UK property p2p lending marketplace Funding Secure was placed in administration today, Oct. 23rd, 2019. Jonathan Avery-Gee, Edward Avery-Gee and Daniel Richardson of CG & Co were appointed Administrators of the Company. No deposits and withdrawal requests from investors are currently processed anymore. More detailed information is provided in this FAQ.

Funding Secure provided roughly 315M GBP funding, mostly for property development loans, but also for pawn loans. The outstanding loan book stands at approximately 80M GBP. The accumulated loan book represents approximately 486 loans from about 3,500 investors.

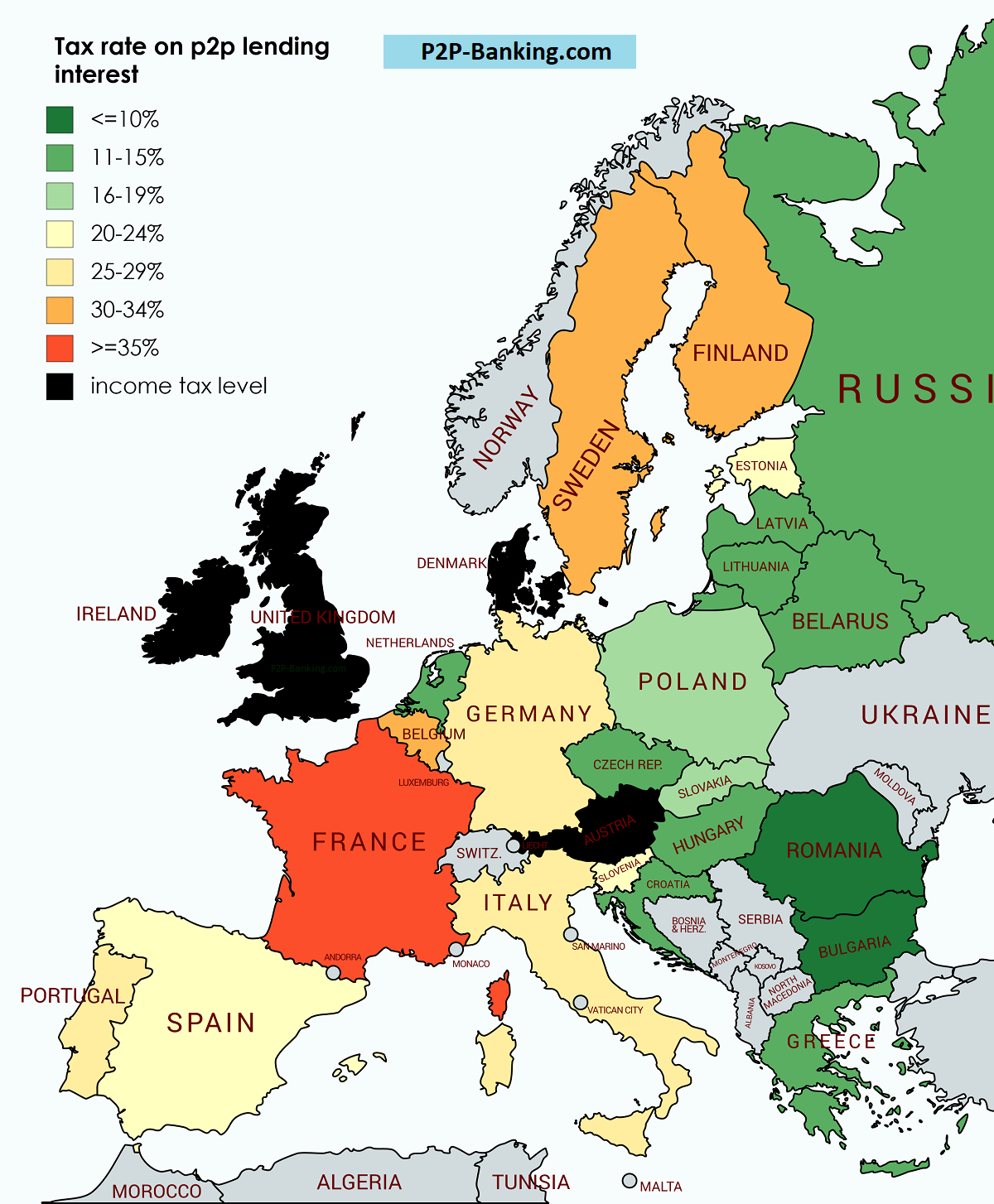

One important aspect for p2p lending investors is tax. In this blog whenever I talked about yields achieved, it is usually pre-tax yield. That is because taxation varies significantly from country to country. In most cases the place of residency of the investor determines the tax regime applicable. There are a few exceptions, e.g. on very few marketplaces withholding taxes are applied.

But I wanted to give a viusal overview on how different tax rates are for p2p lending investors, depending on where they live in Europe. Therefore I created for following map.

For overview purposes only. Source: own research – may contain errors or be outdated. Please note that this is a simplification and will not cover many cases. Do not make any decisions based on this, but rather consult a qualified tax advisor

In the countries colored in black the income tax rate is applied on interest earned on p2p lending investments. That means the individual rate of taxation depends on the other and overall income of the investor. For example in the UK the tax bands are 20%, 40% and 45% dependent on overall income. In Ireland tax bands are 20% and 40%.

But in most other countries there is a fixed rate applicable for interest earned on p2p lending. Tax free allowance up to a certain amount may apply. For example in Germany taxation (Kapitalertragssteuer)Â is 26.375% (a little higher if church tax applies).

Taxation is complex. Futher important points are whether defaults and fees can be offseted against interests earned. Also capital gains (e.g. from selling loans with a premium on a secondary market) may be taxed different than income.

Advantageous tax rules

There are many special tax rules and tax breaks. Consult a qualified tax advisor for information on your situation. Here are just some interesting examples.

UK: UK residents can invest through so called ISA products. There is a special IFISA (Innovate Finance ISA) which can be used to invest up to 20,000 GBP tax-free on peer to peer marketplaces. More information and an IFISA comparison is here. The interesting point is that the allowance is available per year. That means an investor using it in 10 consecutive years can invest 200,000 GBP tax-free into p2p lending.

Estonia: Many Estonians lend through a limited company (OÜ) they have set up. The advantage there is , that as long as the earnings stay in the company they are not taxed. Only at the time the profits are paid out from the company to the investor they are taxed at 20%. This allows investors to postpone the taxation for a long time.

Netherlands: The Netherlands are the only country in Europe where the tax is not based on actual p2p lending earnings, but rather fictual earnings. Wait. What? The tax system is actually a wealth tax, and the tax declaration is not based on income but wealth. The tax authority then assumes you earned a fictual income of 4% on your wealth. Tax rates used to be 30% on that (so 1.2% on your wealth; since 2017 it is now 0.581 to 1.68% dependant on amount of wealth). Now if you actually earned 10% ROI with your p2p lending your effective tax rate calculated on that would be 12% (30%*4%/10%). That’s what I used for simplification purposes in the map.

Portugal: In Portugal the rate is 28%. But if a foreign resident moves to Portugal and earns interest only from p2p lending market places abroad, he can profit from a 0% tax rate on these (providing the originating country does not tax the interest) for 10 years. Mark explains his personal experiences with this on obviousinvestor.com. There are non-resident/non-domiciled rules in other Euopean countries but they usually sound more complicated/restrictive.

Hint to platforms: It may be efficient to target countries in your marketing that have a high GDP but also a low or medium tax rate on p2p earnings.

European p2p lending services are growing. And yields of 10+% are achievable on some of the platforms. This attracts international investors. But if you are a US resident, you may have made the experience that you cannot register on some marketplaces. This is mainly due to KYC (know-your-customer) and AML (anti-money-laundering) requirements, which get more complicated if the client is outside Europe.

I have asked many of the European p2p lending marketplaces, whether they accecpt US residents and US companies as investors.

Here is an overview of 5 services (sorted aplphabetically) that do allow US investors. I have not provided a review for each of the service as the article would have gotten too long, but you can easily find news and reviews by entering the company name into the search box on the upper right of this blog.

On some platforms you need a bank account in the European Union. In most cases Transferwise* borderless or Revolut* will help (while technically e-money accounts, they function pretty similar to bank accounts) and do not charge any monthly fees. They are both very useful for currency conversion (Revolut is better). On Assetz Capital the currency is GBP. On the other marketplaces it is EUR. Mintos has additional currencies. Transferwise borderless is available in all US states except Hawaii and Nevada. Revolut* is currently rolling out the service in the US.

Mentioned new customer cashbacks were correct at the time of the publication of this article. If you are reading the article at a later time, it may have changed. A current list of cashback offers is here.

Assetz Capital

Assetz Capital* is a marketplace for UK SME and property development loans. The liquid ‘access’ products offer 4.1% to 5.75% interest. Other product types offer higher rates. US investors are welcome. UK bank is account required – see notes above. US companies are eligible, but verification might take longer than for individuals. Expect 1-10 days for company registration.

Assetz Capital cashback for new investors: 50-250 GBP (dependent on investment amount; minimum 1000 GBP). To get it just register using this link: Assetz Capital registration and start lending

Bondora

Bondora* is an Estonian p2p lending marketplace for consumer loans. The highly liquid Go&Grow product offer yields 6.75%. With other products higher yields of 10+% are achievable. US investors need to be accredited investors to use Bondora. A bank account in the European Union is not necessary. US companies are eligible to invest. Bondora recommends that interested US investors and companies contact them at investor@bondora.com or by phone at +44 1568 6300 06 (during business hours, Mo-Fr: 9–17 EET) to check eligibility and clear any questions concerning registration.

Bondora cashback for new investors: 5 EUR, to get it just register using this link: Bondora registration and start lending

Estateguru

Estateguru* is an Estonian marketplace for property loans. Typical interest rates are 10-12%. US residents are eligible, if they have a bank account in the EEA (European Economic Area) – see notes above. US companies can invest, if they have a bank account in the EEA.

Estateguru cashback for new investors: 0.5% (1% in October) cashback on all investments in the first 3 months. To get it just register using this link: Estateguru registration and start lending

Flender

Flender* is an Irish marketplace for SME loans. Typical interest rates are around 10%. US investors and US companies are eligible.

Flender cashback for new investors: 5% on all investments in the first 30 days after signup. Register using this link Flender registration and start lending

Mintos

Mintos* is a Latvian p2p lending market place. A wide range of loan types is offered. The fairly liquid ‘Invest&Access’ product currently promotes around 8% rate. Yields of 10+% are possible with manual and autoinvest.

US investors and US companies are welcome. A bank account in the EEA (European Economic Area is required) – see notes above.

Mintos cashback for new investors: 1% cashback on all investments in the first 90 days. To get it just register using this link: Mintos registration and start lending

The article was updated on Nov. 21st as Estateguru has meanwhile changed its position saying that Revolut or Transferwise are sufficient now to satisfy the requirements on a bank account in the European Union.

P2P lending bears high risks, including total loss of investment. This article is not investment advice.

A look back on the past 11 years, that saw the rise of numerous UK fintech players. How the financial crisis provided a hotbed for startups to foster and grow rapidly. The video by 11FS is an hour long and delivers and interesting recap. There is also a report.

Marketplace October* has just announced that due to regulatory requierements it won’t enable retail investors from Germany to invest into any new projects starting next week

In July 2019 we announced that we were going to launch October in Germany by the end of the year after the arrival of our local CEO, Thorsten Seeger. This is now coming fast with our first recruitments and operations in Munich.

For regulatory reasons we cannot open German projects to individuals. This is because the BaFin (German Federal Financial Supervisory Authority) requires the use of a fronting bank to allow retail investment in loans. We have studied this possibility, which has been chosen by other platforms, but the additional constraints and costs make this an unacceptable alternative under our business model.

German projects will only be funded by our institutional lenders (nor Spanish, Italian, French or Dutch retail lenders will be able to German projects). Additionally, lenders who are tax-resident in Germany will not be able to lend to any projects on the platform. Now that we operate locally, we have to apply local restrictions.

This means that you will not be able to lend on October as of next week. You will still be able to:

Receive repayments on your current projects,

Debit your October Account at any time.

We will provide you with your annual tax-summary (and this as long as you will be receiving repayments on your October Account).

We are really sorry to announce this news but have to comply with the German regulation. We have at heart to treat all our lenders, borrowers and partners equally wherever we operate. We will continue to work hard, with our peers in the European Crowdfunding Network, to allow German lenders on the platform in the future. How? We are confident that regulation, particularly at European level, will evolve to enable you to support the growth of European companies.

We are at your disposal should you have any questions.

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 639 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones in culumulative volume lent crossed this month: