fractional shares can be traded, as investments start from as little as 1 Euro. When I checked, Tradegate was displayed as the trading venue, meaning prices and spreads are competitive.

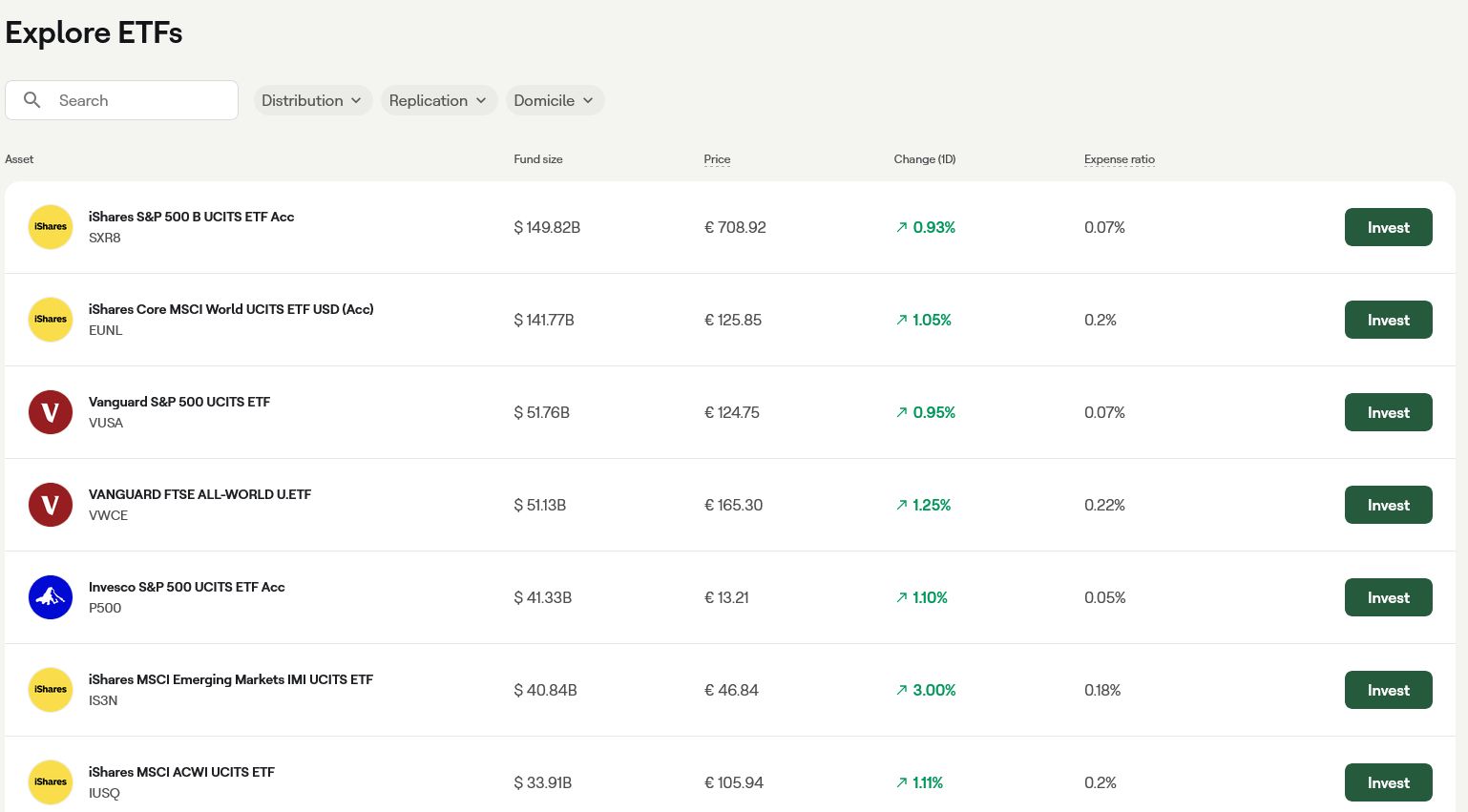

To get started, investors select an ETF from the available list. It looks like this:

click to enlarge

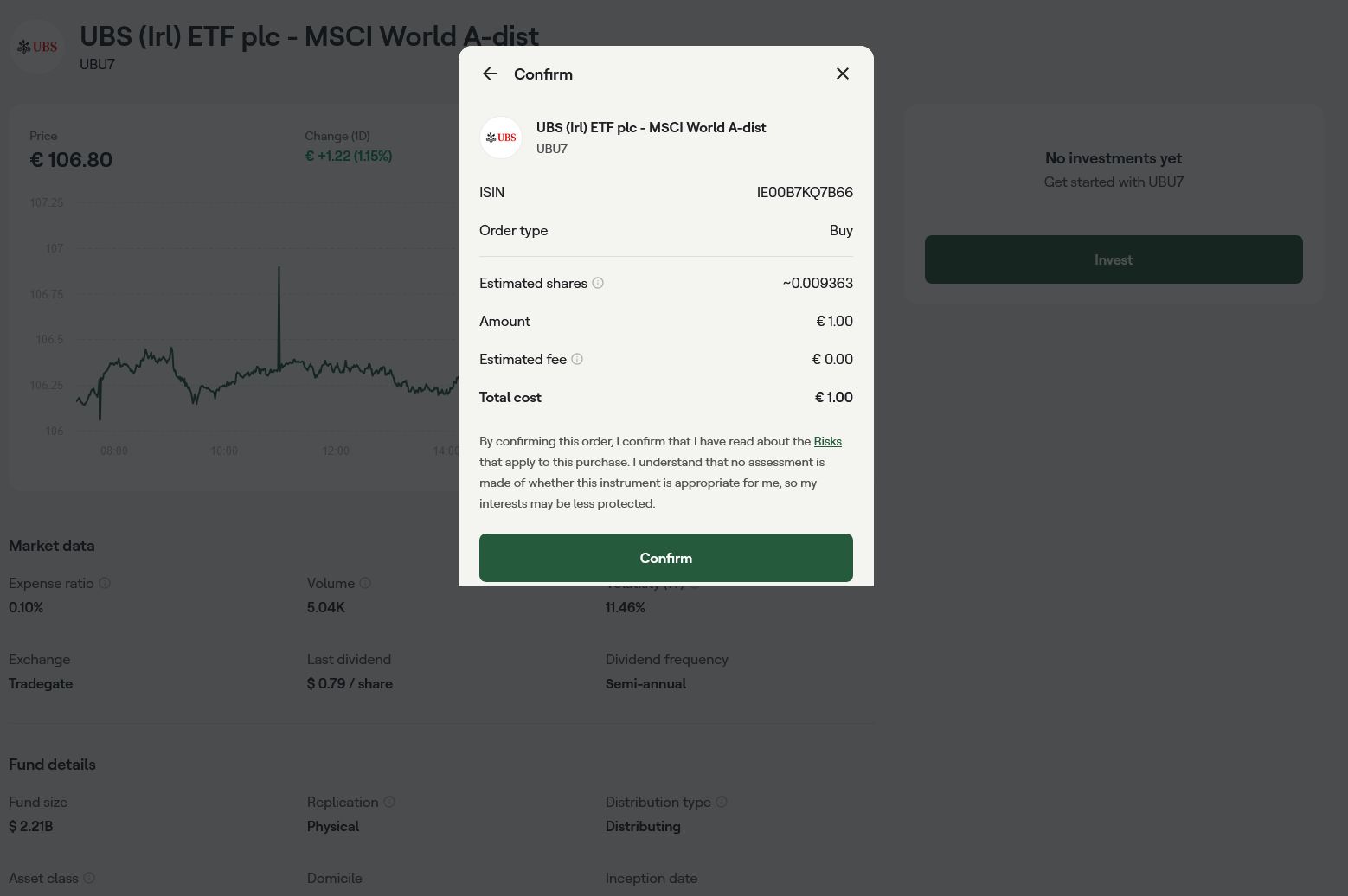

Once an investor has chosen an ETF, they simply click “Invest”, enter an amount, and proceed to this screen (example):

click to enlarge

What do you think of this new offering? Is this the ultimate challenge to neobrokers?

Risk warning: Investing involves risk; you may lose your invested capital. Each ETF carries its own annual fee (Total Expense Ratio) charged by the ETF provider, built into the ETF price. Past performance is not a guarantee of future results.