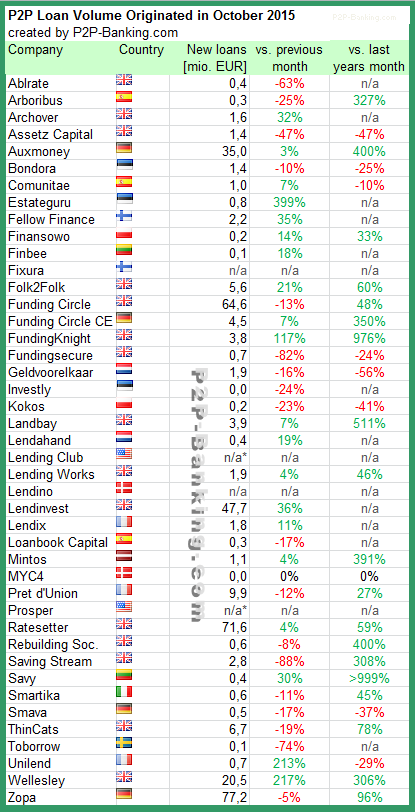

What is Arboribus about?

Arboribus is the leading Spanish P2B lending platform that focus in more than 12 months loans for SMEs. Through our platform, High Net Worth individuals along with retail investors participate in directly lending to the most robust businesses in Spain obtaining a diversified portfolio with a net return around 7%.

What are the three main advantages for investors?

If I have to remark three advantages I would say a combination of a high net return along with a moderate risk and a total decorrelation from the financial markets: Returns from 5% to 7% when fix income securities or deposits returns are under 1%, with a moderate risk obtained by lending to the most creditworthy businesses in a very diversified way, and a total decorrelation from the ups and downs of the stock market. If I’m aloud to say a fourth advantage, I would pick “simplicityâ€.

What are the three main advantages for borrowers?

First, simplicity of the process of getting a loan: all on-line with a dedication from the business of no more than 15 minutes. Second, cost: for small businesses we are slightly cheaper than the funding obtained from traditional banks. And third, we permit the business to really diversify its funding sources and reduce risks of dependency from banks. That last advantage takes a special importance in Spain where SMEs have been traditionally dependent from banks for more than 90% of its external funding, a shocking figure if we look that of UK (30%) of France (50%).

What ROI can investors expect?

What ROI can investors expect?

The actual weighted average interest rates on the platform is around 7%. Nevertheless, we expect to offer a 5% to 6% in a long term basis, net of fees and defaults.

How was Arboribus started? Is the company funded with venture capital?

Arboribus was founded by two friends (Carles and me). After one year of both dedicated full time to build the whole business, we got a first investment round and well after that we did the first crowdlending loan to a SME in Spain (that was July’13). Since there, we got two more investment rounds all covered by private investors (big business owners, bank managers and other business angels).

Is the technical platform self-developed?

Yes. We have in our team one programmer and almost the whole team is involved in improving our tools and developing new ones. Continue reading