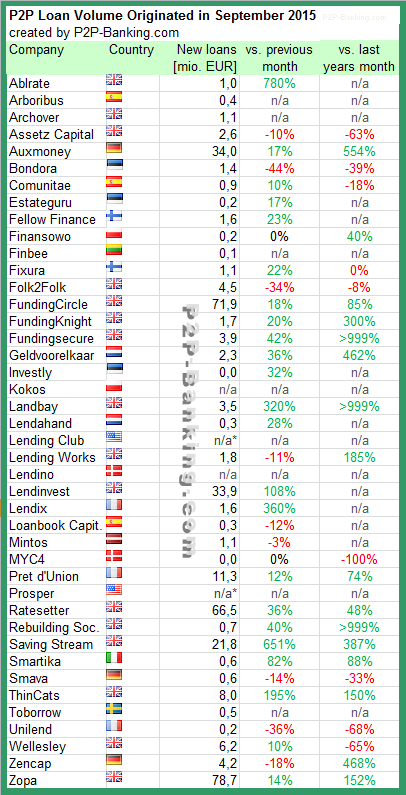

The following table lists the loan originations for September. Most marketplaces grew their loan volume compared to the previous month. Saving Stream had an exceptional month, with several very large loans. I added 4 new services to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in September 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

As reported earlier today, new p2p marketplace Crosslend (Spanish site) (German site) offers unsecured p2p loans to consumers. There was a soft launch phase last week, which enabled me to register early and gain first insights into the marketplace interface. After registration I awaited verification of the newly opened lender account at biw Bank and then deposited money there (if you are outside the Eurozone, you may consider using Transferwise or Currencyfair instead of doing a direct transfer).

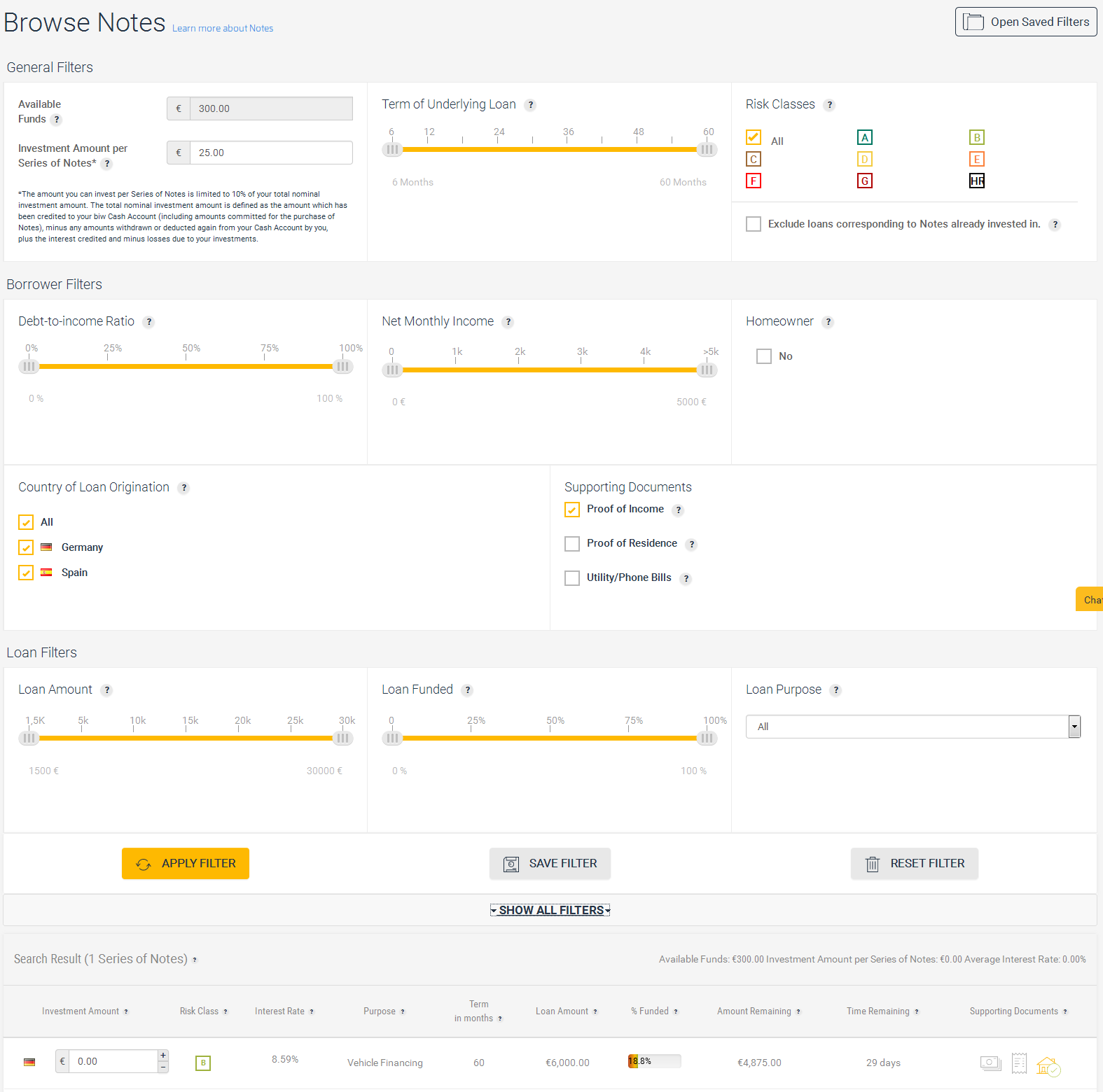

In the dashboard I selected ‘Browse Notes‘ which led me to an overview of all available note. Since my test was conducted during soft launch, there was only one available not.

Screenshot Browse Notes (click for larger view): at the bottom there is the listed loan (risk grade B) for 6,000 EUR vehicle financing at 8.59% interest

Crosslend Filters

Initially only the general filters (loan term, risk classes) for selecting loans are displayed. By clicking on ‘show all filters’ I expanded further loan selection filters: Borrower filters are DTI, monthly net income, home owner, country and supporting documents (proof of income, proof of residence and utility/phone bills). Loan filters include loan amount, funding percentage and loan purpose. It is possible to save filters to reapply them again in future. Continue reading →

Today, new p2p lending marketplace Crosslend launched offering unsecured loans to consumers. Opening to borrowers and investors in Germany and Spain as well as investors in the UK, Crosslend aims for further European expansion and creating a unified European marketplace.

The Berlin headquartered startup was founded by Oliver Schimek and Daniel Schlotter (both had previous FinTech experience at Kreditech) and Marie Louise Seelig (formerly Skrill). Crosslend already raised a funding round prelaunch from Lakestar, Atlantic Internet and others.

Markets targeted by Crosslend

When a loan is granted it is purchased and acquired by Luxembourg based Crosslend Securities SA and securitized by a series of ‘notes’. Notes are debt securities which can be purchased by investors. A series of notes is made up of a number of notes, each with a denomination of 25 EUR. The total nominal value of a series of notes is equivalent to the amount of the loan. When a borrower makes their loan repayments, CrossLend Securities SA makes the corresponding payments of interest and principal pro rata to the holders of the notes. This will enable Crosslend to offer a secondary market, which is due to be launched in a few months.

Borrowers can apply for loans from 1,500 to 30,000 Euro for loan terms from 6 to 60. Crosslend will grade loans in risk classes A to G, HR. Interest rates (APRs range from about 3.5% to about 17%) and borrower fees are dependent on the assigned risk classes. Crosslend checks submitted proofs of income for all loan applications.

To invest lenders first open an account with biw Bank, the partner bank of Crosslend, this involves a short video verification process of the investor’s identity (webcam required). Video verification is an innovative account opening process which several German online banks started to use to replace the identification via postal communication. Investors then deposit money into their account (250 Euro minimum). Then investors can choose which loans they want to invest into (25 EUR minimum bid per loan). Crosslend charges investors a 1% fee at origination.

UK investors should consider using Transferwise or Currencyfair to exchange money into Euro to avoid possible bank fees and a bad exchange rate applied by the bank. Continue reading →

British p2p lending marketplace Assetz Capital will launch a new ‘Quick Access Account’ (QAA) in the very near future.

The new account has a capped target rate of 3.75% gross per annum (before tax and any loan losses) and benefits from the added protection of a Provision Fund. The target rate can vary each month, being set at the beginning of each month based on the loans within the account, but the target rate will never fall below 3.75% gross per annum. Investors may invest up to 25,000 GBP each and the account will be capped at 1M GBP initially and is expected to grow in the future.

The QAA is designed to provide the highest possible speed of access to their money if an investor wishes to withdraw funds at any time, for whatever reason. In normal market conditions transferring funds between Assetz Capital Investment Accounts should be possible within seconds, while withdrawal of funds completely should happen within two days.

There is no fee for immediate access nor any notice period.

The accounts main use will likely not be long term investment, but rather help investors avoid cash-drag while waiting for new investment opportunities to open. Chris Mellish, Technical Director stated: “This isn’t an invest and hold account, ….  One feature … is that you can set your other accounts to automatically invest idle cash in the QAA.  So you could have 10K GBP invested in the MLIA, for example, waiting for a loan to draw down or waiting for .. loan units to become available and that money will earn 3.75% until it’s needed.  The system will automatically pull the money out of the QAA as soon as loan units become available on the loans you’re interested in.”

Stuart Law, CEO at Assetz Capital commented, “We believe that quick access to funds is a fundamental challenge in any investment product – whether it’s a bond, an ISA or a peer-to-peer product. The Quick Access Account not only means that money can be accessed quickly, but because of Assetz Capital’s model, the account offers a target rate of 3.75% gross per annum which should appeal to those looking for good risk-adjusted returns.â€

The Quick Access Account invests in both short and long-term loans and interest is earned and paid monthly. The account always retains substantial cash balances in order to facilitate quick access for investors who require their investment back on short notice and really helps address the issue on many P2P platforms where uninvested cash does not usually receive any return. An investor can press a button to choose to invest any spare cash they have at any time in the QAA and then release it when they wish to invest it elsewhere.

Mr Law, added: “This account really opens the world of peer-to-peer lending up to the mass market. Those investors who want to dip a toe in the water, earn a fair return and have quick access to their cash rather than be tied up in a 5 year loan can do so. Those who were worried about being able to access their funds quickly can be reassured that this product delivers that and therefore the returns on offer can be realised.†Continue reading →

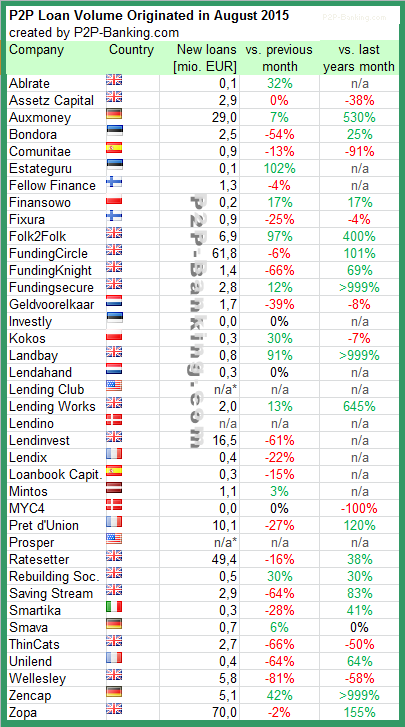

The following table lists the loan originations for August. August was a slow month for many of the listed services probably due to the holiday season. Zopa crossed 1 billion GBP lent since inception (see infographic) and Giles Andrews stated he expects the next billion to be lent in 2016. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

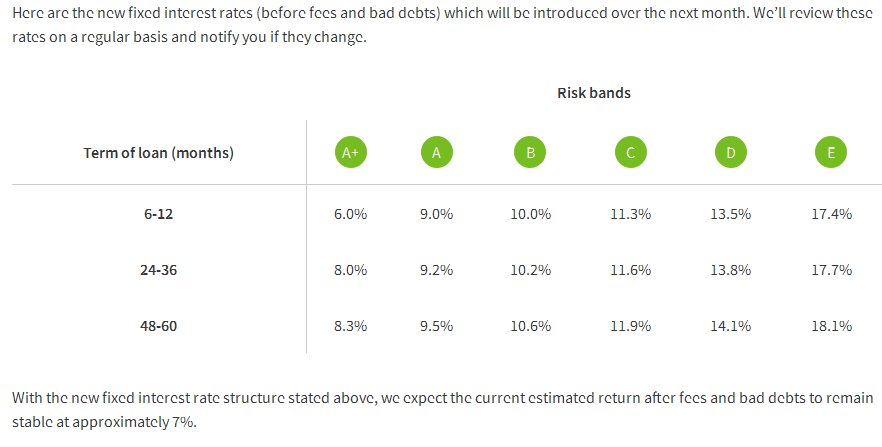

British p2p lending marketplace Funding Circle introduces a new model today. All new loans will be issued at fixed interest rates set by Funding Circle. Coming right after Funding Circle’s fifth anniversary, and 792 million GBP originated in loans to SMEs, the step to discontinue auctions is a major change in the way the marketplace operates.

Spokesman David de Koning told P2P-Banking.com that there were major drawbacks associated with the auction model for borrowers as well as lenders. Borrowers lacked certainty of the final interest rate until the auction period was over which led to some of them cancelling their loan application. Investors on the other hand experienced cash drag and sometimes had to make multiple bids to ensure they participate in the loan they wanted.

Under the new model Funding Circle will set the interest rate based on risk band and loan term. There will be 3 different rates for each risk bank. De Koning pointed out that the introduced model is not completly new for Funding Circle, as Funding Circle did already use fixed rates on property loans and on the US market of Funding Circle. Asked whether he expects loans to close instantly as demand could be higher than loan supply, he said he could certainly see loans to close quicker than before. The long term goal envisioned is that in future borrowers may pre-approve a loan before it is listed and it could close instantly once filled. Continue reading →