At registration put WEALTH into the promo code field (was pre-filled when I looked).

Between August 28th and September 30th invest in notes, bonds, property and/or ETFs. The amount you invested on September 30th determines the size of the bonus (see table below).

The money has to stay invested until Dec 31st 2025.

Bonus will be paid out on January 10th, 2026

Full bonus terms are linked on the Mintos* website.

This translates to up to 2% cashback bonus in 4 months time.

I started investing over 10 years ago at Mintos* in January 2015. I am very satisfied with the results I achieved since. You can read all my previous Mintos articles on this blog.

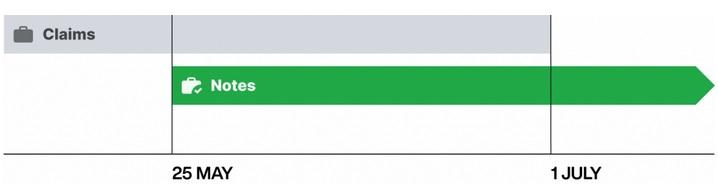

The long announced and several times postponed Mintos Notes product will finally launch on May 25th, Mintos* said yesterday. The notes are financial instruments and issued under the new investment firm license Mintos received last year. For each loan originator there will be a seperate prospectus (see example). Mintos mentions safeguarding of investor funds and notes under MIFID II requirements and increased transparency as investor benefits.

Until 30 June, investors can buy and sell investments via claims on the Secondary Market as usual. Then, from 1 July onwards, investors will be able to buy and sell Notes only, as a result of regulatory requirements.

The transition will mean two key changes for investors:

As the claims cannot be traded from July 1st onwards on the secondary market, investors will have to hold any claims in their portfolio to maturity

Mintos is required to deduct withholding tax depending on the investors country of tax residency and applicable double taxation treaties

My take

The transition will mean a major change for the marketplace that could either stiffle or empower Mintos growth. I expect that many investors will shy away from investing in very long term claims on the primary market in the remaining 7 weeks. Also buyer demand on the secondary market will likely decrease for the claims on long term loans. Potentially this will lead to offers with rising discounts before the trading of claims ends on June 30th.

There is some hesitation voiced among investors regarding the upcoming notes due to the withholding tax and surronding paperwork to claim possible reliefs and reductions (Mintos has announced that it will publish more information on the details). Mintos might try to offer some incentives in order for investors to take the leap and embrace the new product. I also imagine that Mintos will step up investor marketing again, once the notes product has launched. Already Mintos is taking a lot of effort to communicate and explain the coming changes via blog articles and newsletters.

This disruption might also increase the trend of loan originators setting up their own, unregulated investor marketplaces in other jurisdictions than Latvia.

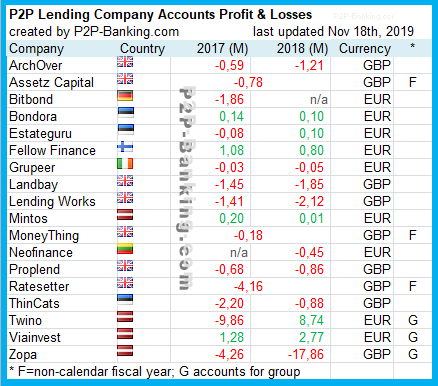

I added a new information page to P2P-Banking compiling data on which p2p lending marketplaces made a profit or a loss in the last business years. You can read more on why this data is useful to investors on the platforms here.

Snapshot of the table at the start of the data collection:

Table: Profits/losses of p2p lending companies (in million currency units) Source: own research.

The table will be updated and added to on this infomation page in future. P.S.: Thx to the crowd for emailing me additional data. Only a few hours after first publication I was already able to add more companies and data so the table on the information page is already more comprehensive than the outdate first version of the publication shown above.

One important aspect for p2p lending investors is tax. In this blog whenever I talked about yields achieved, it is usually pre-tax yield. That is because taxation varies significantly from country to country. In most cases the place of residency of the investor determines the tax regime applicable. There are a few exceptions, e.g. on very few marketplaces withholding taxes are applied.

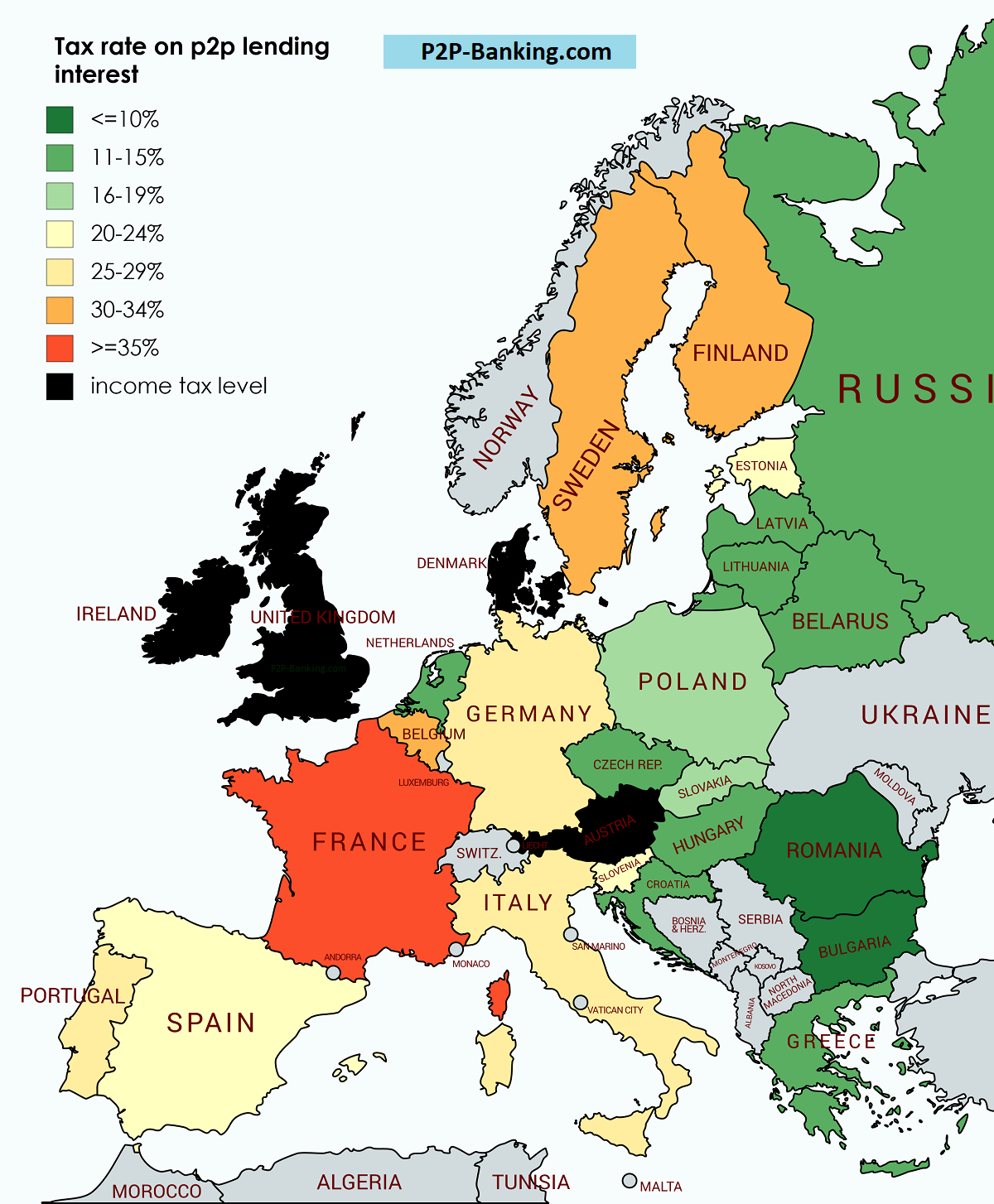

But I wanted to give a viusal overview on how different tax rates are for p2p lending investors, depending on where they live in Europe. Therefore I created for following map.

For overview purposes only. Source: own research – may contain errors or be outdated. Please note that this is a simplification and will not cover many cases. Do not make any decisions based on this, but rather consult a qualified tax advisor

In the countries colored in black the income tax rate is applied on interest earned on p2p lending investments. That means the individual rate of taxation depends on the other and overall income of the investor. For example in the UK the tax bands are 20%, 40% and 45% dependent on overall income. In Ireland tax bands are 20% and 40%.

But in most other countries there is a fixed rate applicable for interest earned on p2p lending. Tax free allowance up to a certain amount may apply. For example in Germany taxation (Kapitalertragssteuer)Â is 26.375% (a little higher if church tax applies).

Taxation is complex. Futher important points are whether defaults and fees can be offseted against interests earned. Also capital gains (e.g. from selling loans with a premium on a secondary market) may be taxed different than income.

Advantageous tax rules

There are many special tax rules and tax breaks. Consult a qualified tax advisor for information on your situation. Here are just some interesting examples.

UK: UK residents can invest through so called ISA products. There is a special IFISA (Innovate Finance ISA) which can be used to invest up to 20,000 GBP tax-free on peer to peer marketplaces. More information and an IFISA comparison is here. The interesting point is that the allowance is available per year. That means an investor using it in 10 consecutive years can invest 200,000 GBP tax-free into p2p lending.

Estonia: Many Estonians lend through a limited company (OÜ) they have set up. The advantage there is , that as long as the earnings stay in the company they are not taxed. Only at the time the profits are paid out from the company to the investor they are taxed at 20%. This allows investors to postpone the taxation for a long time.

Netherlands: The Netherlands are the only country in Europe where the tax is not based on actual p2p lending earnings, but rather fictual earnings. Wait. What? The tax system is actually a wealth tax, and the tax declaration is not based on income but wealth. The tax authority then assumes you earned a fictual income of 4% on your wealth. Tax rates used to be 30% on that (so 1.2% on your wealth; since 2017 it is now 0.581 to 1.68% dependant on amount of wealth). Now if you actually earned 10% ROI with your p2p lending your effective tax rate calculated on that would be 12% (30%*4%/10%). That’s what I used for simplification purposes in the map.

Portugal: In Portugal the rate is 28%. But if a foreign resident moves to Portugal and earns interest only from p2p lending market places abroad, he can profit from a 0% tax rate on these (providing the originating country does not tax the interest) for 10 years. Mark explains his personal experiences with this on obviousinvestor.com. There are non-resident/non-domiciled rules in other Euopean countries but they usually sound more complicated/restrictive.

Hint to platforms: It may be efficient to target countries in your marketing that have a high GDP but also a low or medium tax rate on p2p earnings.

BDO has prepared and emailed the Joint Adminstrators’ Proposal to investors and creditors of the Collateral Companies last night. The report is also available publicly on the BDO website. I have read the whole report. I will not attempt to summarize it, but point out some findings that I find personally really surprising given that Collateral was an operation that managed millions of pounds of client money.

From the outset of the Administrations, we identified that securing the Companies’ electronic records would be critical. Following our initial meeting, the directors advised that all of the Companies’ IT functions and services were outsourced to an IT consultant. Both the directors and … advised that they had no access to the electronic platform, nor any back-up of the data contained within it, and they advised that the electronic platform had been decommissioned during March 2018 due to non-payment of outstanding bills; they did not therefore consider that the Joint Administrators would be able to recover the platform or the underlying data

The company outsourced IT operations, but kept no copies or backups of the data stored. Wow.

BDO did not give up on this, but located the servers and data forensics are working on recovering (part) of the data.

We have since made contact with the third party company holding the servers. Again, following protracted correspondence and with the assistance of our lawyers and my firm’s Forensic Technology team, we have located and secured the actual servers previously used by the Companies. There appears to be a significant volume of data still held on those servers and, as at the date of these proposals, we have taken steps to consolidate the contents of the different servers containing the Companies’ data into a single location (whilst preserving the originals intact). We shortly expect to receive a copy of the data, which we will then interrogate and review to better understand the nature of the data that has been recovered. Whilst it is not yet clear whether we have retrieved all of the Companies’ electronic data, nor whether it will be possible to restore the electronic platform, the Joint Administrators consider that this represents positive progress.

Given that the allocation of client money to loans and the bookkeeping is a primary tasks of a p2p lending marketplace I am appalled when I read this finding:

… also provided certain key information in relation to the investors and loan book, in the form of two spreadsheets (which I refer to below) and copies of email correspondence between his office and various stakeholders during the period in which he purported to act as administrator. …advised that he held no other books or records, and neither did he have any access to the Companies’ electronic platform, or the data contained within it.

Really? The data was held in two spreadsheets? Excel, maybe?

A last quote (highlighting is mine)

Members of the Joint Administrators’ team attended the Companies’ trading address in Manchester on the afternoon of their appointment. The address is a serviced office space, and the office provider advised that the Companies had vacated the office several months prior to the Joint Administrators’ appointment. There were no assets or books and records remaining at the premises.

Now to the good news. BDO confirmed there is money in the client and office accounts. And the report shows the directors are cooperating with the administrator. The report seems to classify investor’s money as trust assets which would, as I understand it, leave investors in a much better position, than the outcome would have been, if they would have been qualified as pure unsecured creditors.

BDO says it is too early to give a forecast to the outcome, given the circumstances, but asseses:

We would, however, note that, as summarised on the statement of estimated financial position attached at Appendix 2, the estimated claims of creditors exceed the book value of the assets held by the Companies (including trust assets). Therefore, even before taking account of any potential asset write-downs and the costs of the Administrations, it appears likely that not all investors and creditors will recover their entire exposure to the Companies and the Collateral lending platform.

A lot will depend on how much can be retrieved from the outstanding property loans, which will fall due by mid-November 2018 at latest.

There is a lot of investor discussion regarding the report on the P2pindependentforum.

Trying to look at this from a high vantage point:

In my opinion a lot of the work, time and fees of BDO would have been saved, if the data would have been stored more persistently by Collateral in the first place

Investors should try to keep some form of offline records. I know depending on platform and number of loans that might be hard and laborous to do, but look at what position the Collateral investors are in now. It is uncertain though if those investors that do have precise records on their loan allocation will be in any way better off than those that do not in the Collateral case

Investors trust regarding operations stability and bookkeeping of smaller UK platforms (Collateral had 5 employees) may be dealt a blow. It might become more important for smaller UK marketplaces to demonstrate robustness and durability of operations (e.g. through a detailed and transparent documentation of the living will, which is required for fully authorised platforms anyway)

The next steps in the Collateral case are described in the proposals in 15.1. and 15.2 of the report (page 20).

Banco BNI Europa was launched in July 2014 as a digital-only bank in Portugal. Banco BNI Europa says it aims to challenge the traditional banking sector through strategic partnerships with fast-moving fintech businesses to launch new products allowing the use of the most advanced technology in terms of risk analysis, consumer experience and rapid entry into the market.

Today Banco BNI Europe announced it will start lending on Fellow Finance.

‘Modern banks expand and grow by partnerships. Fellow Finance enables and offers an easy access to invest and lend in Nordic and Central European consumer and SME loans through its platform. Through their investment account at Fellow Finance, Banco BNI Europa is able to diversify their balance sheet investment into Finnish and German loans easily and cost-effectively. This is an example that banks don’t need to set up their own expensive operations on ground but can effectively enter markets through marketplace lending platforms. It is also an example how banks can also utilize the presence of FinTech among their core business’ says Jouni Hintikka, the CEO of Fellow Finance.

‘Investing via Fellow Finance in consumer and SME loans offers us a great opportunity to easily expand our operations and we are very satisfied with the analytical and professional approach of Fellow Finance in credit intermediation’ echoes Pedro Pinto Coelho, Executive Chairman of Banco BNI Europa.

Last week BNI Europe announced it will fund German SME loans through Funding Circle. According to Pedro Pinto Coelho, Executive Chairman of Banco BNI Europa, ‘an investment in German SME – the staple of European economic stability – is a highly attractive asset class. And Funding Circle is the professional partner that convinced us with their risk assessment and credit analysis. …’.

To date Banco BNI Europa has struck fourteen fintech partnerships with European fintech leaders across the continent. The bank had 141 per cent growth by the end of 2017 taking its total assets above €500m, and cited its focus on ‘innovative products’ as an explanation for the improved performance.