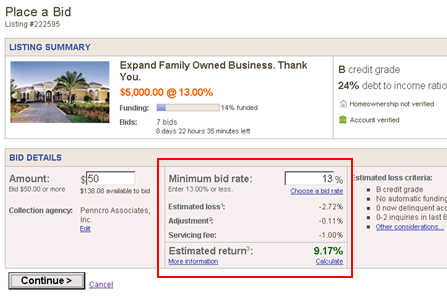

A p2p lending loan is one year into the 3 years loan term, the payments are current and the credit score of this borrower has improved a bit. Of the original amount of 10,000 US$ the remaining balance is 7,241 US$. Average interest rates on the p2p marketplace have dropped considerably since origination of that loan. Let’s also assume that from it’s data, the p2p lending service can gauge the probability and interest rate of a new loan with that credit score funding.

If the p2p lending service constantly monitors all running loans for their refinancing chances and then actively promotes a refinancing offer to those borrowers that have chances to lower their rates, there is a lot to gain:

- The borrower will be pleased that the p2p lending company offers a solution that could lower his rates

- The p2p lending company can earn origination fees again. This measure costs nearly nothing and therefore is much more cost-effective in generating revenue then market to attract new borrowers

- P2P lending services that are short on borrowers (surplus of lender demand) can generate new loans for lenders to bid on

- New lenders will find this loan attractive as the past performance record of this borrower shows that he pays on time.

The only disadvantaged party are lenders on the old loan. They lose the high interest rates for the remainder of the term.![]()

Process