Bondora announced today that the interest rate for the Go&Grow offer for investors will be lowered from 6.75% to 6% effective April, 1st.

Since the introduction of the Go&Grow product in 2017 the rate had been stable at 6.75% but in the last years there had been limitations on the maximum new amount that could be invested each month. Those limits were lifted temporarily last year. It will be interesting to watch how investors react to the rate change after the rate was stable for that long.

At launch Bondora Go&Grow was the only p2p lending marketplace offer with a single one click interest rate to investors where the money was available daily (subject to TOC). Later several other services launched similar offers.

According to P2P-Banking data, Bondora had 274,767 investors as of January 31st, 2024 and was growing by 2,000-3,000 new investors per month. The service is currently offering loans in Estonia, Finland, Spain, Latvia and the Netherlands and in the process of expanding into further markets.

Compared to the beginning of July the interest rates for newly issued EUR loans on Mintos are much lower now. While investors enjoyed interest rates of up to 13-14% for loans issued in the first half of the year, typical rates are 8-11% now, with a 12-13% for more exotic loans mixed in.

Cause of the change in market condition was that Mogo, one of the larger loan originators on Mintos, issued a bond worth EUR 50 million, with an annual interest rate of 9.5% (ISIN XS1831877755) on June 25, 2018 and Mogo announced that starting from July 13, 2018, Mogo would partially repurchase loans from investors on Mintos using their call option as stipulated in the assignment agreement. During July, Mogo plans to gradually repurchase in total up to EUR 16 million net of loans issued to borrowers in Bulgaria, Estonia, Latvia, Lithuania, Poland, and Romania.

Following the repurchase, the interest rates for newly issued EUR loans were sharply lower not only for Mogo loans but also for loans of the other originators on the Mintos platform.

This left most investors with a lot of cash in their accounts, as commonly 1/3 to 2/3 of all the Mogo loans in their portfolios had been repurchased and their previously configured autoinvests did not match any loans any more at their set interest rates.

To find out how investors reacted to the situation P2P-Kredite.com conducted a survey among German speaking Mintos investors. Here are the preliminary results (48 respondents):

35% say they withdraw uninvested cash and invest it on other p2p lending platforms

21% say they continue to invest on Mintos primary market

17% say they just wait, the interest rates will rise again

15% say they withdraw uninvested cash and invest it in other asset classes (e.g stock)

12% say they buy on the Mintos secondary market now, instead of using the primary market

For continental European investors looking for high yield alternatives here are 5 platforms that survey respondents liked:

Bondora Bondora is a long established Estonian company offering consumer loans in Estonia, Finland and Spain. Investors can choose between their new “Go&Grow” product (up to 6.75% interest) or the self-select autoinvest options with individual loans yielding much higher (nominal) interest rates

Estateguru Estateguru is a marketplace for property secured loans mostly in the baltic countries. Typical interest rates are 10-12%. Investors pick individual loans or enable autoinvest

Grupeer Grupeer is a young Latvian platform gaining popularity among the German investors. They list business and development loans in several countries (e.g. Latvia, Russia, Belarus, Norway, Poland). Typical interest rates are 14-15%

Peerberry Peerberry is a young Latvian platform listing consumer and property loans in several countries (e.g. Lithuania, Poland, Czech Republic, Ukraine). Typical interest rates are 11-13%

Robocash Robocash is a Latvian platform listing consumer loans in Kazachstan and Spain. Typical interest rates are 14-14.5%.

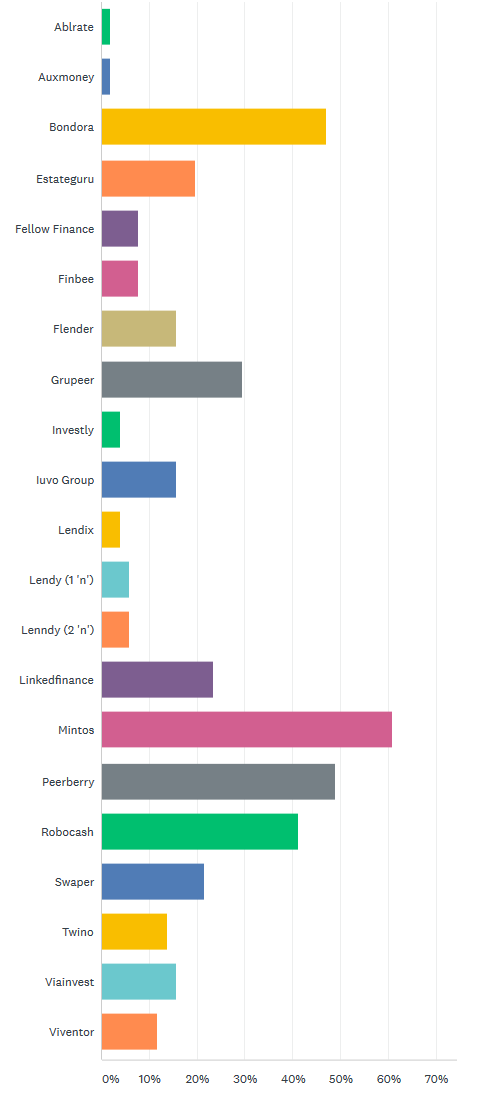

This selection is based on the likings of German speaking investors that voted in August for best p2p lending platform in a P2P-Kredite.com survey:

51 respondents, platforms that got no votes are not shown

The survey shows that Mintos is still rated number one in investor opinion among the queried audience, but the others are catching up (compared to similar surveys in the past).

My own Mintos portfolio shrank to less than 40% of its previous size as only less than 1/3 of the Mogo loans I had in early July are still in my portfolio. I withdrew a lot of cash and have transfered it to other p2p lending market places. Of course I’ll hold on to the my remaining Mogo loans as nearly all of them are at 13-14% interest rate.

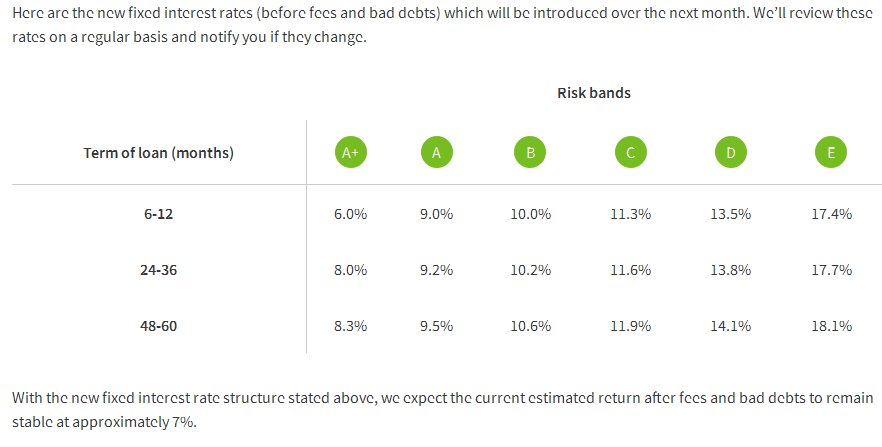

British p2p lending marketplace Funding Circle introduces a new model today. All new loans will be issued at fixed interest rates set by Funding Circle. Coming right after Funding Circle’s fifth anniversary, and 792 million GBP originated in loans to SMEs, the step to discontinue auctions is a major change in the way the marketplace operates.

Spokesman David de Koning told P2P-Banking.com that there were major drawbacks associated with the auction model for borrowers as well as lenders. Borrowers lacked certainty of the final interest rate until the auction period was over which led to some of them cancelling their loan application. Investors on the other hand experienced cash drag and sometimes had to make multiple bids to ensure they participate in the loan they wanted.

Under the new model Funding Circle will set the interest rate based on risk band and loan term. There will be 3 different rates for each risk bank. De Koning pointed out that the introduced model is not completly new for Funding Circle, as Funding Circle did already use fixed rates on property loans and on the US market of Funding Circle. Asked whether he expects loans to close instantly as demand could be higher than loan supply, he said he could certainly see loans to close quicker than before. The long term goal envisioned is that in future borrowers may pre-approve a loan before it is listed and it could close instantly once filled. Continue reading →

After looking on the p2p lending loan volumes, today I present an overview of average nominal interest rates for selected p2p lending services. As nominal interest rates are before fees they are easier to compare and an attempt otherwise would mean to list 2 rates for each marketplace (an APR for borrowers and a lender rate after fees). Of course nominal interest rates are in no way an indication to achievable lender yields as these are dependant – aside from fees -on defaults and recoveries occuring. Also on Wellesley actual lender interest rates are much lower than the quoted nominal rate.

What the chart does allow is to gauge the market segment the individual p2p lending marketplace concentrates on. But again this is only a first glance, for any further comparision any securities (like collateral, assets, or provision funds) have to be considered.

Table: P2P Lending nominal unweighted (*weighted) interest rates up to June 2014. Source: own research Some figures are estimates/approximations.

Notice to p2p lending services not listed: If you want to be included in this chart (or similar charts) in future, please email the following figures on the first working day of a month: total loan volume originated since inception, loan volume originated in previous month, number of loans originated in previous month, average nominal interest rate of loans originated in previous month.

Borrowers needing a small loan can turn to p2p lending marketplace Ratesetter, which matches borrower requests with funding supplied by private lenders. Borrowers can choose a variable rate loan (rolling loan) or a 36 months fixed rate loan. Nominal rates for the 36 months loan have fallen considerably in the past six months from approx. 9% to now under 7% (that translates to a representative APR of slightly under 9%).

Ratesetter has facilitated over 10 million GBP in loans since its inception.

Last week Ratesetter completed raising series C round of funding, raising 1.5 million GBP (approx. 2.35 million US$). The total amount raised so far is 3 million GBP.

RateSetter CEO Rhydian Lewis said: ‘…RateSetter is continually working to narrow the spread between what Savers can earn on their money and what creditworthy Borrowers can pay. This investment will ensure that customers will continue to get great value and a great service‘.

Microplace.com (an eBay company) initially started with interest rates of up to 3% on offer. Over time the highest offered interest rate has risen. Currently the highest interest rate offer at Microplace is 6%.