There is an article in a German startup news magazine speculating that Funding Circle might have bought German p2p lending marketplace for SME loans Zencap from Rocket Internet or is in the process of doing so. The article does not provide any evidence but cites unnamed entrepreneural sources.

I reached out to both Funding Circle and Zencap for comment today but have not heard back yet. EDIT: I received a reply from Zencap that they do not comment on rumours/speculations. I also checked the filing history of the commercial register and there have been no telltale filings on the Zencap file in the past months, therefore I doubt a sale has been completed. But it still is a possibility because it likely would take some time for the filing to appear.

While I don’t have any hard facts either, I think the scenario has some plausibility. In emails I exchanged with a Zencap founder in the past months, there have been hints about upcoming major developments (without any specifics) at Zencap. Also it would match the intentions of Funding Circle to move into continental Europe. Continue reading →

This week UK p2p lending marketplace Ratesetter celebrates its 5th anniversary. When Ratesetter launched in 2010 it introduced the concept of a Provision Fund to p2p lending – an idea that has been adopted by several UK marketplaces since. The Provision Fund now stands at over £16m, the largest in the industry, and has ensured that so far no individual investor has ever lost a penny.

Since 2010, the fast-growing platform has delivered 815M GBP in loans to individuals, businesses and sole traders and expects to lend 500M GBP this year. While most loans are used to buy a car (28%), to pay off more expensive credit card balances (18%) and for home improvements (17%), RateSetter’s 160,000 loans have funded things as diverse as a mobile pizza kitchen that operates from the back of a Land Rover, a didgeridoo and a wind turbine.

Over 26,000 people currently invest with RateSetter, a number that is growing. In total, investors have earned 25M GBP in interest by using the platform. Continue reading →

German marketplace Zencap says the ‘Retail Investor Protection Act (Kleinanlegerschutzgesetz)’, passed into law in July 2015, is the main cause for a shortage of new loans on offer to retail investors on the platform. While Zencap welcomes regulatory guidelines, the company thinks that this law was not thoroughly thought out. Zencap stated: ‘For investors it is confusing that an investment into loans to companies for an amount of more than 100,000 Euro should be subject to different regulatory conditions than loans below that amount.’ (own translation from German original source).

While Zencap could offer loans regardless of size to retail investors in the past, it is has now restricted its offer to retails investors in Germany to loans up to 100,000 Euro as it would be forced to serve a prospectus (‘Vermögensinformationsblatt’) for which the borrowing company would be liable. Continue reading →

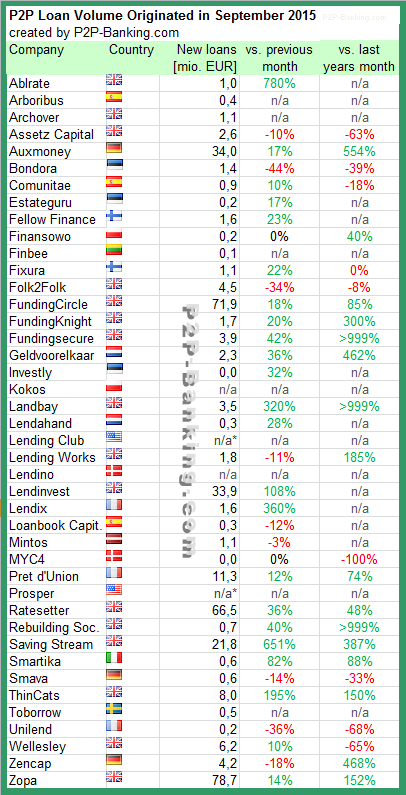

The following table lists the loan originations for September. Most marketplaces grew their loan volume compared to the previous month. Saving Stream had an exceptional month, with several very large loans. I added 4 new services to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in September 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Harmoney, the first p2p lending marketplace in New Zealand, has raised 200M NZD from P2P Global Investments fund (P2PGI) to launch in the Australian market. The agreement includes both debt and equity. In its first year in operation in New Zealand Harmoney already originated 100M NZD in loans to consumers. Continue reading →

GROUNDFLOOR is taking private real estate lending public. We’re paving the way to open a new $70 billion lending market to all – and that’s in single family home renovation and construction lending alone. You can read more about how we’re doing that here.

More broadly, we like to think of the company as an exposition on a theory of capital markets. We believe the broadest base of capital wins—because it’s faster, cheaper, more flexible and more efficient.

What are the three main advantages for investors?

GROUNDFLOOR makes real estate investing more accessible than ever before. We create new investment opportunities for non-accredited investors; a group of Americans that have never had access to these types of investments before.

Our typical loan term is dramatically shorter than what you see with P2P lending products like Lending Club. Our average term is 6 or 12 months, compared to 3-5 years for typical deals elsewhere.

We offer dramatically higher returns than traditional investments. During our one-year pilot in Georgia, the average annualized yield for our investors was over 12 percent. For context, that means that GROUNDFLOOR outperformed the compound average annual return of Charles Schwab’s mutual funds between 1970 and 2014.

What are the three main advantages for borrowers?

It’s fast and simple to get funded on GROUNDFLOOR. You can submit a project by checking your rate in less than 5 minutes. Projects have 30 days to fund, but most projects fund much sooner once they are posted. The closing process is quick and painless using the same closing attorneys you already use.

GROUNDFLOOR is a reliable source of capital. We fund construction, renovation and other loan types that are typically difficult to bank finance, and we offer low fixed interest rates starting at 6% (not including fees).

We offer terms that fit borrower needs. Most of our loans run from 6 to 12 months. Borrowers can repay their loan at any time to reduce borrowing costs, and personal guarantee and cross-collateralization is not required in most circumstances.

What ROI can investors expect?

GROUNDFLOOR backs independent builders with secured loans that pay 5-26% annually. During our one-year pilot in Georgia, the average annualized yield for our investors was over 12 percent.

What is the background of Groundfloor? Who are your seed investors?

GROUNDFLOOR was founded in February 2013 and is based in Atlanta. We have raised $2.5 million in seed funding from angel investors including Michael D. Olander Jr, Bruce Boehm, Tibor Nagygyorgy, Mark Easley Sr. and Inception Micro-Angel Fund.

Brian Dally is co-founder and CEO. He has spent his career building disruptive technology startups during stints in Silicon Valley, Boston, London and the North Carolina Triangle region. Previously, he led the launch of Republic Wireless to take on the big four cellphone carriers to international acclaim.

Nick Bhargava is co-founder and EVP of regulatory affairs. An expert in securities law, Nick was heavily involved in the JOBS Act as an early pioneer who advanced the concept of equity crowdfunding. Nick and Brian met through Groundwork Labs in the Triangle-area startup hub the American Underground. His years in finance have included work for the Financial Services Roundtable, SEC, FINRA, TD Waterhouse and RBC Financial Group. Continue reading →