Estonian property p2p lending marketplace Estateguru announced that it has secured its first institutional investor.

In March 2018, Estateguru signed the firm’s first institutional credit line to be invested in loans originated in the Baltic market with Germany based Varengold Bank AG.

Varengold Bank AG is a German private bank, headquartered in Hamburg. Founded in 1995 as an asset management boutique seeking to offer individual and high-performing financial products for private and institutional clients. In 2013, Varengold was granted a commercial banking license when it transformed into to fully fledged commercial bank.

Estateguru CEO and co-founder Marek Pärtel comments: “Establishing the EstateGuru – Varengold cooperation is a proof of having found a mutually beneficial cooperation model between a traditional financial institution and a fintech company. This is a clear sign that building a diversified portfolio of property backed loans is a very appealing instrument for institutional investors. Our Pan-European retail investor base is still the main source of capital. …”

Estateguru COO Mihkel Stamm adds: “Establishing a cooperation with Varengold Bank is an unprecedented assurance of the quality of EstateGuru’s business processes. The due diligence process was thorough and lengthy, during which Varengold’s representatives were convinced of EstateGuru’s product, procedures and the people behind the business.“

Since the establishment in 2014 Estateguru’s investor base of over 11 000 investors have funded in excess of 50 million EUR of secured property loans in Estonia, Latvia, Lithuania, Finland and Spain. With the recent developments, including entering 2 new markets in 2018 Q1, establishing an institutional credit line and an ongoing equity round, the firm is setting goals for the next European markets, to establish its Pan-European reach in coming years.

Kuflink is a peer-to-peer property investment platform that brings borrowers and investors together. Our borrowers seek quick access to short-term finance that a high street bank would be unable to deliver, and our investors seek competitive interest that beats the typical rates offered with regular savings and current accounts.

Investing in property has previously been reserved for the very wealthy, with the money and means to put significant sums towards developments. The fintech revolution, however, has opened up a wide range of opportunities to retail investors who want to make meaningful returns on their cash, and in turn, opened up borrowing opportunities for a range of projects that would previously be denied such quick access to loans.

Kuflink has built a peer-to-peer platform in this emerging space to give retail investors the opportunities that were previously only available to high net worth individuals and institutional investors. In doing so, it also offers developers bridging loans to fund projects across the UK.

Since our launch of the p2p platform in 2016, Kuflink lenders have invested over 17 million GBP, with 0.00 GBP losses to date.

What are the three main advantages for investors?

Firstly, investors are offered high rates of return associated with property investments, which due to the nature of the property market are often very secure and predictable. In this age of mass-market retail investment, property opportunities have one of the longest track records, as people have been investing in property for hundreds of years, and long before technological advancements allowed us to build an accessible P2P platform.

A second main advantage for investors is that Kuflink has a highly effective due diligence procedure with an exceptional track record. We’re so confident in our vetting of loan requests that we cover the first 20% of losses in each individual opportunity on the platform. We really believe in each loan, and investors can be confident in all opportunities, as like them, we trust the platform with our own funds at risk.

Thirdly, investors are only offered access to the very best opportunities, as Kuflink only approves around 30% of loan applications. This gives lenders peace of mind that their investment is very likely to be successful.

What are the three main advantages for borrowers?

We have been providing bridging and development loans since 2011 of up to 1 million GBP, and our lenders have invested over 17 million GBP in just under 2 years, proving highly advantageous for our borrowers.

Firstly, Kuflink gives property professionals highly competitive rates on development loans. Many of these highly secure projects may not otherwise find funding, as Kuflink’s due diligence process filters highly promising opportunities that others may incorrectly deem inappropriate.

Secondly, borrowers can access a huge number of investors through the p2p platform, and are provided with a highly regulated means of crowdfunding their projects. This allows developers to work on projects that people really want, and can help to build strong community relationships between loan backers and project managers, leading to increased opportunities for future project funding.

Finally, Kuflink’s on hand customer service team is highly responsive to any queries or difficulties with loans, and can offer instant advice and support in the event of any difficulties.

What ROI can investors expect?

There are multiple ways for investors to lend their money with Kuflink, and each of these carries different estimated ROI.

Using the Auto-Invest feature, the platform will automatically diversify investors’ funds, and can offer up to 5.35% interest pa gross*. Investors can also choose to invest in certain opportunities to have more control over their portfolio. This is through Kuflink’s Select-Invest feature, which can offer up to 7.2% interest pa gross* over shorter periods of time. Finally, our IF-ISA offering also allows investors up to 5.35% interest pa*, with a £20,000 tax-free allowance for 2018/19.

You are advertising “investors never lost a pennyâ€. At a future point in time defaults will happen. What is the procedure for dealing with these and what overall unrecoverable rate of debts do you expect?

In the case of defaults, we instruct an insolvency practitioner to recover funds, however we expect our excellent track record to continue and hope we won’t need to act upon this in the future.

Is the technical platform self-developed?

The platform has been developed by our CTO, Hari Ramamurthy, alongside in-house front and back-end developers to ensure the technology seamlessly compliments our P2P offering. Since our launch in 2016, the platform has been operating smoothly, while undergoing continuous updates and improvements. Our in-house technical team can respond immediately to any borrower or lender issues with the software.

How is the company financed? Is it profitable?

The Kuflink platform as it stands today has evolved from alpha bridging, which provided the funds for the launch of Kuflink Bridging, which hosted the initial P2P offering. Kuflink’s model, as with many P2P platforms, is to take a small cut from each transaction, and currently runs at a profit.

What were the main challenges when launching your platform?

One of the main challenges we have had to face is inter-departmental integration. With so many moving parts across different disciplines, from property due diligence experts, to finance and tech experts, making sure there are good lines of communication and correct pathways in place have been essential to our successful operation.

You offer an Innovative Finance ISA with tax advantages. Can you please provide some absolute numbers on how many UK investors have invested into this? And are there more new subscriptions or more transfers in of existing ISAs?

We currently have many IF-ISA account holders who have so far made significant investments. There has been a large influx of transfers in from other ISA providers from both new and existing Kuflink account holders, however we cannot comment on the exact number of account holders or investment value as these figures are commercially sensitive.

Is Kuflink open to international investors?

Our platform is open and accessible to overseas investors with a UK residency and a UK bank account.

Which marketing channels do you use to attract investors and borrowers?

We use a variety of marketing channels, from online advertising, to PR and even major sponsorship deals such as our partnership with Ebbsfleet United Football Club and their Kuflink Stadium.

What factors do you see impacting the British property market in the near future?

Brexit is of course a big issue that could potentially impact property in the UK, with an air of uncertainty surrounding the future of the market. Although we expect this to have a somewhat adverse effect on the markets, we believe that UK property will continue to be an attractive area of growth and investment, and should be relatively robust to any larger market perturbations.

Where do you see Kuflink in 3 years?

We currently have [a] positive outlook for the next three years, even in the face of uncertainty in the marketplace. Our trends show that there is a steady increase in loan applications alongside growing demand from investors for lending opportunities.

We also have plans to continue the work reinvigorating local communities around Gravesend and across the UK through the Kuflink Foundation. We hope to expand our charity and community work, which currently includes sponsorship of Ebbsfleet United, work with Kent County Council, and charities such as Age UK.

You have one wish, that the regulator would fulfil. What is your wish?

We work very closely alongside the regulator and are satisfied by their requirements. Our platform is fully functional within the current rules, and we find that these are more than sufficient for our platform to run smoothly, fairly, and profitably.

P2P-Banking.com thanks Narinder Khattoare for the interview.

Flender launched a year ago. What did you achieve since launch?

We have funded c. 1,300,000 EUR deals through our platform and we are proud that our defaults have remained at 0%.

We have just finished equity fund raise where we raised successfully 800,000 EUR from world’s biggest VC Enterprise Ireland and private investors.

We have strengthened our credit team with head of credit Colin Barry who came from AIB Bank and David McNamara ex director of Merrill Lynch International Bank. David has joined our credit committee and board of directors. This all means that our lenders can be assured that Flender has best in class underwriting practices.

Following due diligence, Price Waterhouse Coopers is heading our debt raise from institutional finance providers.

We offer very attractive 10-11.5% interest rate to our lenders. Current default rate is 0% and our world class credit team will ensure great returns to our lenders.

You now want to raise a 50M Euro debt package. What will that be used for?

Funds will allow:

Accelerate funding of the deals on our pipeline

Loans on our marketplace will get funded quicker

Offer bigger variety of credit options to borrowers such as higher ticket loans and property backed peer to peer loans

Can you please give details about the planned launch of property finance loans?

Our target market will be property developers and builders looking for working capital towards last phases of construction. Target loan size is 250,000-750,000 EUR.

How will these loans be secured?

Loans will be secured against 1st legal charge on the property

What interest rates can investors expect on the property loans?

8-10%

When will we see the first property loan listed on the marketplace?

We are aiming for May 2018

You recently repaid a convertible loan. Why did you decide to repay that loan rather than convert this into equity stakes in Flender?

This was condition of our new equity investor. Investment allowed us to repay our loan participants with very generous 12% return.

Flender holds permission to lend in the UK. How are your plans progressing to offer loans in the UK market?

Our plan is to expand and grow our brand in Ireland. We will review our launch plan for the UK towards end of this year.

What are the main challenges in growing the business right now?

Now that our platform and model have been proven then our goal is to scale up. We would need to grow both the number of retail lenders and involve institutional finance for this.

We welcome your readers to participate in campaigns on our marketplace.

Can you share some demographics on your (retail) investor base?

Ireland 58.41%

United Kingdom of Great Britain and Northern Ireland 14.86%

Germany 13.74%

You have one wish that the regulator fulfils for you. What is your wish?

We would welcome EU wide regulatory framework for p2p platforms.

Crowdestate is an Estonian p2p lending market place focussing on property. It is somewhat compareable to Estateguru or Lendy, the difference is that Crowdestate has a wider mix of offers, including unsecured debts or equity. I published an interview with the Crowdestate CEO last year.

The projects usually come with a term of 1 to 2 years, occassionally a bit long or shorter. There were not that many projects in the past . Often only 1 or 2 a month. Recently the pace has been picking up. Investor demand strongly outweights supply. Often the autoinvest bids fill a new offer instantly, if not then it is often filled within a hour of coming on the plattform. There are no fees for investors. Only a few offers pay interest during term, with most accruing interest to be paid at the end of the term. There are no fees for investors.

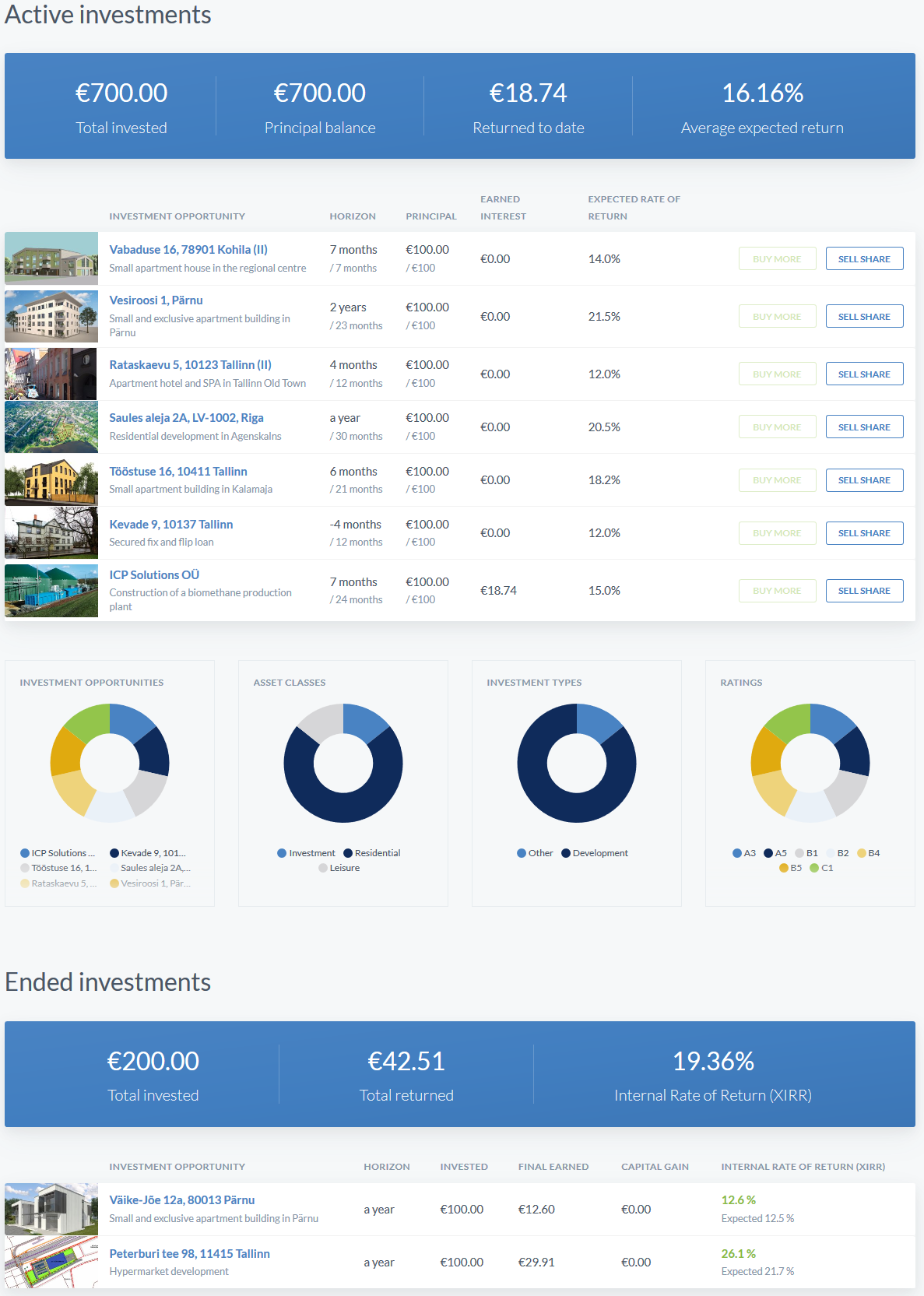

I only invested in a handful of projects to gain some experience. Today Crowdestate launched a new look for the website. This is how my small Crowdestate portfolio is displayed:

My Crowdestate portfolio – click for larger view.

Crowdestate secondary market

Today Crowdestate launched a secondary market. There is a “Sell Shares” button besides each of my active investments. To test it, I just offered one of my loans at a markup. The marketplace allows sellers to set markups or discounts.

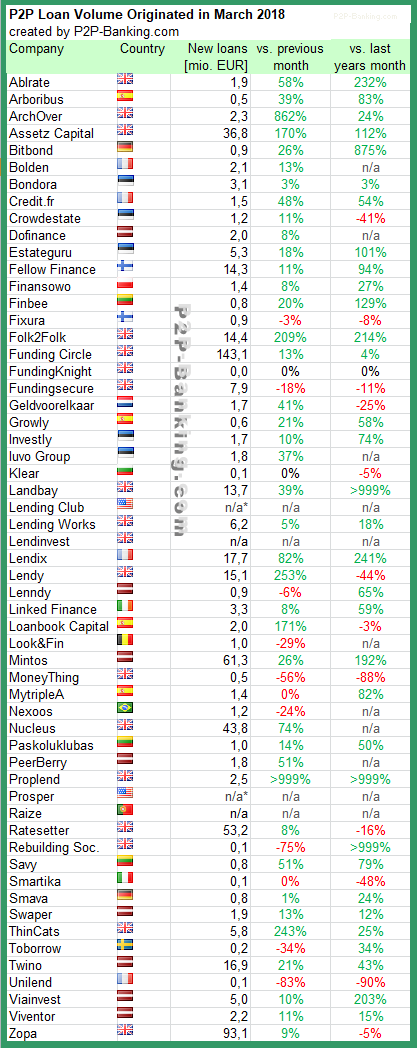

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Mintos, which is in the top 3 for the first time. The total volume for the reported marketplaces adds up to 599 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (overall volume since launch):

Table: P2P Lending Volumes in March 2018. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

LendingCrowd has secured an external funding round of 2 million GBP following a strong 2017 for the p2p lending company, with the proceeds earmarked for ramping up its sales and marketing activities.

The round was led by angel syndicate Equity Gap and included a number of private investors from Scotland’s entrepreneurial and finance scene, and the Scottish Investment Bank. The company says it is on track to scale significantly during 2018 and intends to seek Series A funding over the next 12 months.

As part of its drive to build market position, LendingCrowd this month launched its debut television advert, designed to bring the opportunities available through P2P lending to a wider audience. The advert features Geoff, who decided to “Think Outside The Bank†and invest with the platform after becoming disillusioned with the low rates of return on other investments.

LendingCrowd has originated loan deals totalling 16 million to SMEs across Britain in the past 12 months period. For 2018, CEO and co-founder Stuart Lunn has set a target to more than double loan deals to around 40 million GBP. New clients in 2017 included Summerhall Distillery, producer of award-winning spirits brand Pickering’s Gin, restaurant chain Tony Macaroni and property lettings agency Umega Lettings.

Investor funds on the platform have grown rapidly, with much of the expansion attributed to the launch of one of the first Innovative Finance ISA (IFISA) products in February 2017. After a full 12 months of opening the LendingCrowd Growth ISA, 82% of investors have beaten the advertised 6% target return.

LendingCrowd, which is fully authorised by the Financial Conduct Authority, has over 4,500 investors signed up to its platform and is on track to significantly increase investor numbers this year. It now offers three IFISA products – the passive Growth ISA and Income ISA, and the active Self-Select ISA.

Stuart Lunn, LendingCrowd CEO and co-founder, said: “Having laid solid foundations for the business over the last couple of years, we now have a position in the market that is starting to pay dividends. We have a strong pipeline of both investors and SME demand and with such a strong trajectory, we are now actively speaking to the venture capital and private equity communities about our next phase of growth.â€

Jock Millican from Equity Gap said: “We are extremely pleased that our syndicate members once again backed LendingCrowd, with this raise being the largest single investment by Equity Gap to date. Existing and new investors in LendingCrowd recognise the progress to date and the potential for the business to scale.â€

Kerry Sharp, Director of the Scottish Investment Bank, commented: “We are delighted to provide continued support to LendingCrowd who have demonstrated real market traction with their innovative peer-to-peer lending platform in Scotland.â€