On the Mintos p2p lending marketplace the majority of investors invest on the primary market into loans, either manually or via autoinvest. But for the 29% of investors that do invest on the secondary market picking loans presents them with a huge choice of about 125,000 offers (no typo, really 125K loan parts on offer!).

Main characteristics of the Mintos secondary market:

- no transaction fees

- selling at discount, par or premium, adjustable in 0.1% increments

- no minimum amount for buying, a buyer could make a partial buy of 0.01

- seller and buyer each get credited interest for the amount of days they hold the loan; that means seller continues to accrue interest for an offered loan until the part is sold

- good filtering

Sorting on the secondary market is preset to YTM (yield to maturity). This figure shows the yield the buyer would make (taking into account the discount or premium), if he would buy the loan and hold it to regular (!) maturity. Emphasizing regular is important since many of the buyback loans end prematurily, which would result in a higher than shown yield for loans listed at discount or lower than shown yield for loans offered at premium.

Generally YTM is a very good criterion for sorting an filtering on Mintos the secondary market and it is my most important criterion.

However there are exceptions, when taking the shown YTM at face value is not advisable.

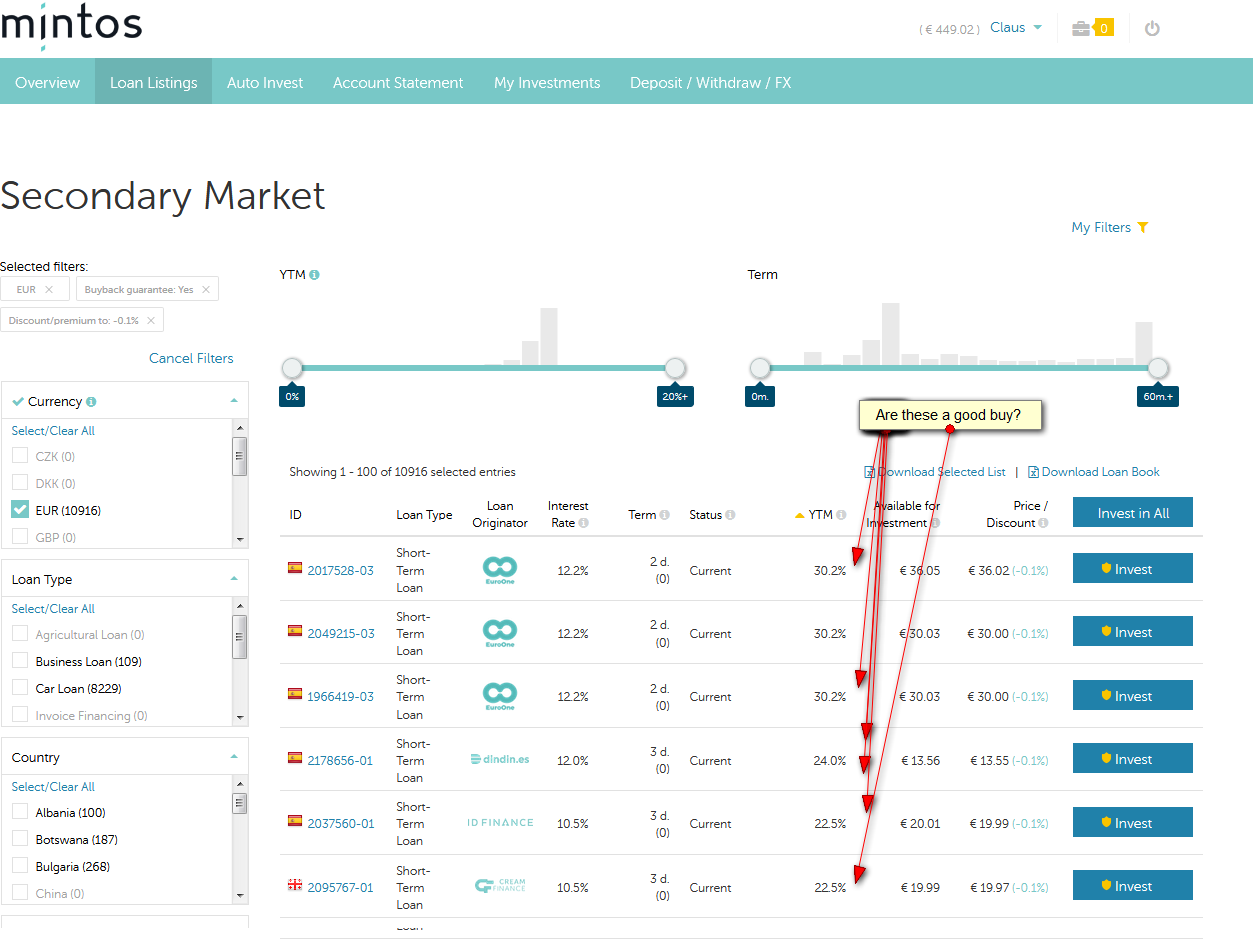

Click on image for larger view

Look on the loan offers in the screenshot above. All are offered at 0.1% discount and the YTM is very high with 22.5% to 30.2% Let’s neglect for the moment that picking these loans would cost the seller time, which if he puts a price tag on time spent would not be worthwhile as these loans are very close to maturity and he would only earn interest for a few days.

The high YTM is caused by the discount in combination with the fact that there are only 2 or 3 days left to regular end date of loan (term is 2d or 3d). The calculation is correct, but there is one caveat. For the shown loans there is a very high probability that they will miss the payment and therefore run an additional 60 days until they are repaid under the buyback guarantee. If that happens the remaining actual loan duration would be 62 or 63 days and the impact of the 0.1% discount on the YTM would be much smaller. The resulting YTM would be somewhere around 11 to 13%. So they would not be a good buy and there are much better offers on the secondary market.

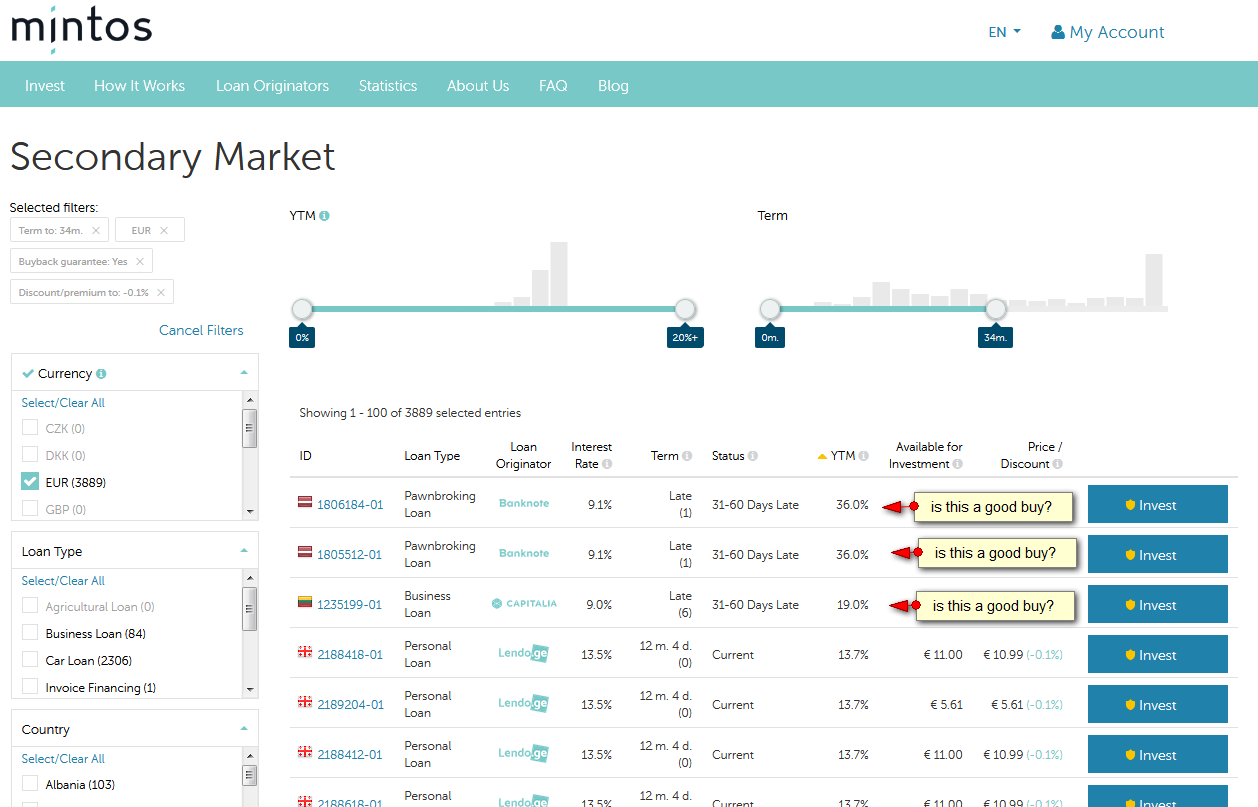

Another example to look at:

Click on image for larger view

These loans are shown with an even higher YTM of 36% and offered at a discount of 0.1%. They are late, but with a buyback guarantee, so aside from the originator risk there is no default loss risk. But for these late loans Mintos calculates the duration to the regular end of maturity with only one day, which in combination with the 0.1% discount results in the high YTM (simplified: 0.1% per days * 360 days results in 36% yield)

If I look into the details of one of these loans, I see that the next payment is actually scheduled in two weeks. So the loan will be repaid then since it is already in the status of 31-60 days late (there is a very low probability that it will repay earlier if the borrower repays).

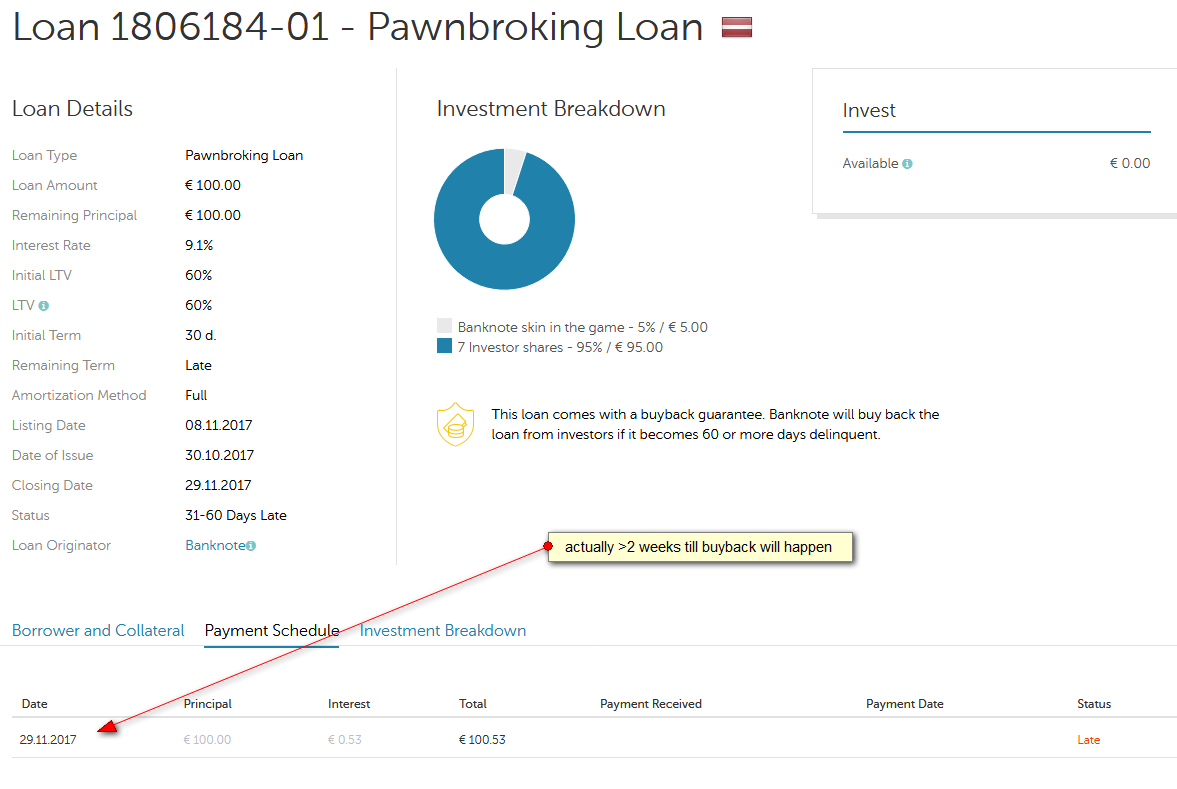

Click on image for larger view

With two weeks remaining the effective YTM for a buyer is not 36% but rather around 12%. Again there are offers with better YTMs on the secondary market.

Conclusion

On the Mintos secondary market YTM is an important figure to regard for buyers. However, while it is calculated correctly under the definition, there are a few cases where the shown figure alone might be misleading especially in case of loans that have less than 1 month remaining loan duration. The shown YTM always applies to the case that the buyer would hold to the loan to the regular maturity date.

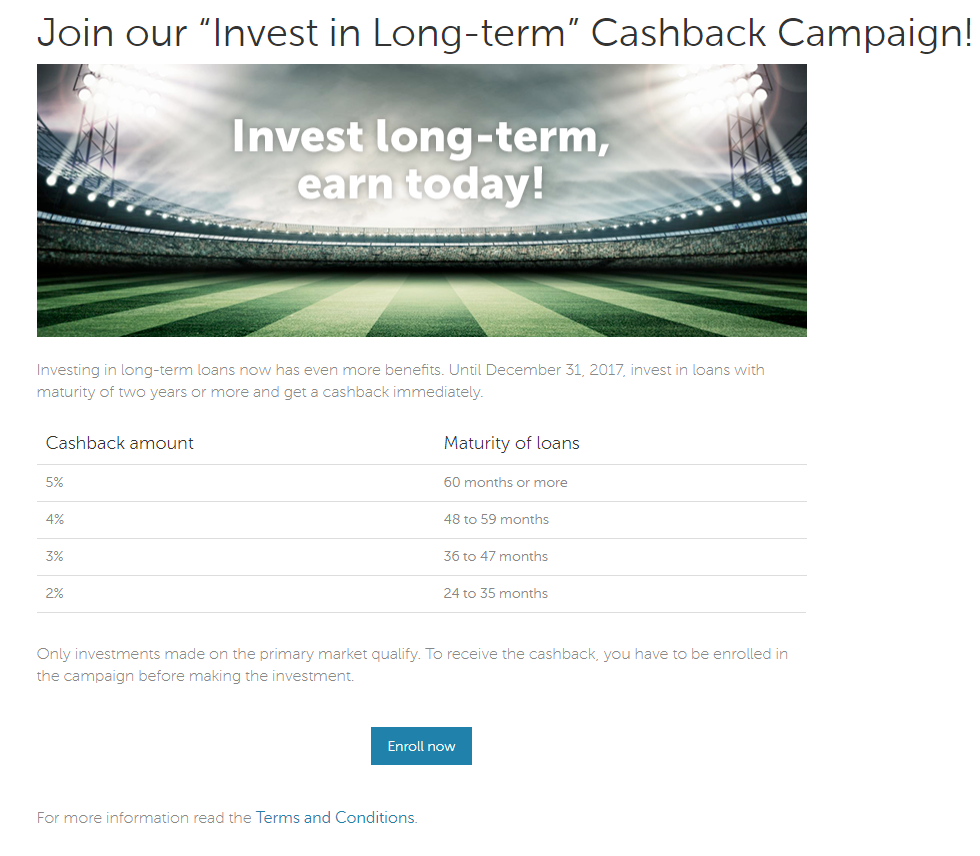

Not yet investing on Mintos? Get cashback.

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

More cashback offers are listed on the P2P-Banking p2p lending cashback list.![]()