Two years ago I started investing on Inrento*. On the Inrento* platform investors select property loans secured by a first rank mortgage. Typical interest rates are around 9-10% with loan terms between 12 and 36 months. Inrento has a strong track record with zero late projects, 78 million EUR lent and around 4200 active investors. The home market of Inrento* is Lithuania, where it is fully regulated and most projects are located – the platform also featured projects in Poland, Latvia and occasionally other countries.

Sample Inrento project photo – click to enlarge

There are detailled project descriptions and regular updates. The minimum investment per project is 500 EUR.

good service (recently something did not go according to plan and a project I invested in was cancelled because the mortgage wasnot signed within the projected 20 days maximum. Inrento* paid all affected investors 0.35% cashback as compensation)

interest is paid monthly

fully regulated

On the downside there is

few new projects (about 1-3 per month), resulting in cash drag

new projects are often filled within hours after coming online

15% withholding tax applied; can be reduced and possibly offseted in tax declarations depending on the rules of the home country of the investor

no auto invest

Profit graph from my Inrento dashboard

Yield calculation from third party tool p2pdash – click to enlarge; shown figures are a little too low as the do not count secondary sales correctly

After roughly two years my yield is a little under 10% per annum. I can say only good things about Inrento*. The main gripe is the cash drag which is the result of the growing popularity of Inrento* among investors.

Other property platforms

Asterra Estate* is a property platform dedicated for a development project of a Latvian village. Loans are high interest around 15%. Minimum investment is 1000 EUR per loan. Interest is credited daily. Early exit feature available. Currently 4-7% cashback if you sign up via this Asterra Estate* link.

Devon* is a property platform with loans backed on Latvian property. Loan rates are around 10-15%. Minimum investment is 1000 EUR per loan. Interest is credited daily. Early exit feature available. 1% cashback (plus 4%-5.5% cashback during current spring campaign, depending on your investment level), if you sign up via this Devon* link

Estateguru* is a fully regulated Estonian platform, featuring loans secured by properties mainly across the Baltics and Finland. Minimum investment is 50 EUR per loan. Secondary market available.

New property platform Devon* features investment in high interest mezzanine loans for Latvian properties. Launched by MJL Enterprise Group which claims 30 years of experience on the market, it will be used by the group to finance own property development projects. Previously the group used other platforms, including Estateguru, Profitus or Crowdestate but now has moved the financing inhouse under its own control. The mezzanine loans rank behind senior debt, which explains the high interest rates of up to 15%.

Currently there are 3 properties available on the platform:

The minimum investment amount is 1000 EUR.

The loan terms end Dec. 2026, Dec. 2027 and Dec. 2025 respectively. While there is no secondary market, Devon features an early exit option where lenders can exit early if another investor is willing to buy the loan investment at par value. For this feature Devon clearly modelled itself on Ventus Energy*.

The interest is credited daily and it can be set either to compound or to payout. With the latter it can be withdrawn once the minimum payout threshold of 10 EUR is reached.

Currently (for investments until May 31st) Devon* offers a generous early bid cashback of 3% which will instantly be invested in the same property. On top of that investor receive 1% cashback on all investments in the first 60 days after signing up via this Devon* link.

The Devon platform has no fees for investors. The unregulated Devon OÜ platform company is registered in Estonia, therefore no withholding taxes are applied on investor interest payouts.

Since last August I am investing on the Indemo* platform. In an earlier article I described in detail how Indemo works and why it was attractive to me. It has been going well so far. My portolio consist of 15 properties in 13 notes. Two further properties have already been successfully sold, yielding profits to investors including me that were well above the originally projected yield of 15.1% p.a.

Last week property A26 was sold, which gave me returns ranging from 15.9% to 24.2% (second column in the screenshot). The different yield numbers rsulting from the same property sale are due to the various different investment dates ranging from November 23rd to April 23rd (first column in grey). In this case the property was sold after only 7 month of being first listed on the platform meaning the success was achieved much quicker than the expected stated term of 24 month.

Click on screenshot for enlarged view

On the previous sale I had even higher yields ranging from 32% to 57% p.a.

Indemo Cashback Bonus

Starting today, Indemo* is offering new investors, that sign up via this Indemo* link 3% cashback on investments. Important: To get the cashback the new investor needs to enter the Indemo promo code “CASHBACK” (without the quotation marks) in the dedicated field during registration. Existing investors get 2% cashback. The cashback will be applied on all investments till July, 31st 2024. The cashback amount is credited instantly. I just invested 800 Euro in a note and as existing customer got credited 16 Euro.

Screenshot: This is how to enter the Indemo Promo Code CASHBACK at registration

Screenshot: I got my cashback for my 800 EUR invest credited instantly

added multiple new features on the website, including a dashboard and analytics section, better account statements, and better information on the object composition in new notes. I observed that Indemo is really aiming to implement features requested by investors to make the user experience better for the investors.

crossed 1,000 registered investors mark

announced 2 million EUR assets under management, saying that growth accelerated compared to reaching the first million EUR

added 3 new objects that are part of new notes offered

Screenshot: one of the recently added properties: an appartment in Barcelona

Most of the properties on the Indemo* platform are in towns on the Mediterranean coast.

‘Earn rental income starting from €50 investment’. As of today, Mintos* is advertising a new offer that it describes as passive property investing.

In fact, investors are investing in Real Estate Securities, which are an interest-bearing debt security backed by underlying bonds. Purchasing Real Estate Securities entitles the investor to receive interest payments for the Notes whenever net property payments are made on the underlying bonds and repayments when the underlying property is being sold.

So to summarise: If everything goes according to plan there is a monthly interest payment, which is fed from the rent, and at the end a payment for the increase in value, which is estimated but not guaranteed.

The underlying properties are located in Austria and come from the Bambus.io portfolio, which acquired them as part of a partial purchase. The older owners are therefore still living in their homes and are now paying rent for the sold portion (kind of a reverse mortage).

Illustration: The first property offer in the new Mintos product as an example (click for larger view)

Advantages for the investor:

Good opportunity for diversification

These are rented residential properties (and not projects of property developers or commercial properties as with some other platform offers)

Invest from as little as 50 euros

Regulated offer

Disadvantages for the investor:

Very long term (20 years in the example)

rather illiquid (although a sale via the secondary market is possible, it is questionable whether there will be demand)

No information on how the valuation was carried out and how the increase in value was forecast

The property from the first offer was valued at 317,500 euros. Mintos* does not provide any further details. Brief research (e.g. here) shows that the valuation of 2,500 euros/m² is not overpriced. According to the Bambus FAQ, the market value of the partial purchase carried out by Bambus is determined by an independent expert. It can be assumed that the market value determined in this way corresponds to the property value stated on Mintos.

Unfortunately, there are no further details on how the increase in value was forecasted. According to the prospectus, Bambus, which has been operating since 2022, has not yet sold any properties. So there is no experience yet.

Is it worth it? My first impression

In my opinion, the interest rate offered is too low for the very long investment period. It is difficult for me to judge whether the increase in value has been realistically forecasted. After all, it could probably be enough to cover inflation.

Comparison with other investments

The question remains, why should investors use the Mintos* offer instead of alternative offers? I have started to build up a portfolio with Inrento* in the last few weeks. The property loans there offer a significantly higher interest rate of 8-9% p.a., interest payments are also monthly and there is also a payment for appreciation (1.5% p.a.). The advantage is the significantly shorter terms of 1 to 3 years.

Estateguru* also offers significantly higher interest rates of 9-11%. There is also a bonus of up to 2% on top for larger investment amounts. The terms are also often shorter at 12 to 18 months. Even taking into account the usual overdrafts of around one year, the investor is much more liquid than with the Mintos product.

Furthermore there are exchange-traded REITs as an alternative. These are much more liquid and enable broad diversification.

If you read any other article on the this blog typically one aspect is how to gauge the risk, that the loans I invest into will default and how to minimize this risk by diversification or other measures. Today I will write about a new platform, where I specifically target non-performing mortgage loans in Spain as basis of my investment. At Indemo* I invest in notes, which are a discounted debt investment (DDI) consisting of 8 underlying non-performing loans.

This is the way it works: DDIs are built on the basis of underlying mortage loans, where the borrower has defaulted and the bank, which was the original lender, has decided to sell the debt at a discount in order to get it off their books.This debt was then bought by a servicer, which can refinance by offering linked notes on the Indemo* platform.

The servicer can act more agile than the bank and has several options to collect on the debt:

Or the debtor passes the keys of the property to the the servicer, and the servicer releases the debtor from part of the excessive debt and then then sells the real estate on te market. Another option is that the debtor or the servicer finds the buyer for the property, sells the property and the debtor is partly released from the excessive debt. All properties on Indemo mostly are secondary residences.

The target collection scenario for the servicing company is to settle the debt pre-court. If that strategy fails, it can file for a court claim and thereafter have the property auctioned

Example of a note I have invested into (click on it to enlarge)

Each note consists of 8 different properties in Spain.

The objects list view shows:

Appraisal: the value of the underlying asset appraised by an independent company

PTV (price to value): PTV is calculated by dividing the price paid for the discounted debt by investors by the value of the property. E.g. in the second property 41%. The appraisal value is 429,404 EUR. The debt was bought for 177.000 EUR.

Term (M): Expected term in months

‘Exp. Return’: Expected annual return rate based on a moderate scenario, where 90% of the debt is settled within 18 months

Status: current status

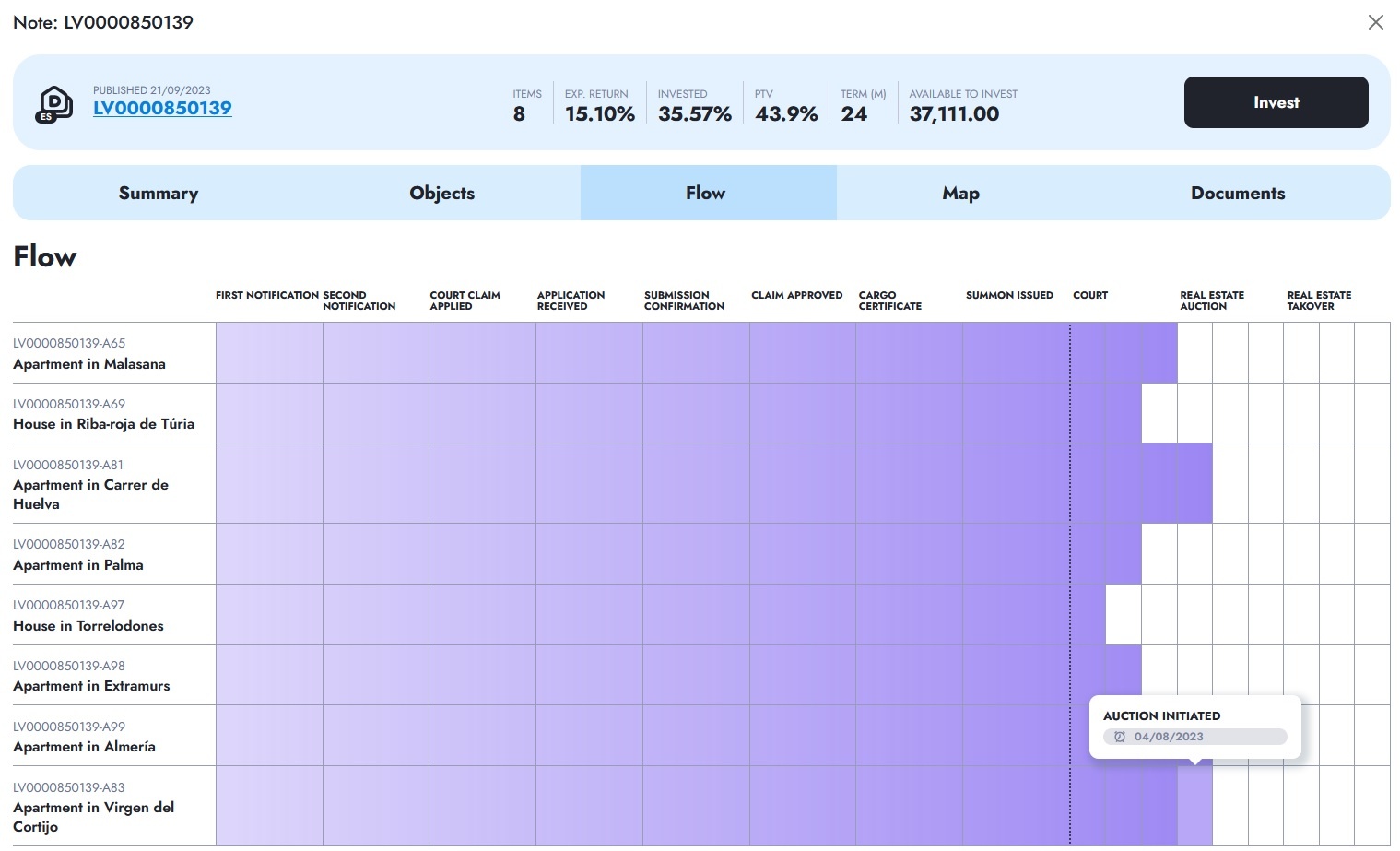

Flow view, showing the status progress of each loan in the note (click on it to enlarge)

It is important to understand, that an investment in a DDI note on Indemo* does not produce a constant cashflow for the investor. Once each attached property is sold for its market value, the investor receives a 50% profit share from the differential between the discounted price paid for the debt and the proceeds from the sale of the property. Usually, the average discount for objects placed on Indemo platform is around 40%. The investor gets repayment of the part of the investment amount and profit allocation once each and any debt in the basket of eight debts is recovered. In the flow chart pictured above the progress of each loan is shown.

Furthermore it should be clear, that this is a high risk investment and the the projected attrative yield of 15.1% might actually turn out higher, lower or even produce a loss. More on the sceanrios that are base for the calculation of the projected return can be found on the Indemo website.

The Indemo product offers

a novelty factor – discounted debt investments are not typically available to retail investors as a product

an interesting return/risk ratio. Considering the high discounts the debts are acquired for, there seems to be enough buffer even in challenging market environment conditions on the property market

I had the opportunity to discuss the pros and cons of the product on several occasions with the Indemo management team. I visited them in their office in Riga in May.

Indemo is fully regulated and licensed by the Latvian regulator. Indemo has so-called passports as an investment services company in several European countries, and is also member of the European Union investor compensation plan up to 20K EUR per investor (note this is against Indemo failure, not against loss of investment, read the specifics). Debt servicing and collection is performed by a professional servicing company authorised by the Bank of Spain according to Law 5/2019, of March 15, regulating real estate lending entities.

Investor signup on the Indemo* platform is pretty straightforward. First an identity verification by Veriff, thereafter answering several questions to determine product suitability. After that is completed the investor can deposit funds and invest. Indemo does not charge the investors any fees.

CrowdProperty was set up in 2013 because we personally felt the pain of raising finance for our property projects through decades of investing in, and developing, property ourselves. The three founders have 75 years’ experience of property investing and developing between us, meaning exceptional expertise in exactly the asset class we’re lending against). So, we set ourselves the challenge of building the best SME property development lender in the market, serving the customer needs we intimately knew better.

Traditional sources of finance have failed quality property professionals looking to undertake quality property projects for years. Large housebuilders feel this pain less but there are a finite number of large sites in this country to develop. Therefore, SME housebuilders are critically important but housing output from this segment fell from one third of UK output in 2008 to just 10% by 2017.

As a country, we need to unlock the power of entrepreneurial SME developers. Whilst Government initiatives around planning and taxation help, by far the biggest barrier is funding, according to 42% of respondents from our SME developer survey last year (which was the largest ever undertaken amongst this community).

This is exactly where our deep expertise lies, where our focus has always been, and where there’s greatest pain in the market. Having now built the best lender in the market, as property finance by property experts, we work in partnership with borrowers by adding value throughout their projects, and therefore deliver a better deal for all – our borrowers, our lenders, the under-supplied housing market and spend in the UK economy.

This is all crucial for CrowdProperty lenders: quality property professionals with quality property projects want to work with CrowdProperty, which has driven £3.8bn of direct project applications. From these, we have expertly curated £100,000,000 of lending – i.e. less than 3% conversion rate – across over 240 loans and 170 projects. This is testament to our tough criteria, rigorous due diligence and knowledge that a long-term lending business is only built through quality and track record, which is at the heart of all that we do.

As others have temporarily closed to retail investors, stopped allowing withdrawals, cut interest rates, introduced lender fees or even had regulatory permissions withdrawn, we have been able to continue funding quality projects which are ready to proceed, with naturally tighter criteria. We have further step-changed our reputation in the market on the borrower-side and direct applications are now c.£200,000,000 per month, with an ever-increasing quality mix.

We believe in data transparency to best inform investor decision making (illustrated by our award-winning statistics page and independent performance verification by Brismo). Resourcing our business strongly with a team of 32 and having a non-London base gives us considerable fixed cost advantage, savings from which we’re able to invest in expertise and further development of our in-house developed proprietary technology platform.

Our proposition is underpinned by an in-house developed proprietary technology platform for efficiencies of underwriting, data analytics, workflows, payments, funding, monitoring and reporting, coupled with decades of SME property development expertise for effectiveness. We have leading third party data, raw data feeds and internal analytics benefiting from nearly £4bn of applications. Property Director Andrew Hall has over 35 years’ experience as a qualified RICS surveyor, through multiple cycles, and is the leading expert in the team that validates deals that go to the investment committee. We have developed a rigorous due diligence process through decades of hands-on expertise in exactly the asset class being lent against. CrowdProperty is directly authorised and regulated by the FCA and an HMRC approved ISA manager.

If an investor would have invested the same amount into every CrowdProperty loan since 2018, what yield would he have achieved by now?

An XIRR of 8.15% (since launch it is 8.74%)**. We’ve now paid back £50,000,000 in capital and interest to lenders with an average rate of return of 8.74% p.a. and a perfect, 100% capital and interest payback track record. CrowdProperty also provides a tax-wrapper for UK-based investors lending through the CrowdProperty Innovative Finance ISA, SSAS pensions and SIPP pensions, all of which are very popular and significantly enhance effective returns due to the tax shields.

CrowdProperty loans are secured by a first charge. An important factor is appropriateness of the price set during valuation. How certain are you that valuations are in line with the market?

Indeed, all CrowdProperty loans are first-charge secured on the property assets, meaning that not only are CrowdProperty loans first in line to be paid back, but also CrowdProperty is able to be in control of any recoveries action, which is often overlooked in importance.

Our first charge security exposure averages provide a strong risk / reward proposition considering the returns offered by CrowdProperty:

Loan to value (LTV, or initial funds release relative to RICS-assessed market value) of 59.7% (55.9% in the 2020 cohort)

Loan to gross development value (LTGDV) 53.6% (excluding interest) and 58.5% (including interest)

The key factor is clearly the assessment of ‘V’ (value) in the above – both current value and end-product value – plus sensitivities of this critical data point to security and stability of the project. The ‘V’ is what we scrutinise most in the numbers, especially at the moment. We appoint societal-bound RICS surveyors with a long list of appointment criteria to conduct valuations on each and every project. This report is talked through with the surveyor and then validated with both leading internal and leading third-party data sets, used as inputs to our in-house expert-led analysis of the property asset in question, with a particular focus around understanding the nuances of the property, project and local market. In parallel, we are assessing the borrower and team in terms of not only their capabilities / experience but also their ambitions, motivations and commitment to this project and their professional property journey. Furthermore, project costings are internally validated by our expert team, supported by benchmark costings and a very detailed baseline Independent Monitoring Surveyor report and through the projects themselves, drawdowns are only ever made in arrears to project progress as formally assessed by the IMS.

CrowdProperty is entirely focused on funding quality property projects being undertaken by quality property professionals serving domestic under-supplied demand in liquid markets throughout the UK at mainstream, affordable price points, where there is enduring demand.

Are property prices going up or down? What factors do currently impact the UK market and where do investors find good (free?) market data to monitor the trend?

It’s been well documented over the past few months that UK property prices are rising, pushing house prices to a record high – the average price for property in UK stood at £315,150 in October 2020. This is being driven by Government stimulus such as the short-term reduction in property purchase stamp duty, but is also set in the context of relatively low growth in the last 3-5 years, real pricing levels that are the same as many points through the last 15 years and historically low transaction levels, resulting in pent up demand for those looking to get onto the property ladder and those wishing to move up / trade down.

We run extensive resilience analyses on both the market and our existing book at very granular levels, running both historical and theoretical scenarios. It’s helpful to reflect back on most recent shocks to the market (which are albeit driven by different macro-economic situations) and understand how trends preceding, during and after those compare to the current situation. We look at the market in a deconstructed way, influenced by what we have seen in the past. Firstly, we think about whether there is a correction waiting to happen given recent growth. Next, we think about the outlook for supply and demand. Thirdly, we carefully watch all activity indicators and finally we ensure that our focus, lending criteria and security are appropriate to uphold the high-quality lending we offer.

We believe that this shock will not lead to the correction of excessive growth that has been long-awaited. Examining he Nationwide House Price Index since 1975, one can see that both 89/90 and 07/08 experienced long periods of housing market growth before economic shocks drove double-digit percentage declines, taking years to recover. At first glance, one might think the signs are here again.

But this is where it is also important to examine real (inflation adjusted) as well as nominal growth – i.e. taking the effects of inflation out of the nominal (unadjusted for inflation) data. Real (RPI adjusted) growth shows a very different story to the nominal picture – average real values today are 16% below the 2007 peak, have been pretty much flat since early 2015 and are currently at the same real value as in 2010 and 2005. This is a very different context to the extended periods of high growth in values that led into the 89/90 and 08/09 market falls.

The balance of supply and demand for housing is again very different to 08/09. Back then, many needed to sell (including banks who adopted wholesale repossess and sell policies) and very few could buy (given the protracted state of the debt markets which was the underlying shock) or were prepared to buy (due to long-term prospects of the debt markets holding back recovery). Whilst the UK’s Job Retention Scheme has undoubtedly helped many households, as that is unwound, there is clearly significant uncertainty around job security and personal finances, and dwindling demand could be expected.

Whilst first-time buyers have been the driving force of the housing market for the last decade, Zoopla’s latest House Price Index suggests that homeowners are becoming increasingly active in the market. This makes sense as “equity-rich homeowners seek more space and a change in location”, while first-time buyers are being impacted by restricted mortgage availability, tighter lending criteria and growing economic uncertainty. Whilst 95% LTV high street owner-occupier mortgages aren’t back yet, in its analysis of the Prime Minister’s speech, Rightmove suggests that the government could be looking to tackle this by bringing back 95% mortgages as part of the effort to “turn generation rent into generation buy”.

On the supply-side, whilst unfortunately there will be many more probate listings this year, there will be a greater decrease in construction completions in 2020, which has been under-supplying the market for decades (part of the reason that CrowdProperty exists). As demand continues to outweigh supply, the market is seeing a 2.6% annual growth rate in UK house prices despite the economic backdrop according to Zoopla. Indeed, Nottingham and Manchester are recording annual house price growth of c. 4% alongside Leeds, Edinburgh, Leicester, Liverpool, Cardiff, and Sheffield. Rightmove’s data shows that searches across September increased 53% on average across the ten biggest cities, but there has also been an uplift in demand for smaller communities as buyers seek out larger spaces – analysts named nine areas where searches have doubled across Surrey, Somerset, Gloucestershire, Berkshire, Dorset, Kent and Suffolk which all have a population of under 11,000.Continue reading →