The following table lists the loan originations for November. Funding Circle overtook Zopa measured by new volume followed by Ratesetter. I added two more platforms to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in November 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Lithuania will regulate p2p consumer lending starting February 1st, 2016.

The main requirements introduced by the new legislation in Lithuania are:

40K Euro of share capital required by the marketplace company,

contingency plan in case of failure of the platform,

limitation of 500 Euro investment per one loan,

limitation of 5,000 Euros investment per platform for ‘inexperienced’ investors,

marketplaces will be allowed to gain their revenue only from monthly instalments paid by borrowers. This means that all platforms will not gain revenue if their portfolio is not performing.

Laimonas Noreika, CEO of Lithuanian p2p lending company Finbee told P2P-Banking.com: ‘Once again Lithuania proved itself as a country with strict financial regulation. [The] new law gives more transparency to all – lenders, platform owners and public authorities. FinBee welcomes the regulation and invites international lenders to discover Lithuania as a country open for P2P lending.‘ Continue reading →

3rd party service LendingRobot today announces a partnership with Funding Circle in the United States, expanding the reach of LendingRobot’s automated investment technology beyond consumer loans and into small business lending.

Through the integration, individual investors using LendingRobot can set automated investment strategies for Funding Circle’s marketplace based on an extensive set of loan filtering criteria, and leverage the unified platform to manage their investments across multiple marketplaces, including Funding Circle.

“Introducing Funding Circle to the LendingRobot family of platforms demonstrates that our algorithmic investment strategies are extensible beyond consumer credit,†said LendingRobot CEO Emmanuel Marot. “The growth of peer lending as an investment vehicle is naturally encouraging an increase in the number and size of focused, vertical marketplaces. What we are building with this partnership is a unified view of all the major aspects of peer lending for investors, …â€. Continue reading →

Arboribus is the leading Spanish P2B lending platform that focus in more than 12 months loans for SMEs. Through our platform, High Net Worth individuals along with retail investors participate in directly lending to the most robust businesses in Spain obtaining a diversified portfolio with a net return around 7%.

What are the three main advantages for investors?

If I have to remark three advantages I would say a combination of a high net return along with a moderate risk and a total decorrelation from the financial markets: Returns from 5% to 7% when fix income securities or deposits returns are under 1%, with a moderate risk obtained by lending to the most creditworthy businesses in a very diversified way, and a total decorrelation from the ups and downs of the stock market. If I’m aloud to say a fourth advantage, I would pick “simplicityâ€.

What are the three main advantages for borrowers?

First, simplicity of the process of getting a loan: all on-line with a dedication from the business of no more than 15 minutes. Second, cost: for small businesses we are slightly cheaper than the funding obtained from traditional banks. And third, we permit the business to really diversify its funding sources and reduce risks of dependency from banks. That last advantage takes a special importance in Spain where SMEs have been traditionally dependent from banks for more than 90% of its external funding, a shocking figure if we look that of UK (30%) of France (50%).

What ROI can investors expect?

The actual weighted average interest rates on the platform is around 7%. Nevertheless, we expect to offer a 5% to 6% in a long term basis, net of fees and defaults.

How was Arboribus started? Is the company funded with venture capital?

Arboribus was founded by two friends (Carles and me). After one year of both dedicated full time to build the whole business, we got a first investment round and well after that we did the first crowdlending loan to a SME in Spain (that was July’13). Since there, we got two more investment rounds all covered by private investors (big business owners, bank managers and other business angels).

Is the technical platform self-developed?

Yes. We have in our team one programmer and almost the whole team is involved in improving our tools and developing new ones. Continue reading →

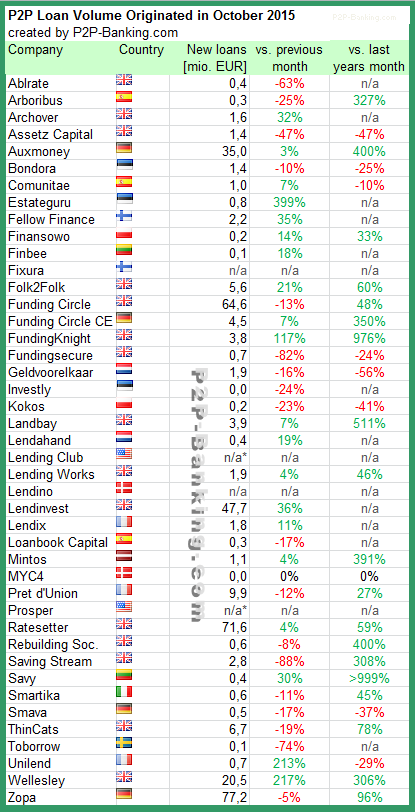

The following table lists the loan originations for October. Zopa is again leading by new volume followed by Ratesetter and Funding Circle. I added 1 new platform to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in October 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Lending Club reported the results for the 3rd quarter today.

Financial Highlights are:

Originations – Loan originations in the third quarter of 2015 were $2.24 billion, compared to $1.17 billion in the same period last year, an increase of 92% year-over-year. The Lending Club platform has now facilitated loans totaling over $13.4 billion since inception.

Operating Revenue – Operating revenue in the third quarter of 2015 was $115.1 million, compared to $56.5 million in the same period last year, an increase of 104% year-over-year. Operating revenue as a percent of originations, or revenue yield, was 5.15% in the third quarter, up from 4.85% in the prior year.

Adjusted EBITDA – Adjusted EBITDA was $21.2 million in the third quarter of 2015, compared to $7.5 million in the same period last year. As a percent of operating revenue, Adjusted EBITDA margin increased to 18.4% in the third quarter of 2015, up from 13.3% in the prior year.

Net Income – GAAP net income was $1.0 million for the third quarter of 2015, compared to a net loss of $7.4 million in the same period last year. GAAP net income included $13.5 million of stock-based compensation expense during the third quarter of 2015, compared to $10.5 million in the prior year.

Earnings Per Share (EPS)– Basic and diluted earnings per share was $0.00 for the third quarter, compared to basic and diluted EPS of ($0.12) in the same period last year.

Adjusted EPS – Adjusted EPS was $0.04 for the third quarter of 2015, compared to $0.02 in the same period last year.

Cash, Cash Equivalents and Securities Available for Sale – As of September 30, 2015, cash, cash equivalents and securities available for sale totaled $918 million, with no outstanding debt.

“We had another spectacular quarter, with revenue growth re-accelerating from 98% to 104%, and EBITDA jumping 181% year-over-year to reach 18.4% margin ,” said Lending Club founder and CEO Renaud Laplanche. “With over 1.2 million customers, continuously high customer satisfaction, strong credit performance, increased marketing efficiency and lower customer acquisition costs, we are continuing to observe tremendous network effects and benefits of scale. Our results this quarter combined with our raised Q4 outlook lead us to forecast a near doubling of revenue again this year and look toward 2016 with high confidence.”

Lending Club opened to retail investors in nine new states, bringing investor base, which is very sticky, to over 100,000. Small business loans grew in line with expectations.

Traditional banks do not benefit from network effects. Lending Club on the other hand does benefit strongly from network effects. All these dynamics lead to lower acquisition costs and higher margins.

From the Q&A of the earning call:

Decrease in returns (approx 1%) is due to network effects allowing Lending Club to pass some benefits in form of lower interest rates to borrowers. This is also enabled by high investor demand.

Custom loans are stable quarter of quarter. Lending Club has not transferred loans to the standard product.

Customer acquisition costs have not risen as Lending Club has invested early into the product and now benefits from it, e.g. through good customer ratings driving traffic

On the question if there is an increase on fraud attempts, Lending Club responded that there was no increase in attempts or frauds committed. Laplanche is not surprised that new platforms might experience a rise of attempts.

Does Santander exiting consumer loans have any impact on the relationship between LC and Santander? Santander was a great partner and accounted for a single digit percentage of volume. Lending Club has replaced Santander with other institutional lenders. The very diverse investor base of Lending Club is seen by Laplanche as a competitive advantage over newer platforms.

Madden has no direct impact on the investor base of Lending Club.

Are whole loans growing faster than originations? The mix is a function of the mix and appetite of the investors behind it.