‘Easy access’ investment will be available in a RateSetter ISA

RateSetter has improved customers’ access to their money by removing all early exit fees from its monthly investment market. This means that RateSetter’s 33,000 investors can now benefit from great rates of return combined with easy access to their money.

RateSetter’s monthly market has proven very popular with investors, delivering an average rate of 3.1% p.a. over the last five years. The latest rate can be found here.

As with all marketplace lending, the speed of access to money is dependent on liquidity. RateSetter has managed market liquidity for over five years, the result being that no investor has ever had to wait to withdraw their money from RateSetter. Early withdrawal fees remain in place for RateSetter’s one year, three year and five year investments. More information can be found here. RateSetter is looking at options to simplify the way fees are calculated to provide greater certainty to investors.

The announcement comes less than two months before the launch date for the Innovative Finance ISA (IF ISA) on 6 April and follows the release of information on RateSetter’s forthcoming IF ISA over a week ago. RateSetter has confirmed that customers will be able to invest in any of its markets within an IF ISA wrapper, and thus can benefit from easy access investments with tax-free returns. Continue reading →

CommuterClub delivers a new and innovative way to access public transport as a subscription service.

By bringing together a low cost loan with the existing annual ticket, CommuterClub can deliver the savings of an annual, in a far more convenient and attractive package as a monthly payment plan.

Our goal is to continue to bring new innovative products for commuters, delivering value for money and ease of use.

I really like the fact that your business model builds on long customer relationships. What do you do to achieve high customer satisfaction?

CommuterClub operates in a sector dominated by large slow moving monopolies who manage public transportation. Our proposition is to offer an alternative approach to commuters that begins with their needs. Our focus on a simple customer journey, great customer service and a simple product all deliver a fantastic outcome for consumers.

This is key in ensuring high customer satisfaction and providing a real alternative to the existing ticketing options.

The audience of this blog is highly interested in p2p lending. Can you please explain how your company ties into this industry and what role Ratesetter and potentially Zopa play for your financing?

CommuterClub works with RateSetter to fund all loans. As a business P2P was the key building block enabling us to deliver a low cost and flexible product to consumers, something that we would have found exceedingly difficult if we worked with incumbent banks.

We expect to continue to work with p2p going forward and to maintain our close relationship with RateSetter.

The pitch video

The timing of this round is a bit of a surprise to me since you indicated to shareholders recently ‘at our current trajectory we expect to be [able to] sustain growth from retained earnings’. Why did you decide to raise further capital now?

CommuterClub has made tremendous progress in diversifying the business expanding nationally in the UK, launching a B2B solution and also looking to cover other verticals like parking.

This expansion of our product set has also expanded our target market and we are now raising capital to fund our continued expansion and growth.

Name one fact that makes your pitch a better investment than any other pitch on Seedrs.

Real, proven traction backed by millions in loans and thousands of happy customers.

Silver Bullion buys, sells, authenticates and stores physical gold and silver. Since mid-2015 we also launched the option for customers to securely lend and borrow to each other using their bullion as collateral.

What are the three main advantages for investors?

Physical bullion buyers receive the best protection possible (in jurisdictional, counterparty and storage risk terms) against systemic crises by being owners of insured physical property under Singapore law rather than bank creditors exposed to financial crises. They also have a long position in gold / silver. They profit from a financial collapse, hyperinflation or foreign nationalizations.

Alternatively, as lenders they receive a safe return (very low risk) by lending their funds to owners of insured and authenticated bullion stored with us. Lender funds are collateralized by a minimum 200% worth of gold and silver and, should during the duration of the loan, the collateral fall to 125% the borrowers will get a margin call. At 110% we will liquidate (sell) the borrower’s silver and gold to ensure the lender’s funds are always fully covered by liquid collateral.

Lenders can offer their funds at an interest rate and duration of their choosing. Borrowers are then free to accept the best rates and vice versa, thereby creating a Bid/Ask exchange which lets lender and borrowers determine their own interest rates. The system is also inexpensive (0.5% fee) and easy to use as borrowers do not need to be rated or scored due to their collateral.

What are the three main advantages for borrowers?

Because the loans involve so little risk (due to collateral) lenders are willing to accept comparatively low interest rates. Therefore borrowers can borrow cheaply (e.g. 4% p.a.) and unlock their bullion liquidity without selling it. The low rates allow for arbitrage opportunities vs. customer in high interest countries.

Because we have an abundance of lenders Borrowers can quickly and easily get a loan whenever they need it, without any usage restrictions and minimal additional paperwork.

Borrowers can choose to easily roll-over /refinance a loan before maturity. So they could roll-over as needed, giving them flexibility and a source of optional liquidity when needed.

Investors are required to open a storage account first. Doesn’t that deter those that only want to invest?

A storage account is required to do our AML and KYC checks and an account number is the pre-requisite to do P2P transactions. A customer / lender does not need to buy or store bullion and there is no cost associated with opening an account. So there is no downside.

What ROI can investors expect?

P2P Lenders have received secure returnsranging from 3.5% to 7% p.a. depending on currency, duration and borrower/lender demand. The nature of the bullion collateral also means are also well protected against both a borrower default and systemic defaults in a crisis.

It depends on the lender whether and how he values this risk diversification.

Is the technical platform self-developed?

Yes. It is highly specialized platform that is integrated with our bullion storage system which stores around 120 million SGD worth of physical bullion.

A word about the people who designed this P2P system might be in order. Gregor Gregersen (primary architect) was a senior data architect for Commerzbank (the second largest German bank), Otbert de Jong headed the global risk advisory department at ABN AMRO Bank and was a partner in PricewaterhouseCoopers and Simon Black is the founder of Sovereign Man, which is one of the best resources on internationalisation and spreading your risk. Continue reading →

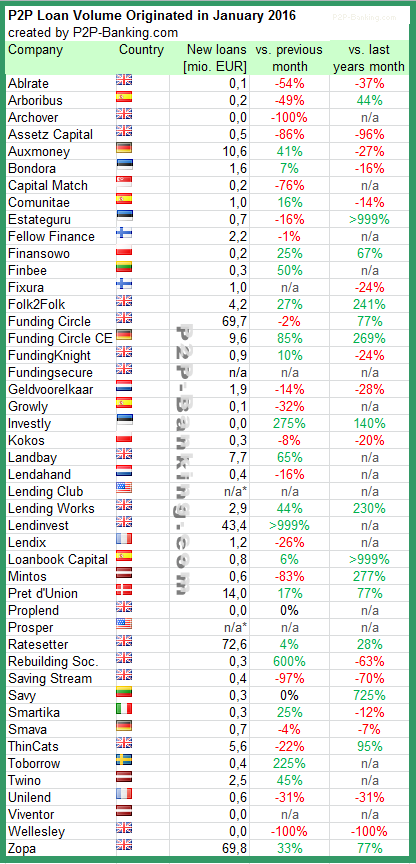

The following table lists the loan originations for January. This month Ratesetter led, followed by Zopa and Funding Circle. I added one more marketplace to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in January 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

In mid-January Crosslend added Dutch loans and I made a bid on the first Dutch loan listing. The majority of loans are still sought by Spanish borrowers. Currently there are over 50 Spanish loan listings available and also a few German or Dutch ones.

10% Cashback

Crosslend currently offers a cashback promotion. New and existing investors get 10% cashback on all successful investments made until March, 31th 2016 (up to a maximum bonus amount of 1,000 Euro per investor; further conditions apply, e.g. minimum investment of 250 Euro during promotion period). Investors contemplating to test Crosslend should consider making use of this cashback offer now.

Update Jan 31th: was informed that this offer runs currently only in the German market; other markets will follow later