I started investing in loans on the Latvian p2p lending marketplace Mintos right after it launched 12 months ago. At that time Mintos offered real-estate secure loans only. The service has evolved hugely with a much wider range of loan types on offer now. Mintos now serves as a platform to enable the transactions while partnering with loan originators, who actually originate loans and are responsible for vetting the borrowers.

Overview of the current main parameters for investors:

- Different loan types

- Typical interest rates range from about 8% to about 14%

- 0% fees for investors on the primary market (1% seller fee on the secondary market)

- All loans prefunded; investors earn interest from the day they invest money into a loan

- Depending on the provider, some of the loans offer buyback guarantees; that means if the loan becomes more than 60 days overdue the provider will pay the principal and the interest of that loan to the investor

- Open to international investors

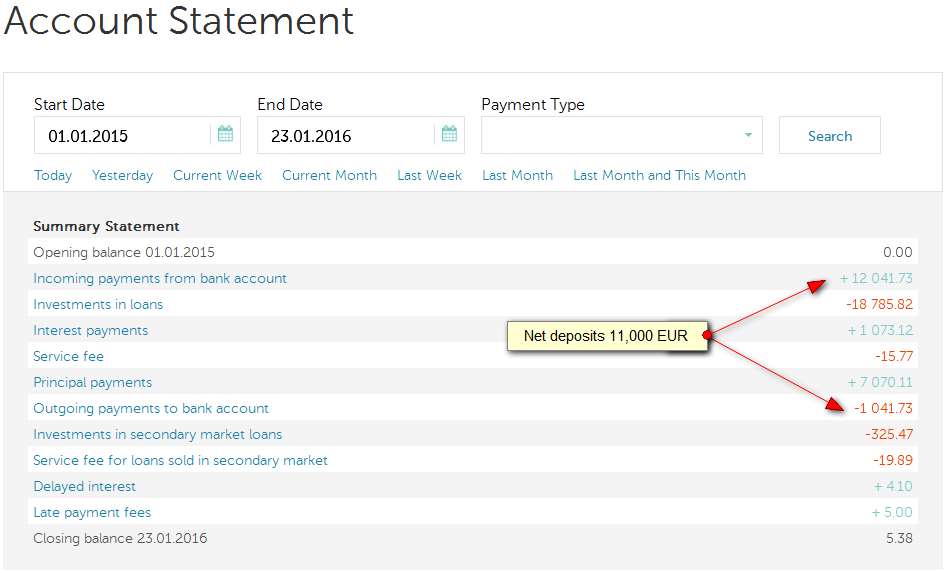

During the past year in several installments I deposited 11,000 Euro into the account via SEPA transfer (actually I deposited 12,041 Euro; but I also withdrew 1,041 Euro). Deposits are fast and reliable; they usually took less than 1 business day for me. Most of the time, I reinvested all repayments and interest earned.

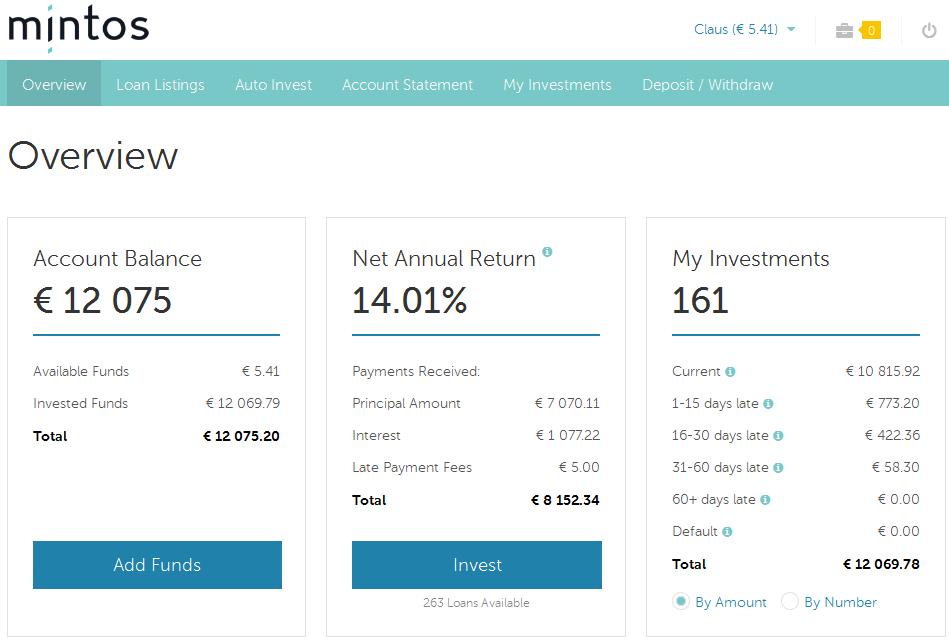

My portfolio yielded 14% ROI so far

Currently I have 12.069 Euro invested in 161 different loans. Over 70% of the amount is in Mogo secured car loans (with buyback guarantee). Over 20% is in mortgage loan (without buyback guarantee). The remainder is in business loans and invoice finance loans (mostly without buyback guarantees). I stayed clear of the personal loans Creamfinance originated in Georgia. The shown 14.01% are an accurate reflection of the actual ROI, I believe.

My strategy

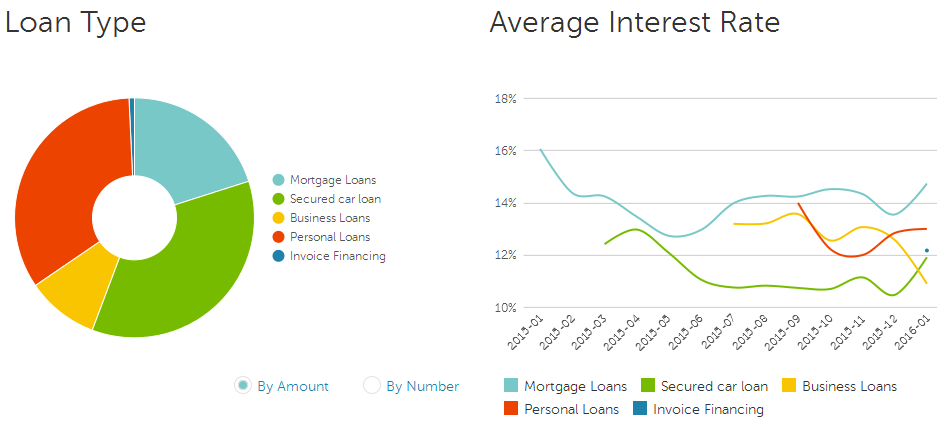

Beating the average ROI of 12.5% is less of a personal achievement, but more due to the fact that I started early on Mintos. In the early days there were only mortgage loans and most of these carried interest rates well over 15%. I still have over 20 active loans from that time with interest rates of 15% or more in my portfolio. After the introduction of the Mogo car loans I shifted my investment focus to these due to the offered buyback guarantee. Again interest rates on this new loan type started out higher than they are now – see chart below for development of rates – and I still profit from that as I focussed on longer term loans (typically around 60 months). Recently I felt that too much of my portfolio is concentrated in Mogo loans and I started to diversify into business loans and the new invoice finance loans by Debifo.

Beating the average ROI of 12.5% is less of a personal achievement, but more due to the fact that I started early on Mintos. In the early days there were only mortgage loans and most of these carried interest rates well over 15%. I still have over 20 active loans from that time with interest rates of 15% or more in my portfolio. After the introduction of the Mogo car loans I shifted my investment focus to these due to the offered buyback guarantee. Again interest rates on this new loan type started out higher than they are now – see chart below for development of rates – and I still profit from that as I focussed on longer term loans (typically around 60 months). Recently I felt that too much of my portfolio is concentrated in Mogo loans and I started to diversify into business loans and the new invoice finance loans by Debifo.

The secondary market

I made the vast majority of my investments on the primary market. Mostly through Auto Invest Profiles though I occassionaly made manual bids. The Mintos secondary market is very liquid – if the price is set right. I did not use it very much with one exception. I regularly list those loans in my portfolio that are more than 30 days overdue with a premium of around 1.4% to 2.0% on the secondary market. My rationale is, that these are very likely to default, in which case I would receive outstanding principal plus interest. By selling them, I get outstanding interest plus premium (minus 1% selling fee) plus interest. I am surprised that these loans are usually bought fairly quickly.

My conclusion so far

The Mintos website and the accounting function very reliable. There is a good supply of loans. Over 70% of my investment is in loans secured by buyback guarantees. So I don’t have to worry much about individual defaults risks of these loans but rather about the operator risk: will the loan provider be able to honor the guarantee? So far it works seemlessly. All covered loans that have gone 60+ days overdue have been reimbursed to me as promised. But with this construct it is very hard for the investor to gauge the risk. Should the guarantee fail, it will probably be too late to exit – I expect there will be no early warning signs. Managing and monitoring my Mintos portfolio requires little time and effort. Clearly investor demand is growing on Mintos too, but I don’t find it as hard to reinvest into new loans as on other platforms.

Loan types at Mintos (overall; not my portfolio) and development of investor interest rates over time

Thanks, Claus! I love the “My P2P Lending Portfolio..” posts because you are showing actual results with actual money. Always good to read other opinions / thoughts about some certain platform.

Thank you for this nice overview and analysis!

How would you explain the situation that after investing 11,000€ (and loans have 12+% annual interest rate) your yielded annual interest income is 1,077€, which makes 9,7% of the invested funds. Could it be because of the late loans? Or are there some loans, which do not have monthly/annual repayments?

Hi Indrek,

the explantion is much simpler: I deposited & invested the 11,000€ over time; so much of it is in the account for only several month and of course has earned interest only for these month (not a full year yet).

Excellent article Claus, I appreciate sharing the real data and real money stats. I am just starting on Mintos now but I am really excited about it, it seems like one of the best p2p lending platforms!