Zopa's new Zopa listings contain several pieces of information. Apart from the "basic information" which include loan amount, loan length, preferred rate, loan purpose, borrower ID, borrower signup date and listing end date, these are:

Credit score

The rating we give to the borrower’s credit score at Callcredit, a UK credit reference agency, relative to other Zopa borrowers

Affordability

Zopa rating (stars) for the borrower based on income and expenditure details provided by the borrower.

Stability

Zopa rating (stars) for the borrower based on details provided by the borrower, such as residence and employment.

Personal profile

Listing text supplied by borrower

Income/Expenses

Self reported detailed budget (see screenshot above for example) Continue reading →

Prosper.com applied several changes as described in this announcement. Some of the changes were expected as plans had been known, some were surprises.

Portfolio plans

Portfolio plans allow the lender to automatically build a conservative, balanced, moderate or agressive portfolio. That means the lender no longer picks individual loans to bid on but chooses to invest in a plan. The feature is implemented based on Prosper's standing orders. The difference is that it uses standing orders predefined by Prosper, not by the lender. Prosper shows "estimated returns" for each portfolio – currently ranging from 8.37 to 11.06 percent. Comment: Lendingclub introduced this concept earlier on. Lenders are currently examining and debating on which rationale Prosper did build the standing orders behind the portfolios.

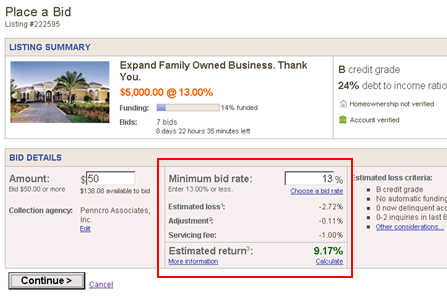

Estimated ROI is shown in listings

Prosper now shows the estimated return on each listing, including predictions for defaults and costs for the servicing fee. The default estimate is now based on Prosper's own data (past performance) rather then Experian data.

Comment: This display does improve lender information especially for unexperienced lenders.

British Zopa.com has launched the Zopa listings. The Zopa listing feature, of which the plans had been announced in August show individual borrower listings requesting loans. The concept is similar to the listings other p2p lending services like Prosper.com use. Read this earlier description of Zopa listings.

MicroPlace’s mission is to help alleviate global poverty by enabling everyday people to make investments in the world’s working poor.

Our idea is simple.

Microfinance institutions around the world have discovered an effective way to help the world’s working poor lift themselves out of poverty. These organizations need capital to expand and reach more of the working poor. At the same time, millions of everyday people here in the United States are looking for ways to make investments that yield a financial return while making a positive impact on the world. MicroPlace simply connects investors with microfinance institutions looking for funds.

The result: more microfinance in the world, satisfied investors, and above all, fewer people living in poverty.

Lenders (termed investors) can invest via Paypal (no paypal fees). Their money goes to the selected microfinance institution (MFI). The MFI uses the money on the purpose described. The investor buys a security issued by a security issuer. Currently investment offers have terms of 2 to 3 years with interest rates between 1 and 3 percent. Each investment offer (example) is described in detail by a prospectus.

Only U.S. residents are eligible to become investors. Minimum investment amount varies by offer (typically 50 US$).

In early September I started funding peer-to-peer microloans to African entrepreneurs on MyC4. Yesterday the first repayments were credited to my account. Siraje Sselugo, a poultry farmer, that wanted to increase the number on chicken paid on time. I had loaned him 20 Euro for a 6 month term at 24% interest. Lydia Lwanga, who sells school stationary and wants to stock more products with the loan, repaid on time. My loan to her was 15 Euro for a 6 month term at 22% interest. All the other repayments were on time, too:

(Screenshot of my account balance at MyC4).

MyC4 allows minimum bids of 10 Euro. So far my portfolio contains 37 small bids on funded loans.

Earlier this month the first Australian p2p lending service iGrin.com.au quietly launched. Here is what Phil Hopper, iGrin's CEO told me, when I contacted him about iGrin's goals: 'We set out with the intention of being Australia's first and best P2P banking community. To date we have intentionally kept a low profile whilst we have gone about proving our business model and ensuring compliance with the Australian regulatory environment. The team behind iGrin has predominantly come from the banking industry and brings with it a wealth of product development, technology and lending experience. We have been impressed with the advances made in P2P lending overseas and are looking forward to applying these to the local Australian market and enabling everyday Australians to get great rates and great returns.'

Browsing the site, the main parameters are:

Borrower fees are 1% (for AA to D credit grades) or 2% (HR) or 90 AUS$ (whichever is greater)

Lender fees are 0.5 to 1.5% annual loan servicing fee (depending on credit grade)

Loans are possible for amounts from 2000 to 25000 AUS$ (approx 22000 US$)

Lenders can invest from as little as 100 AUS$ to a maximum of 25000 AUS$

There is a bididng process, where the borrower sets the initial (maximum) interest rate he is will to pay and lenders bid down the rate (like at Prosper.com)

Currently all loans are for a term of 3 years

The way the Australian credit rating works, simply appling (whether successful or not) for a loan may impact one's credit grade

A feature that differs from other p2p lending platforms is the 'Member direct loan' iGrin offers:

A service that iGrin provides to allow members to offer a loan direct to an individual. We will then undertake all of the transfer of funds and ongoing payments on behalf of the members. This is a great way for family or friends who wish to lend money to each other to have a third party (iGrin) manage all of the repayments and transfer of funds on their behalf. A formal contract is put in place between the two parties. It can also be a great way for someone to improve his or her credit rating.

While a family and friends loan is possible on other p2p lending services too, it is noteworthy that iGrin charges lower fees for Member direct loans than for normal loans.

Excerpts of answers to other questions I asked Phil Hopper, CEO of iGrin.com.au:

P2P-Banking.com: Which background does the management have?

iGrin.com.au: … The founders have over 50 years experience in Banking and Finance. The original founder and CEO is Phil Hopper who has a strong background in Banking and Technology most recently at the Commonwealth Bank of Australia and prior to that at Macquarie Bank. Continue reading →