One of the main developments in UK p2p lending this autumn is the IPO (initial public offering) of Funding Circle. It will be open for investors that commit at least £1,000 through an intermediary (see list of participating intermediaries). Investing at the IPO means investors will invest at a very late stage of the growth phase of a startup. This article and this article suggest that it might not be a good idea to invest in an IPO.

But is there really a chance to invest into equity of a p2p lending marketplace at an early stage, if you are not an employee, business angel or VC? Up to a few years ago the answer would have been NO. But crowdfunding for equity came into use a recently and a surprising number of p2p lending companies have used this route to raise funding.

In this article I will look at the p2p lending services that have used British equity crowdfunding platform Seedrs* to raise money. Some of these p2p lending company funding rounds have taken place years ago, but the interesting point is that Seedrs has a secondary market and new investors can buy shares from existing investors that invested earlier through Seedrs. The secondary market opens every first Tuesday of a month (next on Oct. 2nd) and stays open for a week. Some of the shares on offer are in high demand and often sell out within an hour. If you’d like to buy on the secondary market you should open your Seedrs* account now, as you’ll need time to verify it and deposit funds prior to the market opening.

P2P Lending Startups that raised funding rounds through Seedrs

Assetz Capital

Assetz Capital

Assetz Capital* is a UK platform for SME loans. Assetz raised two rounds on Seedrs for an aggregate of 5.3 million GBP. The last round was in October 2017 at a pre-money valuation of 50M GBP. Shares of Assetz capital are usually in high demand on the Seedrs secondary market.

![]()

![]() Brickowner

Brickowner

Brickowner is a UK property investment platform. Brickowner raised four rounds for an aggregate of 0.4 million GBP. The last round was a converible in March 2018. The pre-money valuation in Nov. 2017 was 2.5M GBP. There is usually some availability of Brickowner shares on the secondary market.

![]()

![]() Crowdlords

Crowdlords

Crowdlords is UK property crowdfunding platform. Crowdlords raised one round for 0.2M GBP in Nov. 2014. The current pre-emption round is at a pre-money valuation of 3.2M GBP. There is usually limited availability of Crowdlords shares on the secondary market.

![]()

![]() Crowdstacker

Crowdstacker

Crowdstaecker is a UK platform for SME loans. Crowdstacker is running a round right now for 0.8 million GBP at a pre-money valuation of 19.5M GBP.

![]()

![]() Crowdproperty

Crowdproperty

Crowdproperty is a UK platform for property development finance. Crowdproperty raised 0.9M GBP at a pre-money valuation of 5.9M GBP in November 2017. There is usually some availability of Crowdproperty shares on the secondary market.

![]()

![]() Flender

Flender

Flender* runs a platform for Irish SME loans. Flender raised on Seedrs round of 0.5M GBP at a pre-money valuation of 4.5M GBP in January 2017. Supply of Flender shares on the secondary market is scarce.

![]()

![]() Investly

Investly

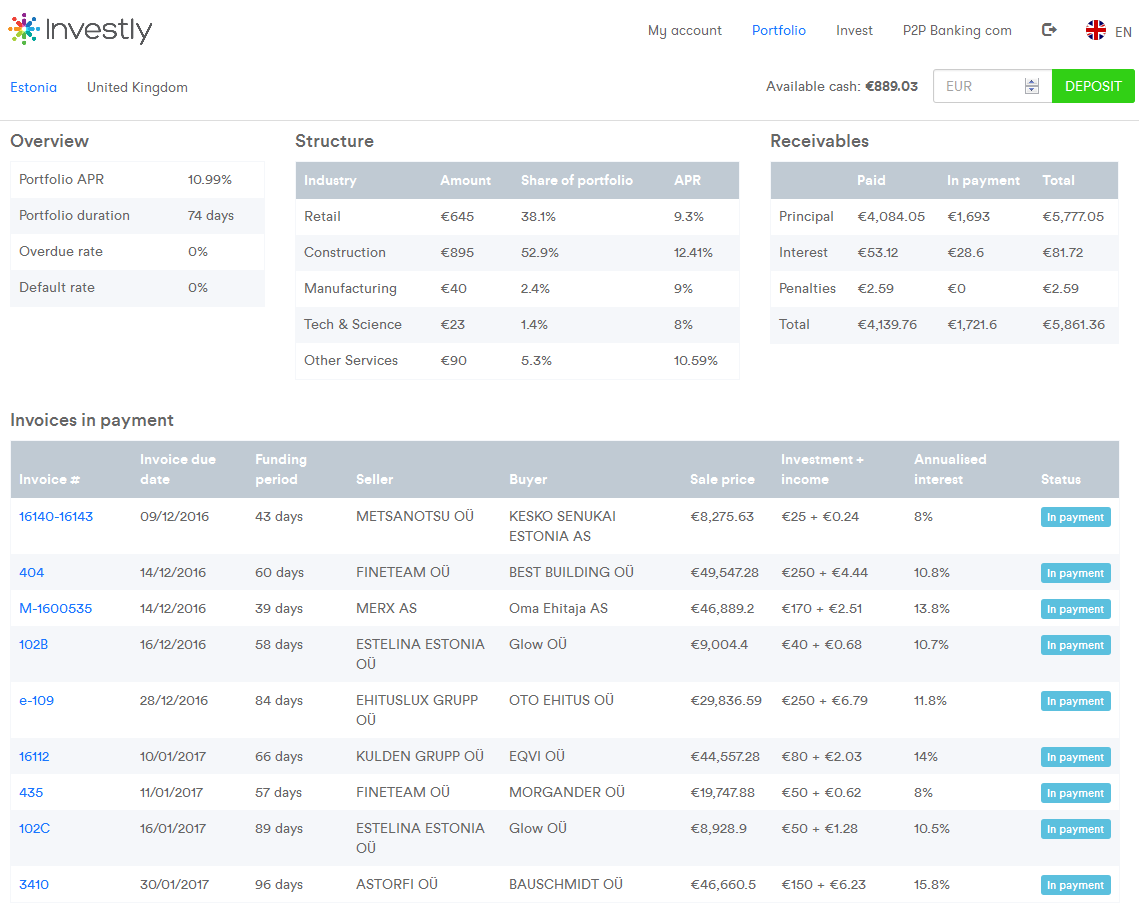

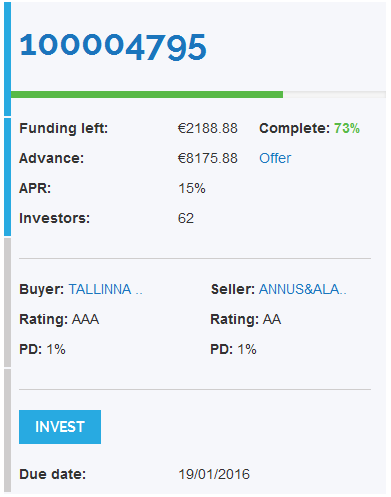

Investly* is a platform for invoice financing operating in the UK and Estonia. Investly raised on Seedrs round of 0.7M GBP at a pre-money valuation of 6.6M GBP in March 2018. Investly shares have been in high demand on the secondary market.

Landbay

Landbay

Landbay* is a UK platform for buy-to-let mortage lending. Landbay did multiple Seedrs rounds from 2013 till 2018. The last round was in March 2018 at a pre-money valuation of 28.9M GBP. There is usually good availability of Landbay shares on the secondary market.

![]()

![]() Orca Money

Orca Money

Orca is an aggregator for UK p2p lending investments. Orca is running a round right now for 0.5M GBP at a pre-money valuation of 1.8M GBP.

![]()

![]() Welendus

Welendus

Welendus is a UK platform for short-term loans. Welendus raised 1.3M GBP GBP through 3 Seedrs campaigns including the currently running round at a pre-money vaulation of 6.0M GBP.

There are shares of mulitple other interesting fintechs available on the Seedrs* secondary market, including Commuter Club which has an interesting connection to p2p lending: The loans for the transport tickets were financed first by Ratesetter lenders and now by Zopa lenders. There is usually good availability of Commuter Club shares on the secondary market.

P2P-Banking has a pre-launch notification service for upcoming new Seedrs campaigns. Sign up and you get a head start on new campaigns which might potentially include Assetz Exchange, a new Brickowner round and p2p lending startup Neo Finance.

Summing up: While there are other sources for shares in p2p lending companies, Seedrs is a good place to start looking.![]()

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.