Ventus Energy*, a platform specializing in renewable energy projects in the Baltics has launched a campaign to celebrate its first birthday. The company is acquiring and running renewable energy production sites, like powerhouses, producing heat and electricity, wind parks, solar parks and battery energy storage systems. Interest is paid daily (or can be set to compounding by choice of the investor). The minimum investment is 1,000 EUR. Company data like energy production, revenue and capital structure is published on the website here and updated monthly.

I have invested small amounts in three projects a year ago and so far everything is running smoothly.

Now Ventus Energy* is running a cashback campaign offering 7-8% cashback on new investments. I copied the announcement below:

Earn 7%+ instantrewards on every new manual investment No pre-registration — just start lending Track progress live under the Birthday Campaign tab Bonuses stack with Invite & Earn + Affiliate rewards

Total Lending Pool: 7,092,024

Example: Invest 5k Euro get 350 instantly Invest another 5k later (total 10k) get +350 instantly = 700 total

Transparency disclaimers: Only new 16% projects qualify Early Exit projects excluded Bonus is paid instantly only when reaching a ladder threshold If Early Exit is used, the bonus is retracted proportionally for the uninvested period until project maturity

Terms and conditions apply – see website.

New investors signing up via this Ventus Energy* link get an additional 1% cashback on top for all investments in the first 60 days after registration.

At registration put WEALTH into the promo code field (was pre-filled when I looked).

Between August 28th and September 30th invest in notes, bonds, property and/or ETFs. The amount you invested on September 30th determines the size of the bonus (see table below).

The money has to stay invested until Dec 31st 2025.

Bonus will be paid out on January 10th, 2026

Full bonus terms are linked on the Mintos* website.

This translates to up to 2% cashback bonus in 4 months time.

I started investing over 10 years ago at Mintos* in January 2015. I am very satisfied with the results I achieved since. You can read all my previous Mintos articles on this blog.

Since last August I am investing on the Indemo* platform. In an earlier article I described in detail how Indemo works and why it was attractive to me. It has been going well so far. My portolio consist of 15 properties in 13 notes. Two further properties have already been successfully sold, yielding profits to investors including me that were well above the originally projected yield of 15.1% p.a.

Last week property A26 was sold, which gave me returns ranging from 15.9% to 24.2% (second column in the screenshot). The different yield numbers rsulting from the same property sale are due to the various different investment dates ranging from November 23rd to April 23rd (first column in grey). In this case the property was sold after only 7 month of being first listed on the platform meaning the success was achieved much quicker than the expected stated term of 24 month.

Click on screenshot for enlarged view

On the previous sale I had even higher yields ranging from 32% to 57% p.a.

Indemo Cashback Bonus

Starting today, Indemo* is offering new investors, that sign up via this Indemo* link 3% cashback on investments. Important: To get the cashback the new investor needs to enter the Indemo promo code “CASHBACK” (without the quotation marks) in the dedicated field during registration. Existing investors get 2% cashback. The cashback will be applied on all investments till July, 31st 2024. The cashback amount is credited instantly. I just invested 800 Euro in a note and as existing customer got credited 16 Euro.

Screenshot: This is how to enter the Indemo Promo Code CASHBACK at registration

Screenshot: I got my cashback for my 800 EUR invest credited instantly

added multiple new features on the website, including a dashboard and analytics section, better account statements, and better information on the object composition in new notes. I observed that Indemo is really aiming to implement features requested by investors to make the user experience better for the investors.

crossed 1,000 registered investors mark

announced 2 million EUR assets under management, saying that growth accelerated compared to reaching the first million EUR

added 3 new objects that are part of new notes offered

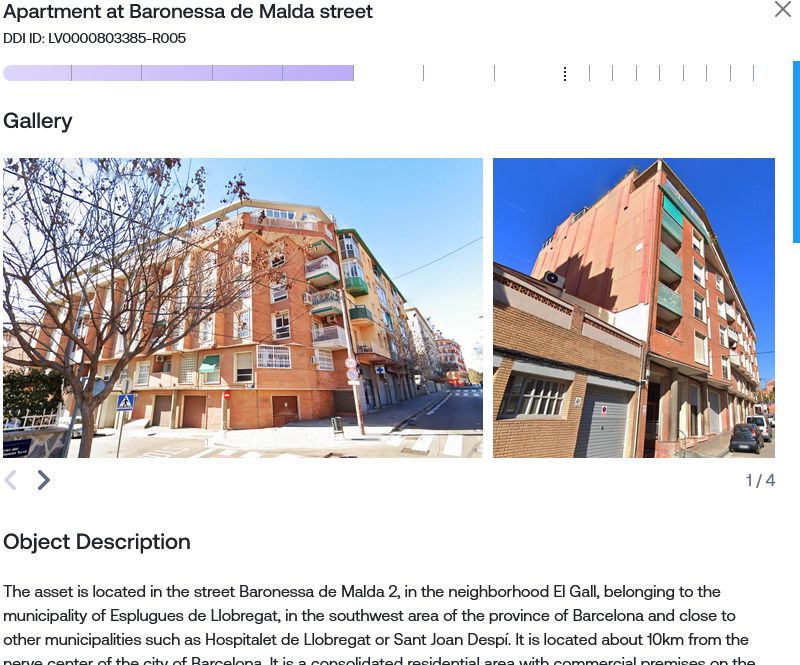

Screenshot: one of the recently added properties: an appartment in Barcelona

Most of the properties on the Indemo* platform are in towns on the Mediterranean coast.

British p2p property platform Kuflink* has been in operation since 2016. Previously accepting only UK residents as investors, the platform announced that they have enhanced their KYC/AML procedures and are now open to investors from anywhere in Europe. Interested investors can use a free UK bank account from Transferwise* Borderless or Revolut* (Smartphone required). And in exchanging money to GBP new TransferGo clients* can get a 10 GBP bonus when exchanging/sending at least 150 GBP.

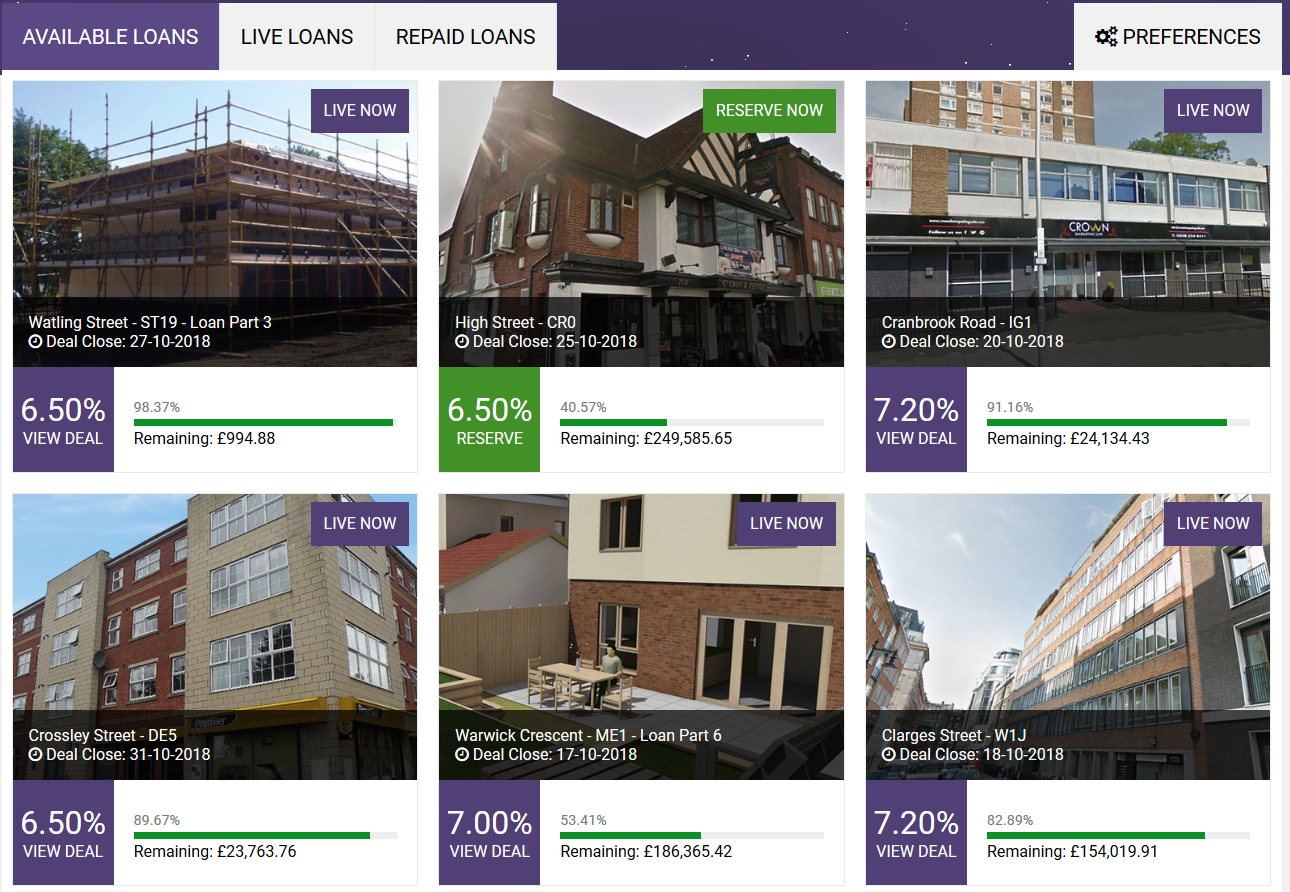

Kuflink* offers short term property loans (usually 3 to 12 month), secured by a legal charge. They run a very generous 100 GBP cashback offer available by signing up through this this link*. Note that the landing page says 50 GBP, but I have negotiated with Kuflink that clients referred by P2P-Banking get 100 GBP (doubling normal cashback). VERY IMPORTANT: Read T&C and strictly follow them. E.g. the minimum investment of 500 GBP must be reached within 24 hours of first investment. While it is possible to spread your investment over several loans, be sure that you are in line with the T&C terms. You can find more cashback deals on this page.

Screenshot: Available Kuflink loans (selection).

Every loan offer comes with detailed information, including a valuation report. Since the start in 2016, Kuflink has originated more than 20 million GBP in loan volume.

Kuflink* does not charge investors any fees. Interest is paid on the first day of each month (for manual investing). There is an autoinvest option, but conditions are less interesting than on manual investing. Two features Kuflink lacks are a secondary market and a detailed statistic page (there is some information in the FAQ).

On the p2p lending marketplace Mintos there is a very large and active secondary market. In my previous article I described that the YTM calculation shown on the secondary market is based on the assumption that the buyer holds the loan part till regular end of term and the buyer will achieve a higher yield, if he buys at discount and the loan is repaid prematurily.

In the article I will look into a possible strategy on the Mintos secondary market: buying overdue loans at discount.

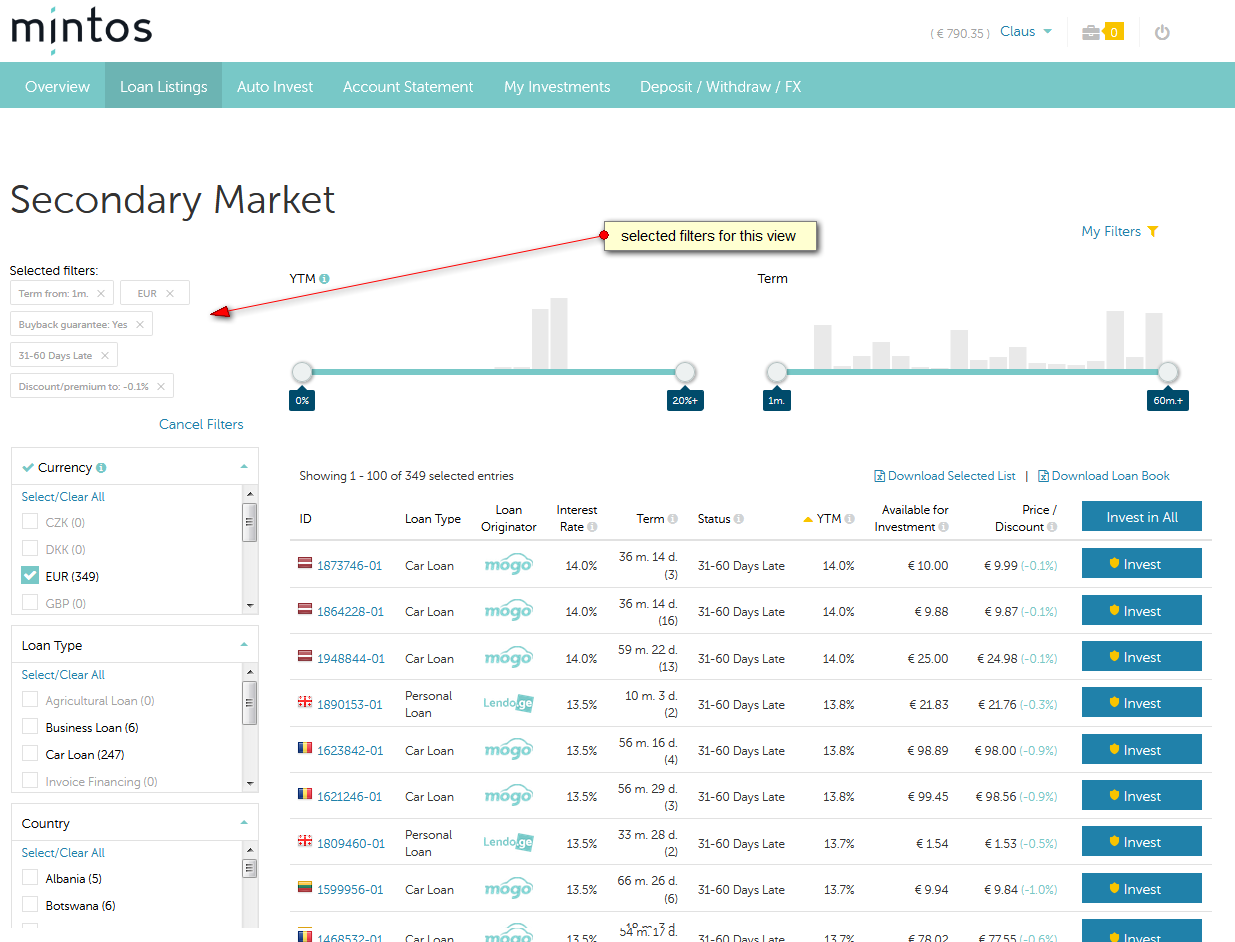

In a first step I sort/filter the buyback loans to only have those at discount that are very late (31-60 days overdue).

Click on image for larger view

I get a result of 349 loans with various discounts and an YTM of up to 14%. Not surprising for me, many of the loans listed at the top are Mogo loans. These are less attractive for buyers with this strategy. Why? Because they actually have a lower probability of defaulting. The paradox of this strategy is that the buying investor actually wants a high probability that the loans he buys default because that will boost his yield.

So in the next step I sort/filter to exclude Mogo loans. I also exclude loans that have a low YTM. This, because there is a chance that they do payup and then the buyer might be stuck with the loans for longer than 30 days.

Click for larger view

Finally let’s change the filter to require a minimum discount of 0.3% and there are 21 results:

Click for larger image

What would a buyer get?

If these loans do pay up and then run till regular maturity date, then he recieves a yield of 12.4% to 13.8%. Decent, but not very high compared to other Mintos loans.

However there is a chance of at least 50% that these loans will default and are bought back within the next 30 days. If that happens to a loan, that a buyer bought at 0.3% discount, it will boost his yield very roughly by more 3.6% (0.3% for 30 days multiplied by 12 to get annual effect). Likely it is more because the next payment date will be less than 30 days away. But even taking 3.6% the yield will be around 17%.

Looking at it, it is obvious that discounts as high as possible are preferable. The loan with the 0.6% discount would mean a boost of very rougly 7.2% yield on top (0.6*12). So that could lead to about 20% yield.

I have taken the screenshots for this article just at a random point in time. Higher discounts do happen and discounts of around 1% are not a rarity.

This is certainly not a strategy for a beginner at Mintos and it requires time and monitoring, but it is a frequently used strategy when investing on the Mintos secondary market.

Not yet investing on Mintos? Get cashback!

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

On the Mintos p2p lending marketplace the majority of investors invest on the primary market into loans, either manually or via autoinvest. But for the 29% of investors that do invest on the secondary market picking loans presents them with a huge choice of about 125,000 offers (no typo, really 125K loan parts on offer!).

Main characteristics of the Mintos secondary market:

no transaction fees

selling at discount, par or premium, adjustable in 0.1% increments

no minimum amount for buying, a buyer could make a partial buy of 0.01

seller and buyer each get credited interest for the amount of days they hold the loan; that means seller continues to accrue interest for an offered loan until the part is sold

good filtering

Sorting on the secondary market is preset to YTM (yield to maturity). This figure shows the yield the buyer would make (taking into account the discount or premium), if he would buy the loan and hold it to regular (!) maturity. Emphasizing regular is important since many of the buyback loans end prematurily, which would result in a higher than shown yield for loans listed at discount or lower than shown yield for loans offered at premium.

Generally YTM is a very good criterion for sorting an filtering on Mintos the secondary market and it is my most important criterion.

However there are exceptions, when taking the shown YTM at face value is not advisable.

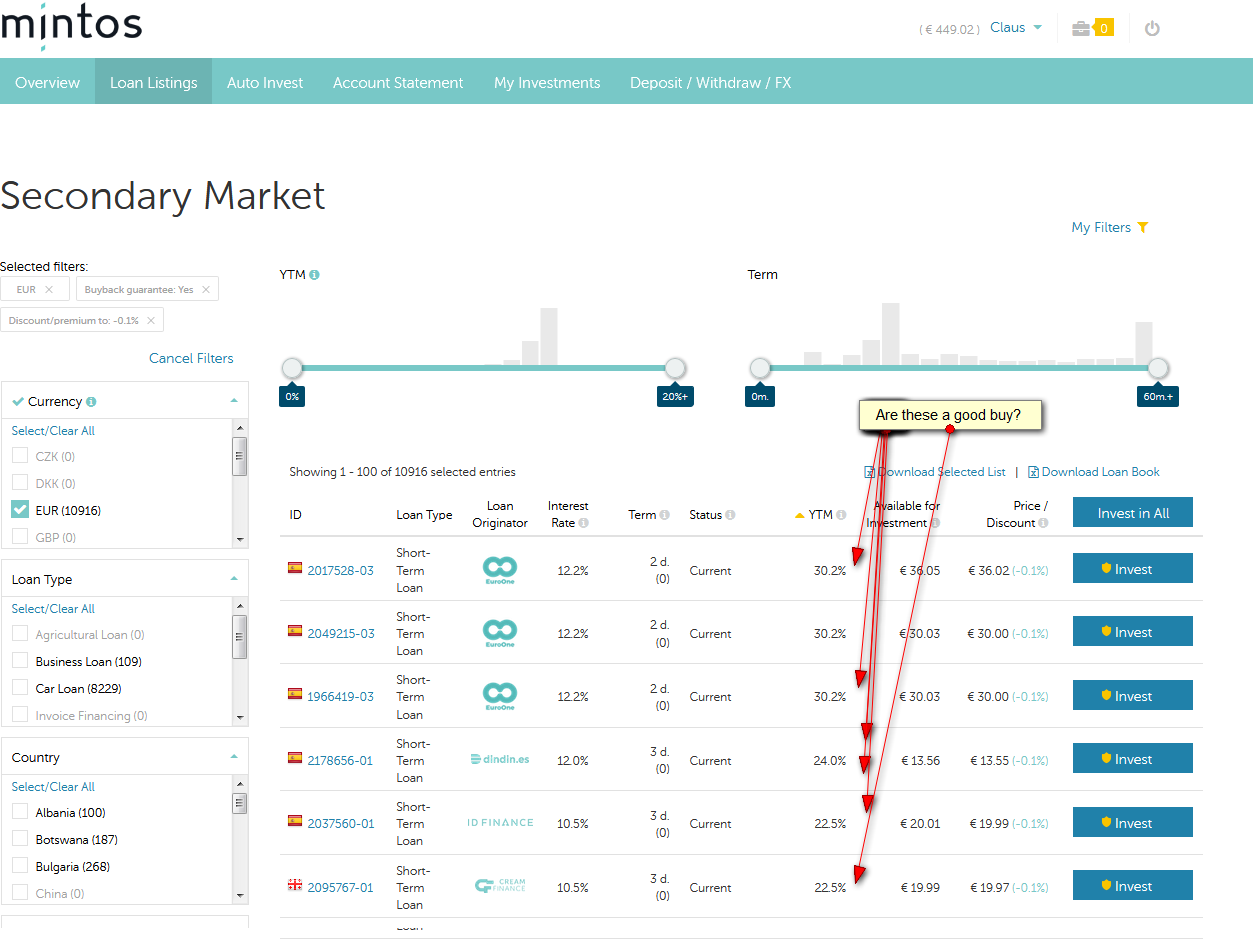

Click on image for larger view

Look on the loan offers in the screenshot above. All are offered at 0.1% discount and the YTM is very high with 22.5% to 30.2% Let’s neglect for the moment that picking these loans would cost the seller time, which if he puts a price tag on time spent would not be worthwhile as these loans are very close to maturity and he would only earn interest for a few days.

The high YTM is caused by the discount in combination with the fact that there are only 2 or 3 days left to regular end date of loan (term is 2d or 3d). The calculation is correct, but there is one caveat. For the shown loans there is a very high probability that they will miss the payment and therefore run an additional 60 days until they are repaid under the buyback guarantee. If that happens the remaining actual loan duration would be 62 or 63 days and the impact of the 0.1% discount on the YTM would be much smaller. The resulting YTM would be somewhere around 11 to 13%. So they would not be a good buy and there are much better offers on the secondary market.

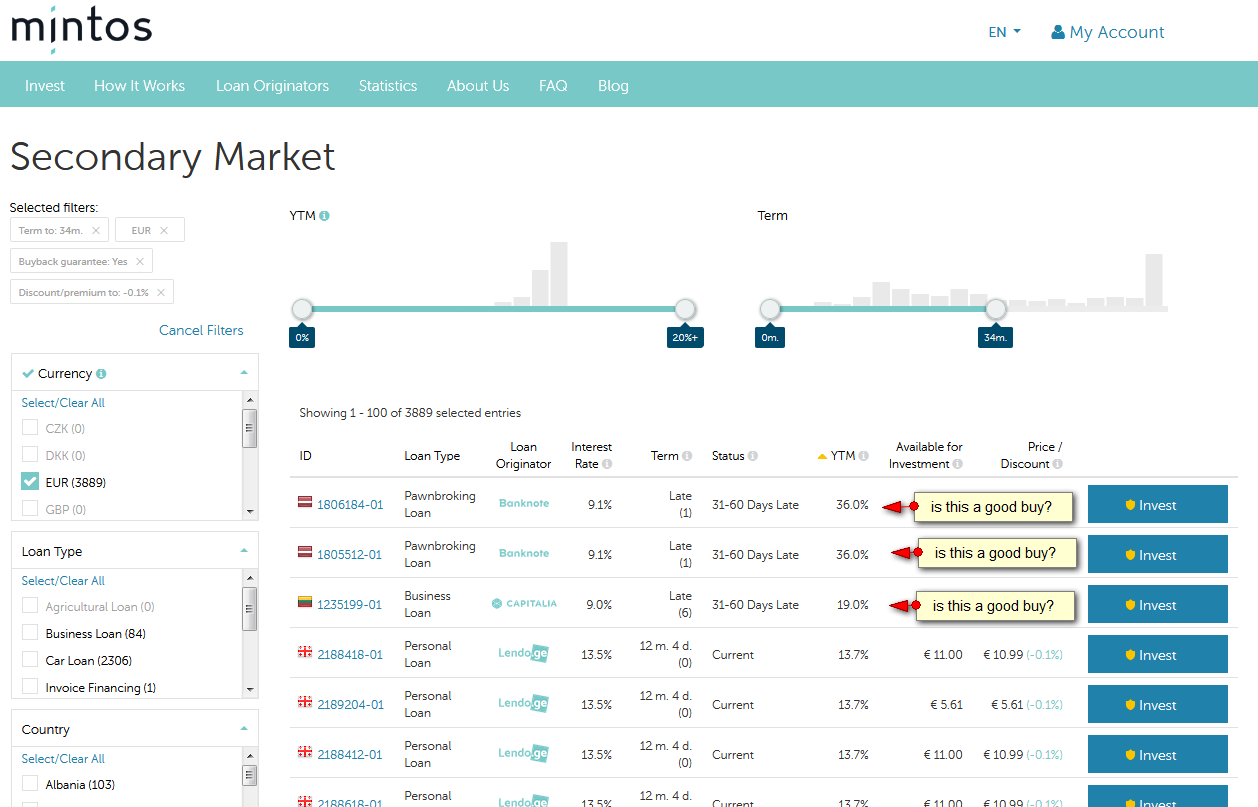

Another example to look at:

Click on image for larger view

These loans are shown with an even higher YTM of 36% and offered at a discount of 0.1%. They are late, but with a buyback guarantee, so aside from the originator risk there is no default loss risk. But for these late loans Mintos calculates the duration to the regular end of maturity with only one day, which in combination with the 0.1% discount results in the high YTM (simplified: 0.1% per days * 360 days results in 36% yield)

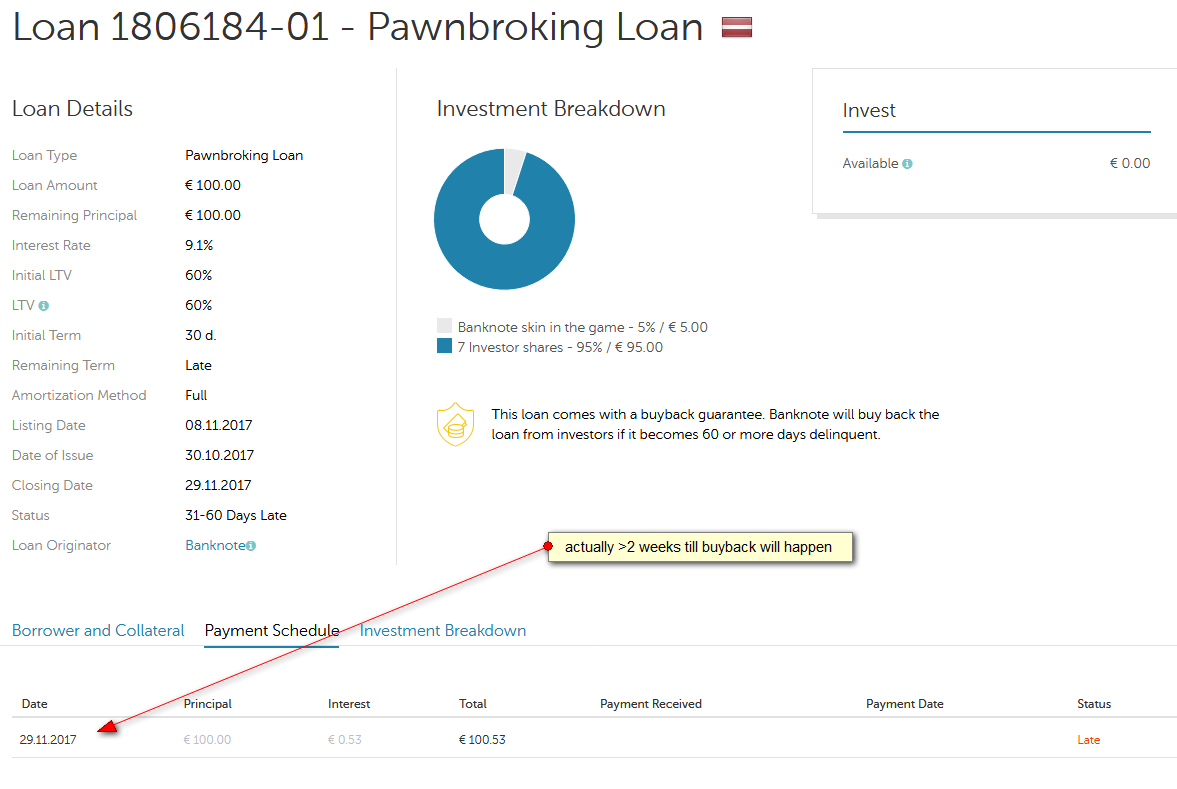

If I look into the details of one of these loans, I see that the next payment is actually scheduled in two weeks. So the loan will be repaid then since it is already in the status of 31-60 days late (there is a very low probability that it will repay earlier if the borrower repays).

Click on image for larger view

With two weeks remaining the effective YTM for a buyer is not 36% but rather around 12%. Again there are offers with better YTMs on the secondary market.

Conclusion

On the Mintos secondary market YTM is an important figure to regard for buyers. However, while it is calculated correctly under the definition, there are a few cases where the shown figure alone might be misleading especially in case of loans that have less than 1 month remaining loan duration. The shown YTM always applies to the case that the buyer would hold to the loan to the regular maturity date.

Not yet investing on Mintos? Get cashback.

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

Birthday Investment Campaign Launched – Quick Summary