Plum is another fintech that makes use of Ratesetter’s products through a cooperation. Plum is bot on Facebook messenger designed to automate savings for the user and to invest money on his behalf. Savings can currently be invested in Ratesetters rolling market. Plum is currently pitching to raise 700K GBP through a convertible with a valuation cap of 5M GBP on Seedrs. Watch the video for more information on the Plum product and pitch. The minimum investment for this equity crowdfunding campaign is 10 GBP. The pitch is EIS eligible (UK residents). Other investors include 200K US$ invested by VC 500 Startups. This pitch is not yet officially launched on Seedrs, but already open for investments. You can use P2P-Banking’s free notification service to be alerted of upcoming Seedrs pitches early and review them ahead of the crowd.

Competitors of Plum include Digit, Qapital, Clarity, Albert, Squirrel, Cleo and Savedroid.

The Plum pitch deck is informative reading. To request that, login, click on ‘Documents’ in the pitch, and send a message to request the pitch deck.

Another example of an innovative cooperative cooperation making use of products of a p2p lending service is Commuterclub.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

This article is a must read for non-residents, investing on British p2p lending marketplaces from abroad. You will learn two advantages that will make the process easier for you and save you money by using the free Revolut App.

What is Revolut?

Revolut is a free app for money management. To register you need:

An Android smartphone or an iPhone with front and back camera

to be a resident in the European Union, Norway or Iceland and your ID document (e.g. passport)

the ability to receive SMS messages

Just download the app in the Google Play store or the App Store on iOS.

After that, I suggest to first follow the steps described that are needed to verify your identity, as this is a prerequisite for some of the features described further down. This took me about 10 minutes.

Usecase 1: Free transfer of money from one UK p2p lending marketplace to another

I have invested on several UK p2p lending marketplaces, but there was no free way to shift money from one UK marketplace to another as I do not have a UK bank account, since I am not a UK resident. Up to April last year I could use a free Monese account, but Monese started charging 5 GBP per month, so that was no longer an option.

Every Revolut user can get an own UK bank account number for free. Important update: Not true any more for new accounts – see comments. It is important to note though that technically Revolut is regulated as an electronic money issuer and is not a bank. This means that money in your account is not protected by the UK deposit protection scheme (FSCS)! However that is fine for me as I just use the account to pass the money through on the way from one platform to another.

The important fact is that with the own account number it is possible to use that for withdrawals from UK marketplaces as no reference is needed for the transfer. I have done this a couple of times now and it takes only a few hours for the money to arrive and get credited. Likewise it only takes a few hours after I transfer it to another platform to be credited there. All without incurring any costs for me.

Entering the recipients bank details on a smartphone is a bit cumbersome, but it needs to be done only once, as the details are stored and can be reused for future transfers.

Note to UK investors: You cannot use the Revolut app likewise for transfering funds from on p2p lending platform in the Eurozone to another p2p lending platform in the Eurozone. At least not at the moment. The reason for this is that users don’t get an own IBAN account number. Warning: Revolut will block Euro transfers that come from a third party and return them and deduct a fee and return the funds to the sender.

Another potential benefit might be, that foreign investors could gain access to those UK platforms that don’t require residency but do require a UK bank account. But I haven’t tried if that works with a Revolut account. If anybody checks this out, please post your experiences in the comments.

Usecase 2: Best exchange rate for changing Euro into Pounds

Conventional bank transfers are not a good option for moving money from an Eurozone bank account to a UK p2p lending platform due to fees and bad exchange rates applied.

Instead I used Transferwise and Currencyfair so far and have been happy with these services. However there might be issues with platforms not supporting withdrawals via these.

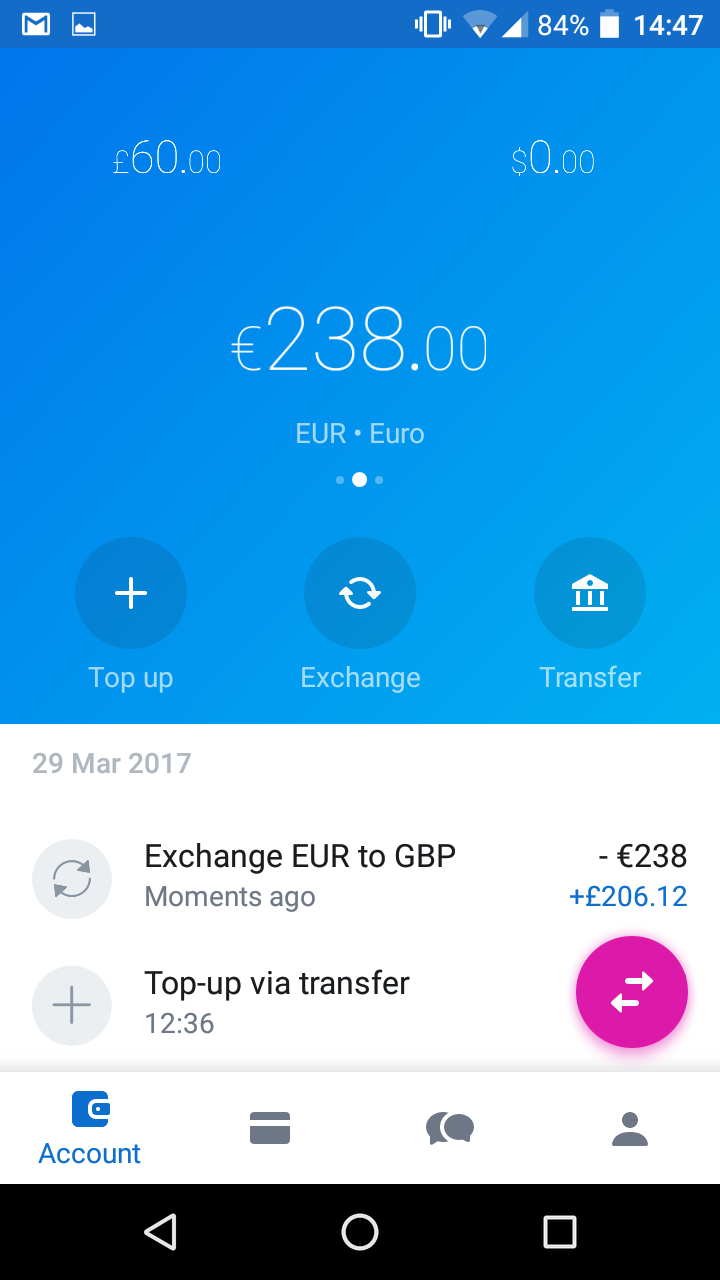

And when I did a comparison of exchange rates at the time of writing this article, I found that actually Revolut offers a much better exchange rate. This is what I got when I compared:

Revolut: 238 Euro gets 206.12 GBP

Transferwise: 238 Euro gets 204.92 GBP

Currencyfair: 238 Euro gets 202.91 GBP

Quite a difference, though it will be smaller for larger amounts and you can actually influence the exchange rate on Currencyfair by setting a desired rate.

To exchange Euro into pounds I simply transfered money from a bank account in my name via a SEPA transfer to the Euro account of Revolut, stating my personal reference number the Revolut app showed me under ‘Top-up‘, ‘EUR‘ ‘Bank transfer‘. After two days Revolut alerted my via push notification (they don’t send emails) that the money arrived. Via the exchange menue point I can then see the fluctating live exchange rates and execute the exchange any time I want.

Important tip: Never exchange money on Revolut on a weekend, as Revolut will charge a 1% fee then.

Also note that there is a limit of 5,000 GBP /Â 6,000 EUR / 6,000 USD (or equivalent) per calendar month for the free foreign currency exchange. That is sufficient for my needs. Above that Revolut charges a 0.5% fee. If you invest really large amounts it might by worthwhile to consider upgrading to a premium account for a monthy fee as premium accounts do not carry fees even for larger exchanges.

To sum up: Revolut makes investing on multiple UK p2p lending platforms much easier for European investors and can save a lot of money during currency exchange for investors from the Eurozone. I have used the account for only a few weeks so far and I really like it and I do hope the basic account will stay free.

Fans will actually have the opportunity to invest into equity of the Revolut company and own shares of Revolut soon. This will be conducted through the equity crowdfunding platform Seedrs. The concrete date has not been announced yet, but if you are interested you should register at Seedrs now to complete the registration and verification process ahead, as I expect the Revolut campaign will be oversubscribed and filled within hours, if not minutes, once it is launched. In fact, when Revolut raised 1 million GBP last year on Crowdcube, the offer was massively oversubscribed. To see how pitches work at Seedrs have a look at the current pitch by p2p lending company Landbay or read my earlier articles about Seedrs. Notice:This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

Revolut says it currently has 550,000 users. I expect that to rise fast with the advantages the Revolut account offers. Have you used Revolut in the context of your p2p lending investments? You are welcome to share your Revolut experiences in the comments.

Oh and I forgot to mention: There is even another interesting tie-in of Revolut with peer to peer lending. UK users can get a loan through Revolut which is actually handled by Lending Works funded though fellow p2p lenders. During AltfiEurope Summit a figure of 300 referred loan applications per day was given and that was only 2 weeks after launch.

Wellesley is a lending business. It provides an alternative for borrowers than traditional high street lenders. Our business allows us to meet the needs of two key underserved markets:

experienced mid-sized property developers who are building homes in the UK

investors seeking higher returns that can be achieved in deposit accounts who are willing to take a level of additional risk through a range of different products.

What are the three main advantages for lenders?

Lenders can achieve higher risk adjusted returns than are available in traditional deposit accounts

Property development lending is asset backed

Funding is being put to good use, helping to build homes in the UK

What are the three main advantages for borrowers?

They are dealing with a lending firm who specialises in property development

We are committed to very high levels of service and quick decisions

Each individual borrower is important to us

Wellesley is quite established in the UK marketplace lending sector. Why do your raise capital via Seedrs through a convertible now?

We want to raise more capital to enable us to invest in acquiring new customers and developing our technology. All of our external funding is retail rather than institutional. Raising further equity through a retail route will help us to build a business where strong alignment of interests between investors and shareholders will build a stronger company for the long term.

To which extend (if any) are equity investors covering capital losses on loans to p2p lenders vs the mini bond holders?

So far the board has chosen that the company (shareholders / equity investors) will cover the losses incurred by all other investors. This is at the board’s discretion and investors are all aware that they are taking risk in relation to property development lending. Investors continue to carry the risk of losses on both P2P and mini-bonds.

Wellesley aims to use the funding to expand its business, its marketing, human resources and IT development.

Wellesley originated about 80M pound YTD. Did you experience any effect of Brexit and what is your outlook for 2017? How do you see the opportunity of the IFISA market?

In the run-up to the referendum and in its immediate aftermath property development across “middle Britain†took somewhat of a pause. There are signs now that growth is returning to the market and the outlook for 2017 is positive as the key driver – the demand for more housing – shows no sign of reducing.

We continue to develop a product that meets the technical requirements of the IFISA market and will provide an update as soon as there is more to say.

We specialise in multi-unit developments, our average unit size is less than £500k. As a result we believe that we are well-placed to face any challenges that the UK residential housing market may face post-Brexit.

Are there any plans for international expansion?

At this stage, quite the opposite. We had started doing some lending in Majorca, Spain and decided back in the first half of 2015 that we would be better able to serve our customers through the economic cycle if we focused on our core expertise and competency in the UK market.Continue reading →

Flender is a peer to peer finance platform which helps businesses and consumers to borrow and lend money through their existing networks.

Businesses can leverage their customer base and strengthen loyalty; while friends become part of each other’s’ success. Flender does this while adding a new element of trust via social network connections.

Flender emphasizes the social relationships between borrowers and lenders. Don’t you think borrowers are hesitant to ask friends and connections for money?

The social lending market among friends, family and connections has never been formalized, which is crazy when you consider that this is a market worth over 3 billion EUR a year in Ireland and the UK based on independent research performed in September 2016.

Asking people that you know for money – and lending to them – is an awkward thing to do and is certainly an unreliable means of finance. Whether it’s to fund further study, grow a business or to fund home improvements, Flender will let you borrow from and lend to people with whom you have a connection much more easily.

For individuals, there is the satisfaction of helping others while earning more interest than a standard savings account while businesses can have access to funds faster and at the interest rate they prefer. Everyone wins.

P2P lending has evolved a lot over the past 10 years. Your model has a back to the roots touch to me. Do you see your model as a reinvention of the true spirit of p2p lending?

I believe p2p lending and the sharing economy is the future of finance.

We have all lent or borrowed money at some stage of our lives and will use some sort of finance in the future – be it mortgage, car leasing, credit card, deposit account or investments. Similarly, we all have people in our social circles and professional networks who have money to lend or are looking for finance. It makes no sense that rather than doing these transactions with people who you know and trust we would do these with complete strangers with whom we know little or nothing.

Flender is not trying to create a new marketplace. We are simply formalising existing massive social lending market and by providing a seamless user experience and having first- mover advantage we feel we can dominate this sector.

Flender positions itself as different to other p2p lending marketplaces. Yet you take these as benchmarks for valuations in an exit. Furthermore your expected margin is much higher than those of other UK p2p lending marketplaces. What is the reasoning behind this?

Yes, we are very different to other p2p platforms, but investors will initially want to benchmark against something with which they are familiar, hence our comparison to existing platforms. Continue reading →

In December 2013 I saw the pitch of a promising pre-launch UK p2p lending startup called Landbay pitching on the UK p2p equity platform Seedrs to the crowd. The pitch explained how they planned to do p2p lending secured by property in the UK. I liked the proposal and invested a small amount in Landbay shares.

Since then it has been very interesting journey. I watched how Landbay fared, saw them grow the marketplace substantially. There have been subsequent following rounds into which I invested again. Shares issued through Seedrs come with pre-emption rights, that means I am entitled (but not obliged) to invest in next rounds to avoid dilution of my share percentage.

Currently Landbay is pitching to raise 1M GBP at a pre-money valuation of 10.3M GBP. You can see the current pitch here. The shares are priced at 85 GBP, that is the minimum investment amount (normally most Seedrs pitches come with a minimum investment of just 10 GBP). At the time of this writing the pitch is already filled 91%. Before it opened for public bidding recently, it was only accessible for existing shareholders like me to enable them to execute their pre-emption rights. I am not sure the pitch will allow overfunding.

Last week Landbay announced that they received an investment from Zoopla. Zoopla is a company that operates property sites uSwitch and Prime Location.  Zoopla announced full year results (ending September 20, 2015) showing a revenue increase of 34% as the top line number jumped to £107.6 million. Profit for the year increased 20% to £25.4 million.  The partnership with Landbay is designed to help scale their retail customer base as the P2P lender becomes a more established mortgage lender.While the precise amount of the investment into Landbay was not disclosed, Zoopla invested into a total of 4 companies and the total for that was 1M GBP. This deal will also trigger previous convertible rounds that Landbay did on Seedrs.

If you are interested in the pitch you don’t need to be a UK resident. Just sign up at Seedrs and follow the process. If you are outside of the UK, I recommend considering to use Transferwise or Currencyfair, when depositing money in order to reduce currency transfer fees significantly. If you are a UK resident, note that the pitch is EIS eligible.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

CommuterClub delivers a new and innovative way to access public transport as a subscription service.

By bringing together a low cost loan with the existing annual ticket, CommuterClub can deliver the savings of an annual, in a far more convenient and attractive package as a monthly payment plan.

Our goal is to continue to bring new innovative products for commuters, delivering value for money and ease of use.

I really like the fact that your business model builds on long customer relationships. What do you do to achieve high customer satisfaction?

CommuterClub operates in a sector dominated by large slow moving monopolies who manage public transportation. Our proposition is to offer an alternative approach to commuters that begins with their needs. Our focus on a simple customer journey, great customer service and a simple product all deliver a fantastic outcome for consumers.

This is key in ensuring high customer satisfaction and providing a real alternative to the existing ticketing options.

The audience of this blog is highly interested in p2p lending. Can you please explain how your company ties into this industry and what role Ratesetter and potentially Zopa play for your financing?

CommuterClub works with RateSetter to fund all loans. As a business P2P was the key building block enabling us to deliver a low cost and flexible product to consumers, something that we would have found exceedingly difficult if we worked with incumbent banks.

We expect to continue to work with p2p going forward and to maintain our close relationship with RateSetter.

The pitch video

The timing of this round is a bit of a surprise to me since you indicated to shareholders recently ‘at our current trajectory we expect to be [able to] sustain growth from retained earnings’. Why did you decide to raise further capital now?

CommuterClub has made tremendous progress in diversifying the business expanding nationally in the UK, launching a B2B solution and also looking to cover other verticals like parking.

This expansion of our product set has also expanded our target market and we are now raising capital to fund our continued expansion and growth.

Name one fact that makes your pitch a better investment than any other pitch on Seedrs.

Real, proven traction backed by millions in loans and thousands of happy customers.