If you read any other article on the this blog typically one aspect is how to gauge the risk, that the loans I invest into will default and how to minimize this risk by diversification or other measures. Today I will write about a new platform, where I specifically target non-performing mortgage loans in Spain as basis of my investment. At Indemo* I invest in notes, which are a discounted debt investment (DDI) consisting of 8 underlying non-performing loans.![]()

This is the way it works: DDIs are built on the basis of underlying mortage loans, where the borrower has defaulted and the bank, which was the original lender, has decided to sell the debt at a discount in order to get it off their books.This debt was then bought by a servicer, which can refinance by offering linked notes on the Indemo* platform.

The servicer can act more agile than the bank and has several options to collect on the debt:

- Or the debtor passes the keys of the property to the the servicer, and the servicer releases the debtor from part of the excessive debt and then then sells the real estate on te market. Another option is that the debtor or the servicer finds the buyer for the property, sells the property and the debtor is partly released from the excessive debt. All properties on Indemo mostly are secondary residences.

- The target collection scenario for the servicing company is to settle the debt pre-court. If that strategy fails, it can file for a court claim and thereafter have the property auctioned

Example of a note I have invested into (click on it to enlarge)

Each note consists of 8 different properties in Spain.

The objects list view shows:

- Appraisal: the value of the underlying asset appraised by an independent company

- PTV (price to value): PTV is calculated by dividing the price paid for the discounted debt by investors by the value of the property. E.g. in the second property 41%. The appraisal value is 429,404 EUR. The debt was bought for 177.000 EUR.

- Term (M): Expected term in months

- ‘Exp. Return’: Expected annual return rate based on a moderate scenario, where 90% of the debt is settled within 18 months

- Status: current status

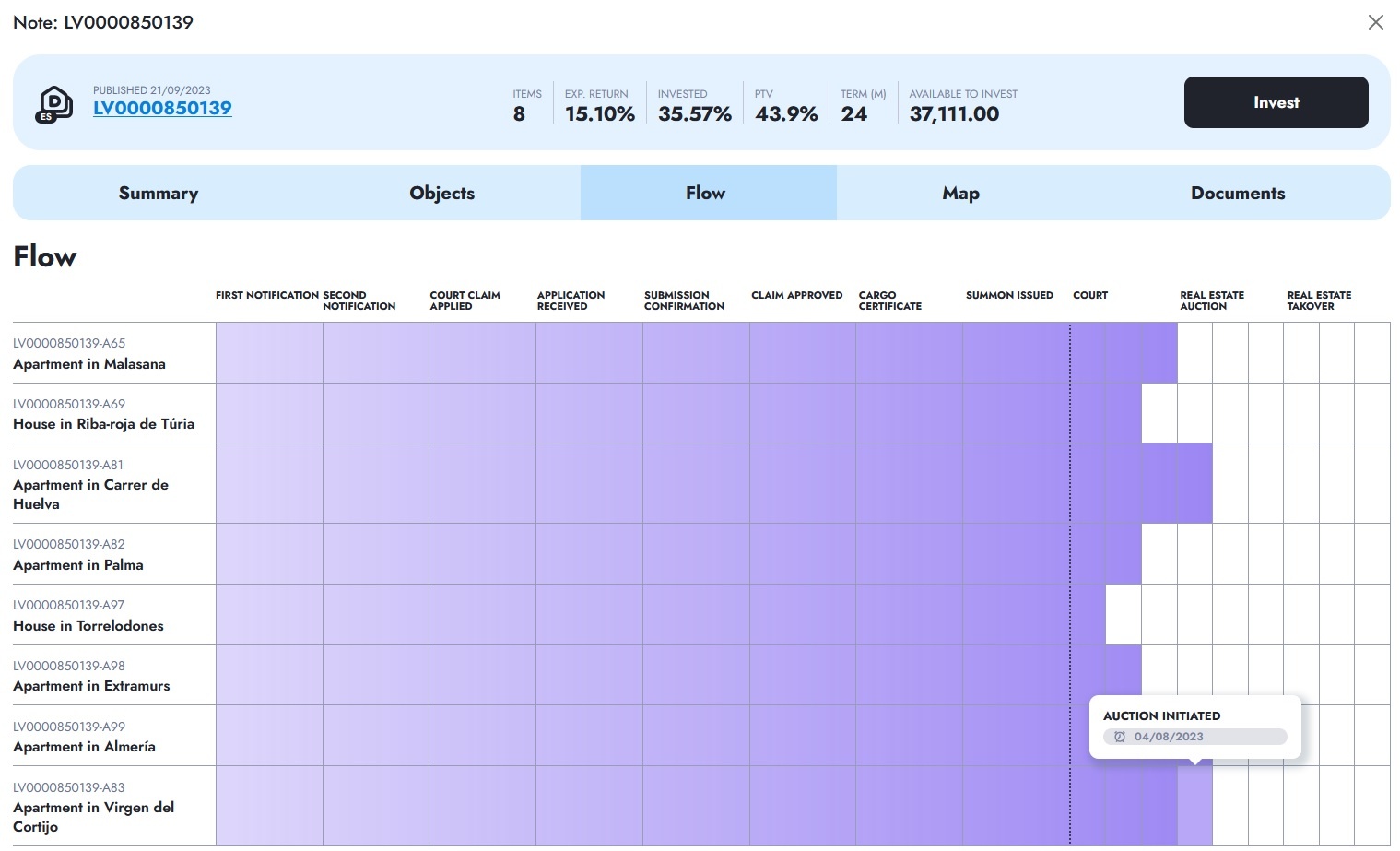

Flow view, showing the status progress of each loan in the note (click on it to enlarge)

It is important to understand, that an investment in a DDI note on Indemo* does not produce a constant cashflow for the investor. Once each attached property is sold for its market value, the investor receives a 50% profit share from the differential between the discounted price paid for the debt and the proceeds from the sale of the property. Usually, the average discount for objects placed on Indemo platform is around 40%. The investor gets repayment of the part of the investment amount and profit allocation once each and any debt in the basket of eight debts is recovered. In the flow chart pictured above the progress of each loan is shown.

Furthermore it should be clear, that this is a high risk investment and the the projected attrative yield of 15.1% might actually turn out higher, lower or even produce a loss. More on the sceanrios that are base for the calculation of the projected return can be found on the Indemo website.

The Indemo product offers

- a novelty factor – discounted debt investments are not typically available to retail investors as a product

- an interesting return/risk ratio. Considering the high discounts the debts are acquired for, there seems to be enough buffer even in challenging market environment conditions on the property market

I had the opportunity to discuss the pros and cons of the product on several occasions with the Indemo management team. I visited them in their office in Riga in May.

Indemo is fully regulated and licensed by the Latvian regulator. Indemo has so-called passports as an investment services company in several European countries, and is also member of the European Union investor compensation plan up to 20K EUR per investor (note this is against Indemo failure, not against loss of investment, read the specifics). Debt servicing and collection is performed by a professional servicing company authorised by the Bank of Spain according to Law 5/2019, of March 15, regulating real estate lending entities.

Investor signup on the Indemo* platform is pretty straightforward. First an identity verification by Veriff, thereafter answering several questions to determine product suitability. After that is completed the investor can deposit funds and invest. Indemo does not charge the investors any fees.