British p2p property platform Kuflink* has been in operation since 2016. Previously accepting only UK residents as investors, the platform announced that they have enhanced their KYC/AML procedures and are now open to investors from anywhere in Europe. Interested investors can use a free UK bank account from Transferwise* Borderless or Revolut* (Smartphone required). And in exchanging money to GBP new TransferGo clients* can get a 10 GBP bonus when exchanging/sending at least 150 GBP.

Kuflink* offers short term property loans (usually 3 to 12 month), secured by a legal charge. They run a very generous 100 GBP cashback offer available by signing up through this this link*. Note that the landing page says 50 GBP, but I have negotiated with Kuflink that clients referred by P2P-Banking get 100 GBP (doubling normal cashback). VERY IMPORTANT: Read T&C and strictly follow them. E.g. the minimum investment of 500 GBP must be reached within 24 hours of first investment. While it is possible to spread your investment over several loans, be sure that you are in line with the T&C terms. You can find more cashback deals on this page.

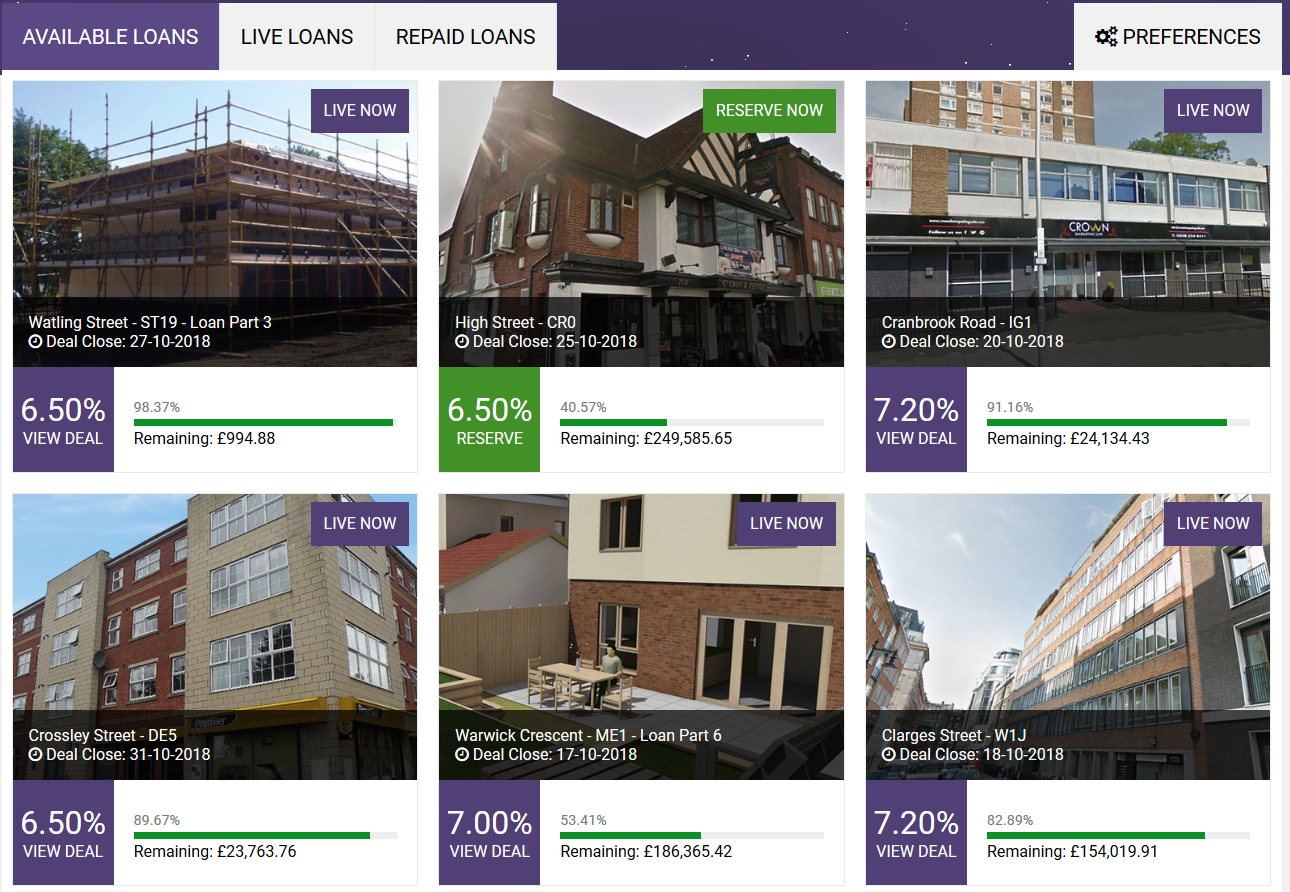

Screenshot: Available Kuflink loans (selection).

Every loan offer comes with detailed information, including a valuation report. Since the start in 2016, Kuflink has originated more than 20 million GBP in loan volume.

Kuflink* does not charge investors any fees. Interest is paid on the first day of each month (for manual investing). There is an autoinvest option, but conditions are less interesting than on manual investing. Two features Kuflink lacks are a secondary market and a detailed statistic page (there is some information in the FAQ).

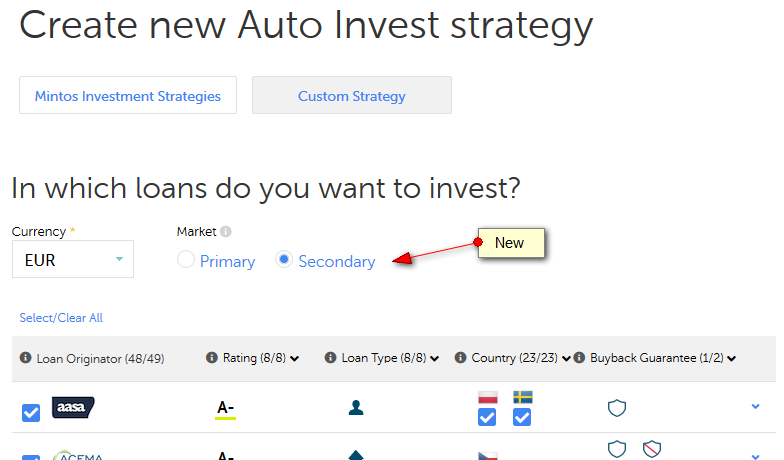

Mintos* has announced a new feature – the autoinvest can now be used to buy loan parts on the secondary market too. I am setting up a new autoinvest to test it and am curious how many loan parts I will be able to acquire with this new feature. Just like on the primary market there are many selections adjustable.

Screenshot Mintos Auto Invest Secondary Market

Mintos will roll out the new feature to all investors on Dec. 3rd. Only selected investors will be unlocked earlier. Mintos* says investors can deposit an additional 5,000 EUR to add to their balance to get early access. Also investorswhich have invested at least 50,000 EUR will have early access.

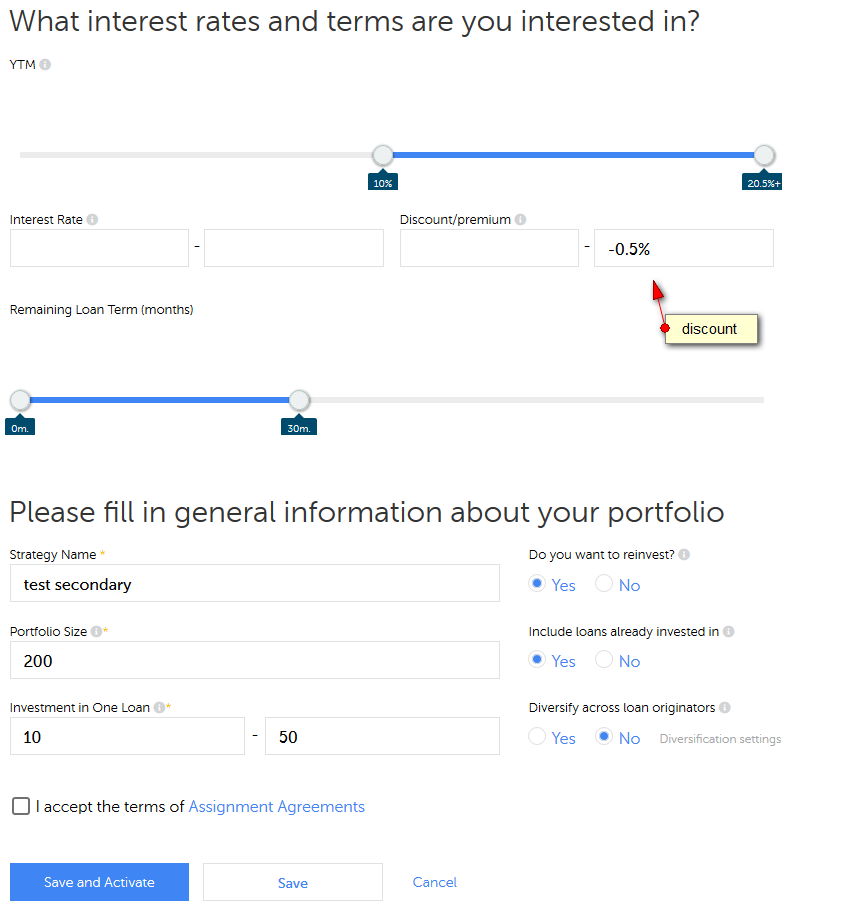

Screenshot: Further details of Mintos Auto Invest Secondary Market

For the further details of the test, I set the secondary market auto invest to buy loans with at least 10% YTM, a maximum loan term of 30 month and at least 0.5% discount. I left the interest rate open, as the restriction is not really necessary for me in this case in conjunction with the YTM and the discount.. For ‘Do you want to reinvest’ and ‘Include loans already invested in’ I choose ‘Yes’. I deselected ‘Diversify across loan originators’ as I want to buy all loans that match these conditions.

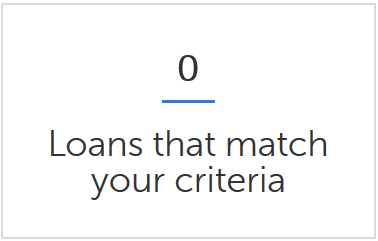

No surprise – no loans match my selection. Loans with these criteria selected by me have been bought up fast in the past, even before the introduction of this new autoinvest. I do wonder, which investor will get priority in case there will be autoinvests of multiple investors matching a new loan up for sale. I expect this new autoinvest will be a popular feature amongst Mintos* investors.

Not many but a few other p2p lending platforms offer autoinvests for their secondary markets too.

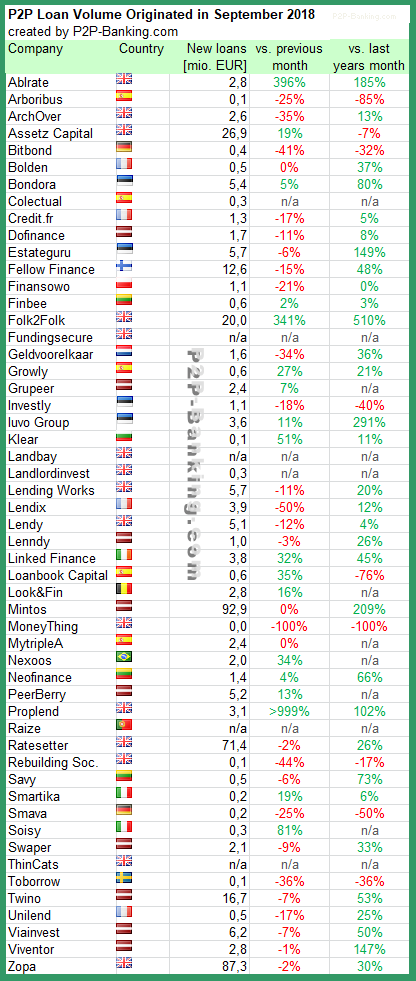

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 410 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Colectual* and Landlordinvest*.

Milestones achieved this month (total volume since launch):

One of the main developments in UK p2p lending this autumn is the IPO (initial public offering) of Funding Circle. It will be open for investors that commit at least £1,000 through an intermediary (see list of participating intermediaries). Investing at the IPO means investors will invest at a very late stage of the growth phase of a startup. This article and this article suggest that it might not be a good idea to invest in an IPO.

But is there really a chance to invest into equity of a p2p lending marketplace at an early stage, if you are not an employee, business angel or VC? Up to a few years ago the answer would have been NO. But crowdfunding for equity came into use a recently and a surprising number of p2p lending companies have used this route to raise funding.

In this article I will look at the p2p lending services that have used British equity crowdfunding platform Seedrs* to raise money. Some of these p2p lending company funding rounds have taken place years ago, but the interesting point is that Seedrs has a secondary market and new investors can buy shares from existing investors that invested earlier through Seedrs. The secondary market opens every first Tuesday of a month (next on Oct. 2nd) and stays open for a week. Some of the shares on offer are in high demand and often sell out within an hour. If you’d like to buy on the secondary market you should open your Seedrs* account now, as you’ll need time to verify it and deposit funds prior to the market opening.

P2P Lending Startups that raised funding rounds through Seedrs

Assetz Capital Assetz Capital* is a UK platform for SME loans. Assetz raised two rounds on Seedrs for an aggregate of 5.3 million GBP. The last round was in October 2017 at a pre-money valuation of 50M GBP. Shares of Assetz capital are usually in high demand on the Seedrs secondary market.

Brickowner Brickowner is a UK property investment platform. Brickowner raised four rounds for an aggregate of 0.4 million GBP. The last round was a converible in March 2018. The pre-money valuation in Nov. 2017 was 2.5M GBP. There is usually some availability of Brickowner shares on the secondary market.

Crowdlords Crowdlords is UK property crowdfunding platform. Crowdlords raised one round for 0.2M GBP in Nov. 2014. The current pre-emption round is at a pre-money valuation of 3.2M GBP. There is usually limited availability of Crowdlords shares on the secondary market.

Crowdstacker Crowdstaecker is a UK platform for SME loans. Crowdstacker is running a round right now for 0.8 million GBP at a pre-money valuation of 19.5M GBP.

Crowdproperty Crowdproperty is a UK platform for property development finance. Crowdproperty raised 0.9M GBP at a pre-money valuation of 5.9M GBP in November 2017. There is usually some availability of Crowdproperty shares on the secondary market.

Flender Flender* runs a platform for Irish SME loans. Flender raised on Seedrs round of 0.5M GBP at a pre-money valuation of 4.5M GBP in January 2017. Supply of Flender shares on the secondary market is scarce.

Investly Investly* is a platform for invoice financing operating in the UK and Estonia. Investly raised on Seedrs round of 0.7M GBP at a pre-money valuation of 6.6M GBP in March 2018. Investly shares have been in high demand on the secondary market.

Landbay Landbay* is a UK platform for buy-to-let mortage lending. Landbay did multiple Seedrs rounds from 2013 till 2018. The last round was in March 2018 at a pre-money valuation of 28.9M GBP. There is usually good availability of Landbay shares on the secondary market.

Orca Money Orca is an aggregator for UK p2p lending investments. Orca is running a round right now for 0.5M GBP at a pre-money valuation of 1.8M GBP.

Welendus Welendus is a UK platform for short-term loans. Welendus raised 1.3M GBP GBP through 3 Seedrs campaigns including the currently running round at a pre-money vaulation of 6.0M GBP.

There are shares of mulitple other interesting fintechs available on the Seedrs* secondary market, including Commuter Club which has an interesting connection to p2p lending: The loans for the transport tickets were financed first by Ratesetter lenders and now by Zopa lenders. There is usually good availability of Commuter Club shares on the secondary market.

P2P-Banking has a pre-launch notification service for upcoming new Seedrs campaigns. Sign up and you get a head start on new campaigns which might potentially include Assetz Exchange, a new Brickowner round and p2p lending startup Neo Finance.

Summing up: While there are other sources for shares in p2p lending companies, Seedrs is a good place to start looking.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

Finnish p2p lending marketplace Fellow Finance* plans an IPO at Nasdaq Helsinki. Established in 2013 and launching operations in 2014, Fellow Finance is an internationally active and growth-oriented FinTech group that provides crowdfunding services. The Company has facilitated peer-to-peer loans to consumers as well as loan-based crowdfunding and invoice financing to businesses in a total amount of more than EUR 295 million, serving nearly 430,000 users from around 50 different countries. Fellow Finance’s net sales consist mainly of commissions and interest income. Taaleri Plc is the largest owner of the Company, with an ownership of 45.7 percent before the IPO.

In 2017 Fellow Finance’s net sales was EUR 8.7 million, growing by 55 percent from the previous year. The good development continued in the first half of 2018, as the Company’s net sales grew by 43 percent compared to the same period of the previous year.

The objective of the planned IPO and Listing is to finance international growth and expansion of operations. Further objectives for the Listing are to increase the number of share-holders, give the Company access to capital markets, and in-crease the liquidity of the Company share and awareness of the Company. The Listing will also allow the more efficient use of shares as e.g. means of payment in eventual corporate acquisitions and in the remuneration of employees. The gross proceeds that the Company will receive from the Share Issue are estimated to amount to a total of approximately EUR 10.0 million, before IPO related fees and expenses.

Institutional investors consisting of certain funds managed by OP Fund Management Company Ltd and Sp-Fund Management Company Ltd as well as Prior&Nilsson Fund and Asset Management Ltd have given their pre-commitments to subscribe for shares and agreed to become cornerstone investors in the IPO. Additionally, the Company’s Chairman Kai Myllyneva, and members of the Board of Directors Esa Laurila and Jorma Alanne given their pre-commitments to subscribe for shares in the IPO. Total subscription commitments amount to approximately EUR 4.6 million.

Fellow Finance’s CEO Jouni Hintikka says: “We have created an advanced marketplace where we unite businesses and individuals looking for financing in Finland, Sweden, Germany and Poland with a global pool of investors looking for returns. Borrower customers are provided with peer-to-peer loans, business loans and invoice financing at market terms. For investor customers our services enable diversification of assets into an alternative asset class with minimum need of time and effort.”

Today I take a look at the recent development of investor numbers on several p2p lending marketplaces. I chart relative numbers with the index set to 100 for June 1st, 2018. The advantage of using indexed numbers for this comparison is that platforms use very different definitions for their investor base size. Some count registered investors, some count investors with deposits, some count active investors, some count recently active investors, … .

The disadvantage of showing indexed numbers for growth is that it gives smaller, younger an advantage as their percentage increase of investor base is likely still higher because they come from smaller absolut numbers. An example for this effect is Peerberry where percentage growth of investors is rapid, but the absolute number as of Sep, 1st has reached only 2468 investors as it is a very young marketplace.

Indexed investor numbers (with June 1st, 2018 = 100). Peerberry exceeds the choosen display scale – value for Apr. is 66 and value for Sep. is 183 Reading example: On Sep 1st the index value for Mintos was 123, meaning Mintos had 23% more investors than on Jun. 1st