In December 2013 I saw the pitch of a promising pre-launch UK p2p lending startup called Landbay pitching on the UK p2p equity platform Seedrs to the crowd. The pitch explained how they planned to do p2p lending secured by property in the UK. I liked the proposal and invested a small amount in Landbay shares.

Since then it has been very interesting journey. I watched how Landbay fared, saw them grow the marketplace substantially. There have been subsequent following rounds into which I invested again. Shares issued through Seedrs come with pre-emption rights, that means I am entitled (but not obliged) to invest in next rounds to avoid dilution of my share percentage.

Currently Landbay is pitching to raise 1M GBP at a pre-money valuation of 10.3M GBP. You can see the current pitch here. The shares are priced at 85 GBP, that is the minimum investment amount (normally most Seedrs pitches come with a minimum investment of just 10 GBP). At the time of this writing the pitch is already filled 91%. Before it opened for public bidding recently, it was only accessible for existing shareholders like me to enable them to execute their pre-emption rights. I am not sure the pitch will allow overfunding.

Last week Landbay announced that they received an investment from Zoopla. Zoopla is a company that operates property sites uSwitch and Prime Location.  Zoopla announced full year results (ending September 20, 2015) showing a revenue increase of 34% as the top line number jumped to £107.6 million. Profit for the year increased 20% to £25.4 million.  The partnership with Landbay is designed to help scale their retail customer base as the P2P lender becomes a more established mortgage lender.While the precise amount of the investment into Landbay was not disclosed, Zoopla invested into a total of 4 companies and the total for that was 1M GBP. This deal will also trigger previous convertible rounds that Landbay did on Seedrs.

If you are interested in the pitch you don’t need to be a UK resident. Just sign up at Seedrs and follow the process. If you are outside of the UK, I recommend considering to use Transferwise or Currencyfair, when depositing money in order to reduce currency transfer fees significantly. If you are a UK resident, note that the pitch is EIS eligible.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

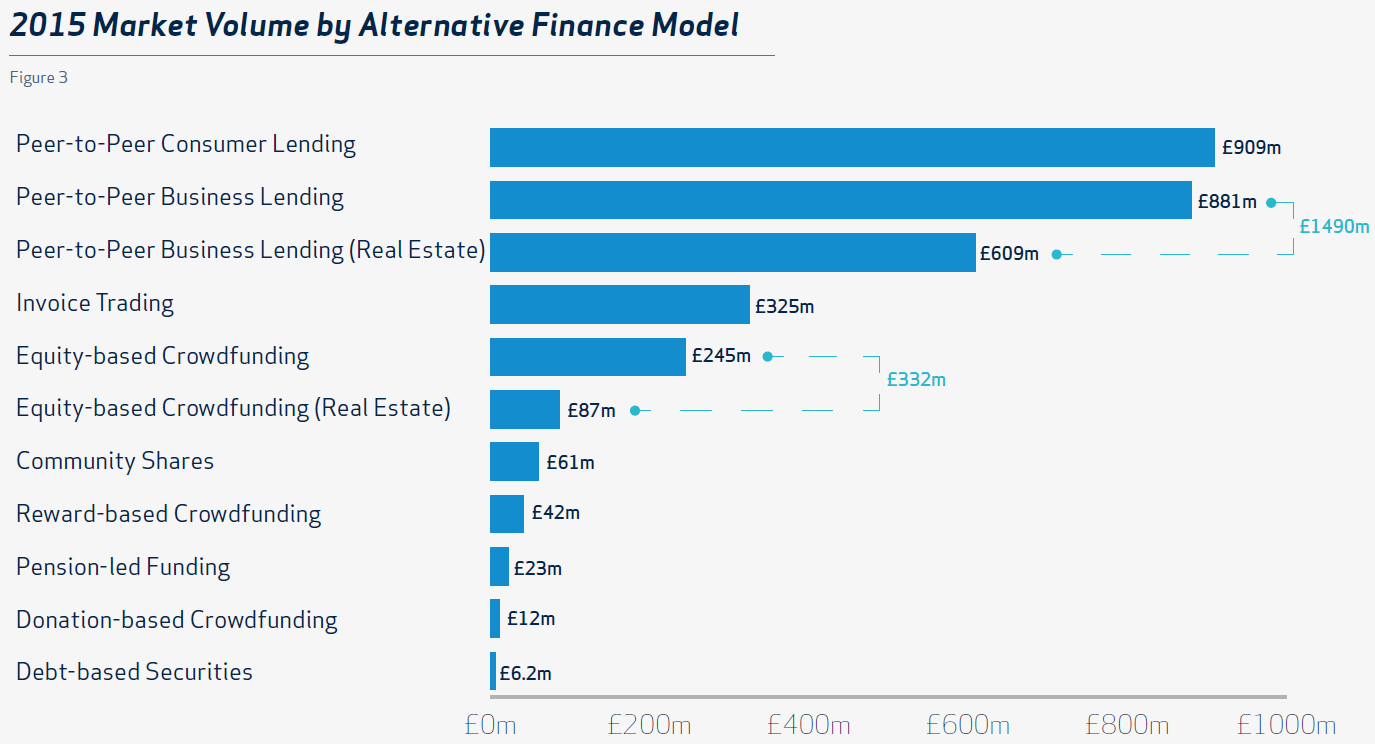

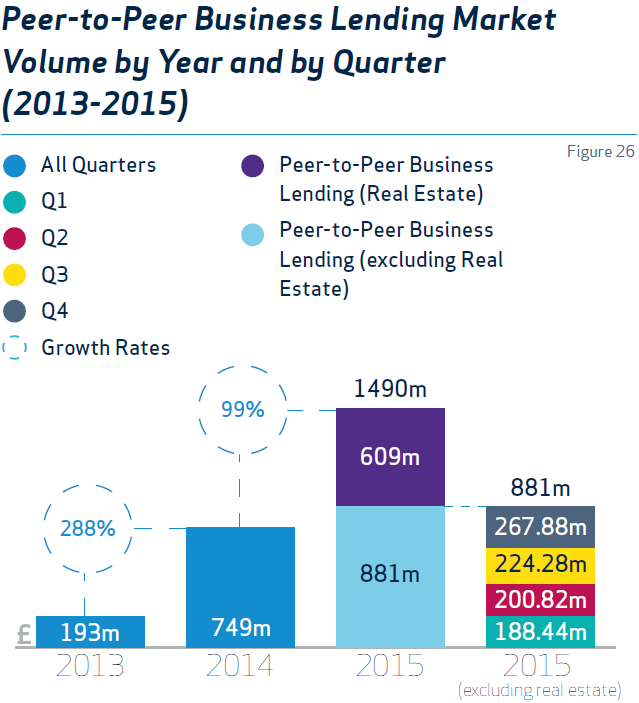

Landbay loan volume growth