Estonian P2P Lending Platform Bondora* has submitted an application for a bank license in Estonia (source; paywall). Pärtel Tomberg, Bondora CEO is cited saying ‘This is a significant step and the beginning of a new phase.’. He expects teh FSA to grant the banking license in 2026.

According to earlier media reports Bondora selected Tuum as the supplier of its cloud-native core banking platform. According to a press release ‘Tuum was selected for its modular design, cloud-native architecture, and ability to meet stringent EU regulatory expectations. The decision was also supported by Tuum’s track record with other Eurozone institutions, including LHV and OP Financial Group.’

‘Choosing Tuum means we can focus on customer experience and innovation while building on a modern, scalable foundation’ said Andrus Raudsalu, Chief Strategy Officer at Bondora.

Bondora follows earlier similar moves of p2p lending marketplaces evolving into banks, e.g. Zopa in the UK.

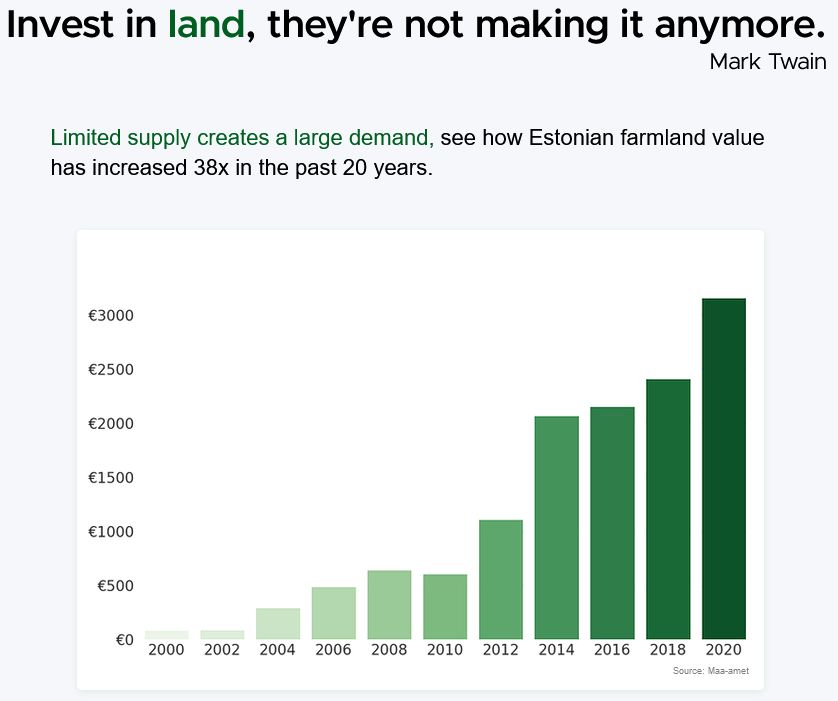

Looking to diversify into an asset class with solid security, interesting yield and less volatility? Lots of people have been investing in property for that purpose – however farm land and forest land has been outside the scope of most private investors bar the ultra-rich so far.

The newly launched startup Landex* (please use referral code 3SHWP, thx) now gives everybody access to this interesting asset class by enabling investments into European land starting from 10 EUR.

All the details of how the processworks are on the Landex* website, so here are just some excerpts.

From the whitepaper:

Land types provided on Landex Landex wants to give investors a wide choice while doing thorough due diligence. Landex is well-equipped to assess and have listing of the following land types:

Farmland– typical farmland investment where we leasethe land to farmers

Forestland– we manage the forestland and sell thecrops

Carbonland–asubcategoryofalltheabove,landsthathaveasignificantpartoftheirreturnscomingfromcarbonincome.Regenerativeagriculture,reforestationlandsandimprovedforest management, etc.

Biodiversityland–typesoflandsthatdonothaveacommercialcrop.Naturallyprotectedareas, wetlands (swamps, mangroves), natural grasslands, etc.

Developmentland–landpurchaseswiththeideatoturnthemintoresidentialorcommercial areas

The whole process is managed through the Landex app (available for iOS and Android).

After registering, I deposited 100 EUR to gain first experiences and then went through the verification process on the smartphone (which is conducted by Veriff and was completed in 2 minutes in my case).

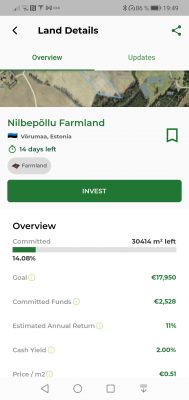

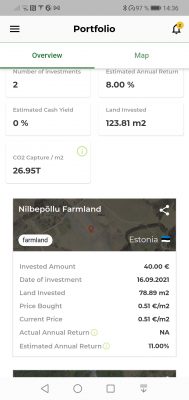

Then I was ready to invest. I browsed the details of the 2 land plots on offer and invested 40 EUR in the farmland plot and 20 EUR in the forest land plot.

As it is of course impossible to buy whole plots for the amount I invested, Landex is based on crowdfunding with multiple investors financing a purchase through an SPV and fractional ownership.

Why invest in land?

I like it for the following factors. It is a scarce ressource, that is limited and cannot be inflated. Land is an economic asset that has been bought, sold and used for centuries offering high security. It’s price is much less volatile than other assets (e.g. stocks or houses). While the yield is primarily generated in value appreciation is does generate some yearly income too as most plots are rented out.

Landex has just launched. The next development steps are introduction of an autoinvest feature and a secondary market. Landex does not charge any fees for investing, but optional usage of the secondary market will incur a small fee.

Landex uses a refer a friend feature, where investors can invite further investors. For each referred investor you get 10 EUR bonus that can be used to invest in land. If you need a referral code to sign up at Landex* please use code 3SHWP, thank you.

Crowdestate is an Estonian p2p lending market place focussing on property. It is somewhat compareable to Estateguru or Lendy, the difference is that Crowdestate has a wider mix of offers, including unsecured debts or equity. I published an interview with the Crowdestate CEO last year.

The projects usually come with a term of 1 to 2 years, occassionally a bit long or shorter. There were not that many projects in the past . Often only 1 or 2 a month. Recently the pace has been picking up. Investor demand strongly outweights supply. Often the autoinvest bids fill a new offer instantly, if not then it is often filled within a hour of coming on the plattform. There are no fees for investors. Only a few offers pay interest during term, with most accruing interest to be paid at the end of the term. There are no fees for investors.

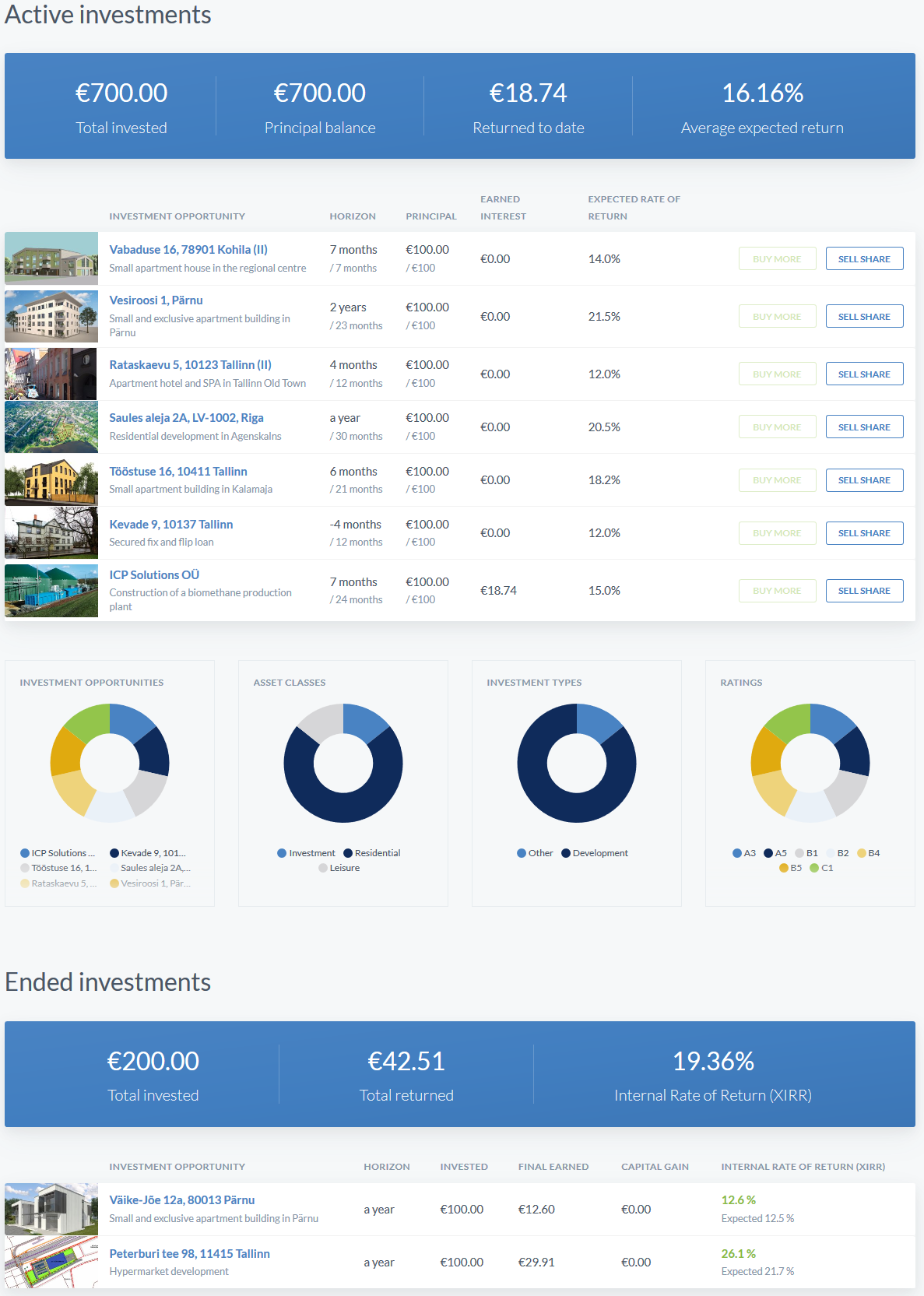

I only invested in a handful of projects to gain some experience. Today Crowdestate launched a new look for the website. This is how my small Crowdestate portfolio is displayed:

My Crowdestate portfolio – click for larger view.

Crowdestate secondary market

Today Crowdestate launched a secondary market. There is a “Sell Shares” button besides each of my active investments. To test it, I just offered one of my loans at a markup. The marketplace allows sellers to set markups or discounts.

Crowdestate is a leading Nordic real estate crowdfunding marketplace offering high-quality, pre-vetted real estate investment opportunities. Only the best investment opportunities survive our rigorous due diligence process, and these are the ones we open for investing on our platform. With each project, we present our investors with extensive background information, risk level, SWOT, business plans and financial models. Combine it with Crowdestate’s low, just 100 euro minimum investment – all of this makes investing into real estate quick, easy and affordable to everyone.

What are the three main advantages for investors?

Pre-vetted real estate investment opportunities – Our experienced real estate and finance team evaluates thoroughly each aspect of every project and picks the best investment opportunities to be published for crowdfunding. Low minimum investment amount – the minimum investment on our platform is just 100 euros, meaning basically anyone can afford to invest into real estate with Crowdestate. Everyone can invest – Crowdestate is open to all investors all around the world, provided that they have a way to make an international bank transfer to their virtual investment account previously created on our platform.

As an additional advantage, we charge no fees from our investors.

There are many different types of investment opportunities on Crowdestate. Debt, equity, secured, unsecured… Why did you decide to use so many different types for the offers?

If we look at the real estate industry, any real estate project needs different types of capital – from senior loans to mezzanine debt to preferred or common equity. Crowdestate’s aim is to become a full capital stack provider so we can address our Sponsors’ needs properly. This is the reason why we have not limited us to a single capital type.

If we look the real estate projects from investors’ perspective, investors have different investment preferences (e.g. time horizon, risk tolerance etc) and therefore they are looking for different types of investment. Young and aggressive investors might like high-risk equity deals while some other investors might prefer lower risk-lower return senior loans.

What ROI can investors expect?

The historical money-weighted average internal rate of return on our exited investment currently at 29.59%. However, as the fast-increasing money supply is driving the expected returns down, the investors’ annual returns are probably going to remain between 10-20%. The return rate is a reflection of project’s riskiness – a mortgage-backed senior loan might yield around 10% per annum while riskier mezzanine or equity investments may offer much higher yield.

How did you start Crowdestate? Is the company funded with venture capital?

During my few decades in the banking industry, I have met hundreds, maybe even thousands of clients, who are unhappy with the investments offered by their banks and they have clearly expressed their preferences to invest in real estate. Unfortunately, for most of these people investing into real estate never became a reality. They simply could not afford it due to the high entry costs and significant individual investment ticket.

At the same time, funding real estate projects had become a challenge for developers as banks became more and more picky.

I founded Crowdestate in 2014 to match the needs of the investors to the needs of real estate companies.

Is the company profitable now?

Yes, Crowdestate has been profitable from its very first year, and we have reinvested all the profits to developing the business.

Is the technical platform self-developed?

Yes, our platform was developed from scratch, and we are constantly working on improving it.

Are there any new features for the platform your team is working on? What about a secondary market?

We are currently finishing updating our mortgage-back loans offering and we will have very quick and automated approach there. We are also introducing a reverse interest auction to determine a true market rate for a specific project and an autoinvest feature.

We are also considering opening a Secondary Market for investments within this year allowing our investors to buy and sell their investments to other Crowdestate’s investors.

Currently there are usually one or two new investment opportunities per month. Can investors expect more deals in the second half of this year?

Our thorough vetting process eliminates most of the original investment ideas and therefore limits the number of investment opportunities we can present o our investors each month. Our Estonia and Latvia based teams are working hard to identify high-quality investment opportunities in the region.

We are also testing the interest for crowdfunded corporate finance deals and we are launching a new mortgage-backed loans solution soon. We expect those new solutions to increase the variety of investment opportunities on the platform.

Crowdestate is open to international investors. Can you please share from which countries the majority of your investors come?

Crowdestate is visited from all over the world and our investors come from South-East Asia to North-America.

As Crowdestate was founded in Estonia, Estonians are still the largest investor group, but the fast-growing number of international investors will bypass them probably quite soon.

Do you plan to cooperate with institutional investors? In which way?

Crowdfunding is about crowd and investment democracy and we prefer to serve a large number of small investors to serving a small number of large investors.

What is the current state of the real estate market in Estonia?

We believe the overall health of the market is good as the economy is doing well, interest rates are low and real wages are growing fast. At the same time, we have some suspicions on the health of specific sectors, namely offices and retail spaces – there is a lot of speculative developments in those sectors and we will probably see some changes there.

How do you think the property development market will be impacted by p2p lending in Estonia / in Europe in the future?

One of the leading Scandinavian banks stated recently, that the residential developments should be funded by equity, prepayments and crowdfunding. As the credit is quite tight in most of CEE countries, crowdfunding will play a significant role in funding the real estate development market.

Where do you see Crowdestate in 3 years?

I hope that Crowdestate is present outside our current domestic markets and we can help hundreds of thousands of investors in turning their savings into earnings.

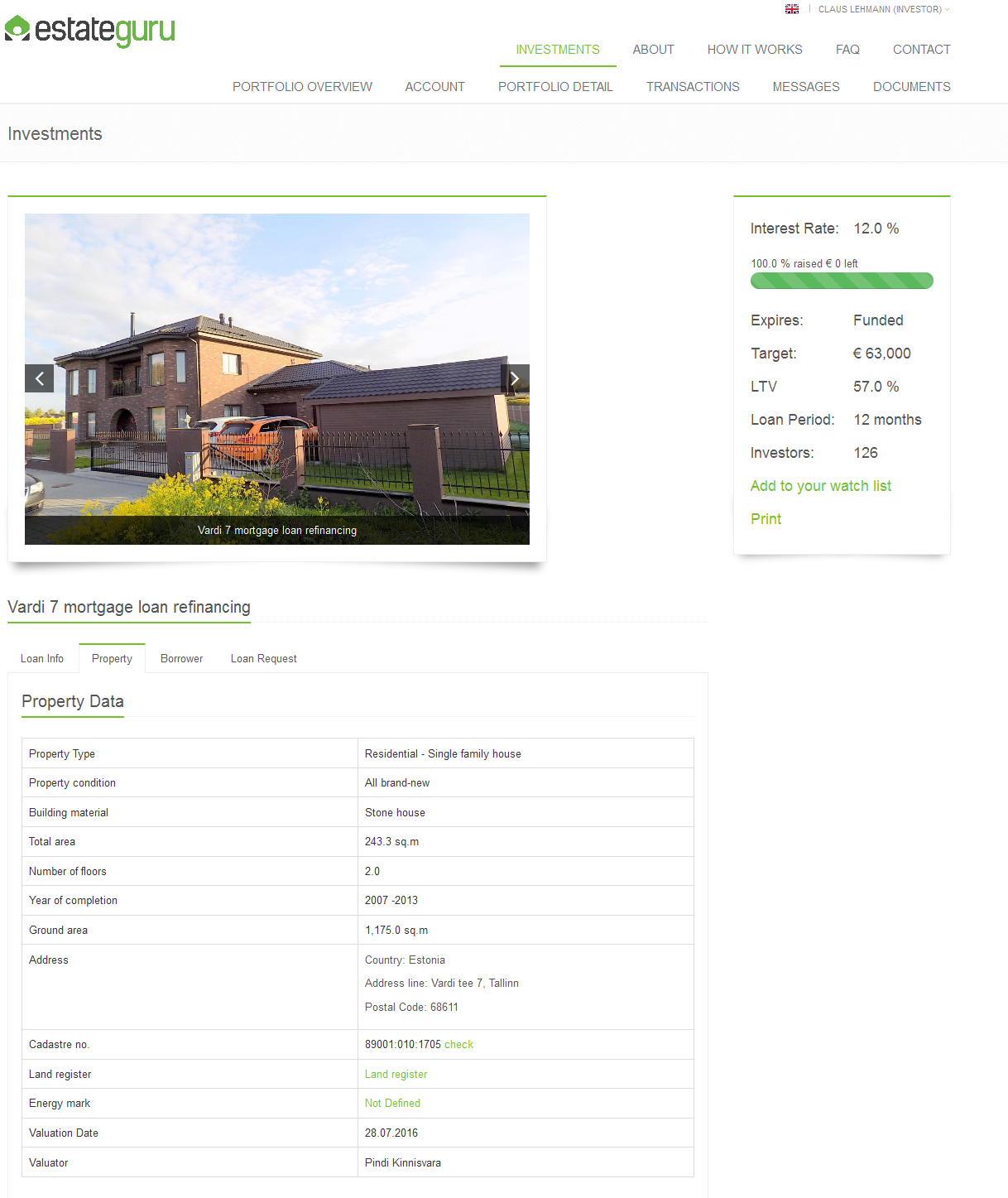

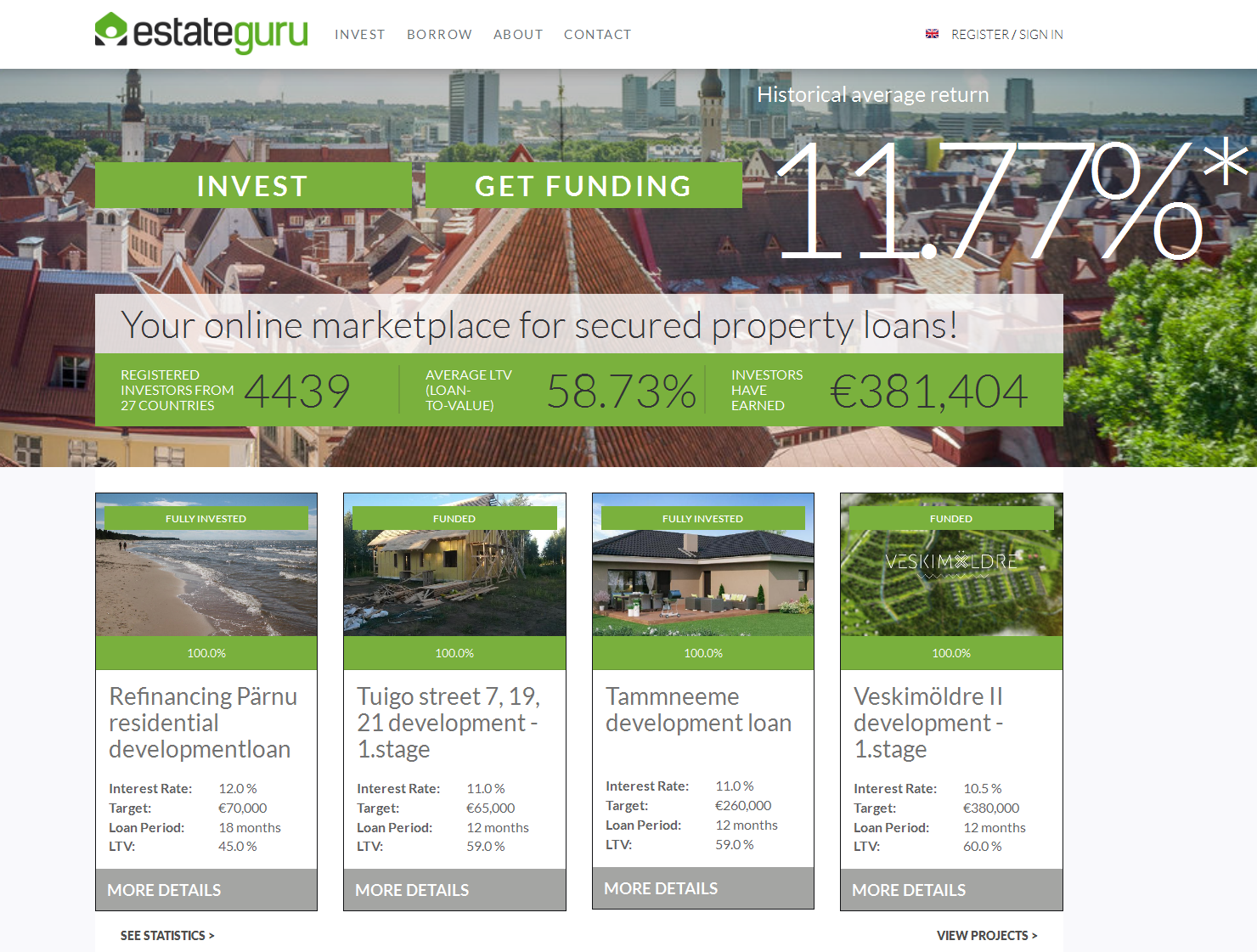

Estateguru is a p2p lending marketplace in Estonia focussed on bridge loans to property developers in Estonia. Since the launch in 2014 Estateguru has facilitated a loan volume of more than 10 million Euro in a total of 65 loans. The loans are secured by 1st or 2nd rank mortgages. Typical interest rates range from about 9% to about 12%. Some of the loans pay monthly interest, while for others the interest is paid at the end of the loan term. The minimum bid amount is 50 Euro.

Estateguru provides appraisal reports for the security. Estonia is highly advanced in digitization – this allows Estateguru to provide direct links to the official records in the land register for the plot.

Example of an Estateguru loan listing (shortened, click to enlarge image). There is more information about the loan, the security and the borrower in the other tabs

I have invested in a couple of loans over the past years and the handling is smooth. Two loans are repaid (one early) and the other loans are running on schedule. Other investors report that there have been no defaults yet, only some loans where the payment came in late for a couple of days (or a few weeks at max.). Unlike other platforms, Estateguru sends no updates about the loans.

Many investors keep some cash in the Estateguru account in order not to miss out, when new loans appear. Smaller new loans usually fill within hours. Investors can opt for a notification email, that is sent when new loans arrive. However tiny loans (< 40,000 EUR) are sometimes 100% funded by the time the email arrives. There is no autoinvestment feature / prefunding facility. Estateguru does not have a secondary market, but many loans are only for 12 or 18 months term.

Estateguru is open for investors from all over Europe (actually the EEA). If you are inside the Eurozone investments are fast via SEPA transfers. If you live outside you should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

Bonus: If you sign up using this link Estateguru will credit you 0.5% cashback on all investments you make in the first 90 days.

After what felt like a drought period, Bondora seems to focus again on working to improve functionality for investors. This week they released a new version of the cash flow report, with the following upgrades:

1) Historic payments will be split between current loans and loans in default as per the status active at the date of the payment 2) We will introduce day-level information that shows cash flow categorized per each investment 3) Forecast settings can be defined also for historic schedules so you can use cash flow based adjustments for predicting future payments 4) You can adjust your net return calculation based on the probability settings defined in the cash flow report 5) Cash flow report will show the opening cash balance and closing cash balance for each period 6) You will be able to define which data series to show on the chart 7) Historic planned schedules will be split between current loans and loans in default 8) Cash flow table results can be exported to Excel 9) You will be able to define which data series to show in the cash flow table 10) Live data from the current day (currently under Account statement for the last 24 hours) will be incorporated into the cash flow report 11) All data is in one table 12) You will be also able to filter to a specific loan in the Investments list straight through the cash flow report so you can quickly take loans off secondary market or put them there based on the information visible in the cash flow report

I have experimented a bit and like the way this report page gives me a quick visual representation of what is happing in my account and that it is very customisable. Plus it lets me set my personal values for expected loss rates and use that to calculate net return displayed in the dashboard. Read also what investor Oktaeder blogged about this feature.

If you are not investing at Bondora, this Bondora video will give you a good overview of the functionality.