There is news today from Estateguru* a marketplace for property backed loans to SMEs in various European countries.

Estateguru has announced that the Estonian Financial Supervision and Resolution Authority (Finantsinspektsioon) has granted the platform its European European Crowdfunding Service Providers for Business (ECSPR) licence, allowing it to operate as a crowdfunding service provider across all European Union (EU) member states under unified rules.

Estateguru was the first crowdfunding platform to be regulated in several markets, including Lithuania, Finland and the United Kingdom. The granting of the new Pan-European licence serves to confirm that the company is fully compliant with all of the recently introduced regulations and that its internal processes and procedures meet the financial standards necessary to operate anywhere in the EU.

‘The ECSPR licence marks a significant milestone for Estateguru, enabling the platform to expand its services and provide investment opportunities to a wider user base throughout the European Union. The recently introduced ECSPR regulations provide for greater transparency for investors and introduce new obligations to ensure consumer protections and safeguard the interests of investors,’ said Mihkel Stamm, CEO of Estateguru.

Estateguru says it has been proactive in preparing for this regulatory change, having already implemented customer checks, complaint-handling protocols, appropriate marketing messages, and other changes in order to fully comply with the ECSPR regulations. The company had previously championed the creation of the regulations and even contributed to their formation in Estonia.

‘As Estateguru becomes among the first ones on our home markets to receive a licence, the company solidifies its position as a trusted and compliant crowdfunding service provider, both in the region and all of Europe,’ – added Mihkel.

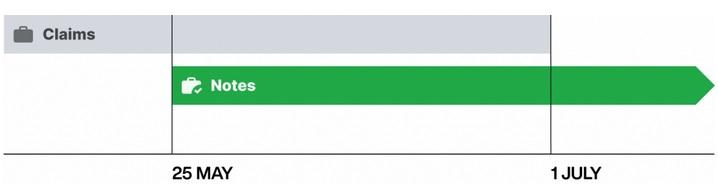

The long announced and several times postponed Mintos Notes product will finally launch on May 25th, Mintos* said yesterday. The notes are financial instruments and issued under the new investment firm license Mintos received last year. For each loan originator there will be a seperate prospectus (see example). Mintos mentions safeguarding of investor funds and notes under MIFID II requirements and increased transparency as investor benefits.

Until 30 June, investors can buy and sell investments via claims on the Secondary Market as usual. Then, from 1 July onwards, investors will be able to buy and sell Notes only, as a result of regulatory requirements.

The transition will mean two key changes for investors:

As the claims cannot be traded from July 1st onwards on the secondary market, investors will have to hold any claims in their portfolio to maturity

Mintos is required to deduct withholding tax depending on the investors country of tax residency and applicable double taxation treaties

My take

The transition will mean a major change for the marketplace that could either stiffle or empower Mintos growth. I expect that many investors will shy away from investing in very long term claims on the primary market in the remaining 7 weeks. Also buyer demand on the secondary market will likely decrease for the claims on long term loans. Potentially this will lead to offers with rising discounts before the trading of claims ends on June 30th.

There is some hesitation voiced among investors regarding the upcoming notes due to the withholding tax and surronding paperwork to claim possible reliefs and reductions (Mintos has announced that it will publish more information on the details). Mintos might try to offer some incentives in order for investors to take the leap and embrace the new product. I also imagine that Mintos will step up investor marketing again, once the notes product has launched. Already Mintos is taking a lot of effort to communicate and explain the coming changes via blog articles and newsletters.

This disruption might also increase the trend of loan originators setting up their own, unregulated investor marketplaces in other jurisdictions than Latvia.

Marketplace October* has just announced that due to regulatory requierements it won’t enable retail investors from Germany to invest into any new projects starting next week

In July 2019 we announced that we were going to launch October in Germany by the end of the year after the arrival of our local CEO, Thorsten Seeger. This is now coming fast with our first recruitments and operations in Munich.

For regulatory reasons we cannot open German projects to individuals. This is because the BaFin (German Federal Financial Supervisory Authority) requires the use of a fronting bank to allow retail investment in loans. We have studied this possibility, which has been chosen by other platforms, but the additional constraints and costs make this an unacceptable alternative under our business model.

German projects will only be funded by our institutional lenders (nor Spanish, Italian, French or Dutch retail lenders will be able to German projects). Additionally, lenders who are tax-resident in Germany will not be able to lend to any projects on the platform. Now that we operate locally, we have to apply local restrictions.

This means that you will not be able to lend on October as of next week. You will still be able to:

Receive repayments on your current projects,

Debit your October Account at any time.

We will provide you with your annual tax-summary (and this as long as you will be receiving repayments on your October Account).

We are really sorry to announce this news but have to comply with the German regulation. We have at heart to treat all our lenders, borrowers and partners equally wherever we operate. We will continue to work hard, with our peers in the European Crowdfunding Network, to allow German lenders on the platform in the future. How? We are confident that regulation, particularly at European level, will evolve to enable you to support the growth of European companies.

We are at your disposal should you have any questions.

Yesterday evening investors on the Collateral p2p lending marketplace were informed via email by a letter by Gordon Craig that he was appointed administrator for Collateral (UK) Ltd, the company running the marketplace.

The company is continuing to trade under his supervision, but will not be facilitating any new loans and the secondary market is closed at the moment. Reason for the company going into administration is given as ‘The Company was operating in the belief that it was authorised and regulated by the Financial Conduct Authority under interim permission. It has transpired that this is not the case and consequently the Company has ceased lending‘.

Most reassuring for investors into loans is, that he states: ‘Please note that your investment is safe and this is a procedural and compliance issue. … ‘

Investors into loans do not need to take any immediate action. ‘I have lent money via the Collateral platform do I need to do anything? No. Subject to the borrower continuing to make payments of interest and capital those will be returned to you in accordance with the Collateral terms and conditions.’

At a later point it was clarified that uninvested cash and money invested in loans without drawdown is also safe:’ I can confirm however that any monies that are sat on the platform and are not invested are ring fenced in a separate client account and the intention is for these to be returned to all investors after the Administrator has obtained control of the bank account and carried out a reconciliation.‘

As P2P-Banking has learned, the individual loans are bankruptcy remote, with security held by a separate security trustee – Collateral Security Trustee Ltd.

Collateral has lent about 17 million GBP since the start, most loans were secured by property.

So that are the positive points.

It remains unclear to me how Collateral could have misjudged the regulatory status? The interim permission seems to have lapsed on January 29th. Again it is unclear whether it was actively revoked by the FCA. Investors analyzed yesterday that Collateral had quitely removed references to FCA authorisation (e.g. from email footer) after January 30th. Worse yet the company seems to have changed T&C materially and investors complain they were not notified about any change of T&Cs.

There is also the question why it was allowed to continue to operate from January 29th to February 28th, if it did not have the necessary regulatory approval (anymore). And the lack of communication (prior to the letter of the administrator which is comprehensive) is a disaster (see my previous article). Putting up a server maintenance note for two days, when you are going into administration is not the right way to do it in my opinion.

The adminstrator has not decided if the website will go live again ‘We are currently looking into the website and the possibility of this being reopened in order for investors to view the balance of their investments, however this isn’t something that will be dealt with until next week at the earliest.’

Several other UK platforms have emailed investors and informed them about procedures in place to reassure them that they have taken all the necessary precautions to be prepared in case of a situation like this.

To sum it up, while it is very unfortunate that a platform goes into adminstration with a chance that eventually it will go out of business, it looks like investors into loans will get off fairly lightly.

According to the FT the FCA commented it was ‘aware of the issue and working with the firm‘. The role of the FCA in this happening leaves some questions open for debate at the moment.

On the majority of p2p lending marketplaces that accept non-resident international investors, the necessary process to comply with ‘Know Your Customer’ (KYC) rules involves multiple manual steps both on the side of the investor and on the side of the marketplace. After filling in details in forms the investor typically needs to submit scans (or photos) of an ID or a passport. As an investor I balk at the very few marketplaces that ask me to submit these via unsecured email. The better ones offer an upload inside the SSL secured website after login. The British marketplace typically also require a recent utility bill to confirm address.

Video ident

In continental Europe a few marketplaces are doing video ident. Recently when I registered at Paskoluklubas, aside from entering details in forms I needed to schedule a Skype video call in which I answered several questions and had to show my ID live. While it was straightforward, it is not more time efficient (both for investor and for marketplace). And I was lost for words for a split second when asked for my zodiac. How many non-native-english speakers can answer that question without hesitating for the right word (luckily mine is easy to translate). So there may be a higher drop off in conversion than in the document upload version.

I learned from Paskolulubas that they used video ident not to optimize the process but rather to fulfill Lithuanian regulation requirements: ‘In the end of last year in Lithuania … [a law was passed] which legalized digital identification …. There are just two legal methods to identify clients through digital technologies. The first one is to use special programs, applications or other measures to ensure that the photos execution process is continuous and that the photos transfer in non-real time would be impossible. The second one is video identification when [the] company directly could record customer and his ID document. We chose … [the latter] method because of the following reasons: a. easier control of quality with in house team and b. faster start’.

So Paskolulubas uses inhouse staff to conduct the video ident process.

Outsourcing KYC

In Germany video ident is also an allowed method of identification. And it slowly replaces the traditional Postident process, a longtime German proprietary solution, since it avoids media discontinuity. But usually the video ident process, while integrated in the website is outsourced to a specialized service provider.

Another example of outsoucing is the process Lenndy uses. When registering, all an investor is asked by Lenndy is his email address, nothing else. Then the investor is required to link an Paysera account with at least level 3. Either an existing one or a newly setup one. Paysera is a E-money institution with over 5 million customers. Lendy then imports the customer data, which have been verified by Paysera with the consent of the the customer. While this solution is elegant for Lenndy, Paysera receives mixed reviews by several German investors in p2p lending. But as the search for ‘Paysera’ in the last link shows, actually several p2p lending platforms use Paysera processes to some degree.

All of the above still require mainly manual labor for checking, even if some of the work is outsourced.

Automating KYC for international investors

Last week British Relendex moved from a manual document upload process to an automated process for investors of 7 countries; Australia, Canada, Denmark, Germany, Sweden, Switzerland. Relendex uses the Call Validate solution and checks (in case of Germany) first , middle, last name, gender, phone, address, city and postal code with the data coming from three different data sources and which Relendex says has high match accuracy. Relendex’s criteria was that the data available should be of equal quality and accuracy to that of the UK database.

A Relendex representative told P2P-Banking: ‘With the new process, international lenders from the nine countries could see their account be approved in a matter of minutes. Where previous manual checking could take a couple of days, the automated KYC process is much more efficient.’

Of course there are other solutions. I reached out to other companies for comment. But those who have automated are tight-lipped about details citing proprietary technology and competitive advantages.

Marketplaces that also use automation are welcome to comment and add to this story.

Linked Finance announced yesterday that it secured full approval from UK regulator:

I’m delighted to announce that we recently gained full authorisation from the Financial Conduct Authority in the UK. This approval is the culmination of a rigorous 2-year application process and a lot of hard work.

In the absence of any regulatory framework in Ireland, we originally began this process as a way to demonstrate our commitment to operating Linked Finance in line with best practice from the much more developed UK market.

This UK approval also opens several exciting avenues to us in terms of our plans for future expansion. It gives us the opportunity to attract lenders form the UK to support Irish SMEs. It would also allow us to start supporting SMEs north of the border, as well as paving the way for a full UK roll-out.

The P2P industry in the UK is the largest in the world on a per capita basis and platforms there are originating more than €1 billion in lending each quarter. It would be a logical next step in our evolution.

That said, our primary focus remains on Ireland and helping to grow the sector here as market leaders.

This authorisation in the UK won’t have any major impact on how you use Linked Finance but you may see some slight changes and modifications on the site, as we look to implement some of the various requirements, such as warnings and disclaimers, that would be required when operating in the UK.

The fact that we have gained full authorisation from the FCA should simply serve to underline that Linked Finance has developed the type of management processes and controls that are in line with industry best practice.

The timing couldn’t be better too.

This announcement comes as the Irish government have launched a public consultation in relation to regulating the sector here.

It’s a move that we wholeheartedly welcome. We believe that all platforms who want to operate in Ireland should be required to operate to the same high standards as Linked Finance.

Obviously, this approval from the FCA demonstrates that we are well ahead of the curve in the Irish market and we are encouraged that the Department of Finance is now considering a similar set of rules here.

We recognise that the development of P2P lending in the UK owes a lot to the introduction of government initiatives that promote the industry, including tax-free Innovative Finance ISAs and direct government lending to SMEs, via the British Business Bank, on platforms such as Funding Circle and RateSetter.

We would love to see the same type of support here and we will be using the current public consultation as an opportunity to promote similar initiatives in Ireland.

For our Irish lenders, this approval from the FCA in the UK should serve as further evidence of our commitment to developing a strong and stable platform that will continue to deliver healthy returns while providing much need credit to great local businesses.