Estonian P2P Lending Platform Bondora* has submitted an application for a bank license in Estonia (source; paywall). Pärtel Tomberg, Bondora CEO is cited saying ‘This is a significant step and the beginning of a new phase.’. He expects teh FSA to grant the banking license in 2026.

According to earlier media reports Bondora selected Tuum as the supplier of its cloud-native core banking platform. According to a press release ‘Tuum was selected for its modular design, cloud-native architecture, and ability to meet stringent EU regulatory expectations. The decision was also supported by Tuum’s track record with other Eurozone institutions, including LHV and OP Financial Group.’

‘Choosing Tuum means we can focus on customer experience and innovation while building on a modern, scalable foundation’ said Andrus Raudsalu, Chief Strategy Officer at Bondora.

Bondora follows earlier similar moves of p2p lending marketplaces evolving into banks, e.g. Zopa in the UK.

Metro Bank today announces that it has agreed to acquire Ratesetter* (Retail Money Market LTD) for initial consideration of 2.5 million GBP, with additional consideration of up to 0.5 GBP million payable 12 months after completion subject to the satisfaction of certain criteria and further consideration of up to 9 million GBP payable on the third anniversary of the completion of the transaction, subject to the satisfaction of certain key performance criteria.

The acquisition does not include Ratesetter’s holding in Ratesetter Australia which is being retained by Ratesetter shareholders.

Ratesetter will no longer use money for retail investors to fund new loans. All new loans will be funded by Metro Bank’s depositor base. Ratesetter will continue to manage the existing Ratesetter loan portfolio and Provision Fund on behalf of its existing peer-to-peer investors, with Metro Bank assuming no credit risk for these existing loans.

Ratesetter states “For investors, there is no change to your investment, with RateSetter continuing to manage the loan portfolio and the Provision Fund. Our Investor Services team remains available in the usual way to assist with any questions you may have and will continue to provide all administrative services. “. Retail Investor reactions on the announcement are mixed. While some welcome the development thinking that it will stabilze Ratesetter and reduce mid-/longterm risk for repayment of outstanding funds, others worry that the risks for their committed funds might increase as there will be no new loans and managed funds will thereby decrease.

Metro Bank will operate Ratesetter as an independent platform and originate loans under both the Ratesetter and Metro Bank brands.

Rhydian Lewis and Peter Behrens and CFO Harry Russell will join Metro Bank’s  team. The transaction will be funded from existing cash resources, whilst the final fair value and goodwill elements will be determined as part of the Company’s year-end accounting process. The acquisition is anticipated to reduce the Company’s CET1 ratio by circa 0.3% at 30 June 2020 on a pro forma basis.

The acquisition is conditional upon approval from the Financial Conduct Authority and shareholders holding at least 60 percent of Ratesetter’s shares acceding to the relevant transaction documents and is expected to close by the fourth quarter this year. The board of directors of Ratesetter unanimously recommends the transaction and that shareholders of Ratesetter accede to the relevant transaction documents. Shareholders holding 45.7 percent of Ratesetter’s shares have signed the relevant transaction documents at the date of this announcement. Once Ratesetter shareholders holding 60 percent of Ratesetter’s shares have signed or acceded to the relevant transaction documents, it is expected that Ratesetter shareholders who have not signed or acceded to the transaction documents will be dragged into the transaction, resulting in Metro Bank acquiring 100 percent of Ratesetter’s shares at completion.

LendingClub (NYSE:LC) announced that it has signed a definitive agreement to acquire Radius Bancorp, and its wholly owned subsidiary Radius Bank, (together “Radius”) valued at 185 million USD. LendingClub says Combining Radius and LendingClub will create a digitally native marketplace bank at scale with the power to deliver an integrated customer experience, enabling consumers to both pay less when borrowing and earn more when saving.

Radius is an online bank founded in 1987 and based in Boston, MA, with more than 1.4 billion USD in diversified assets. Its platform provides features such as check deposit, bill pay, card management, and a personal financial management dashboard, as well as open APIs to offer “banking-as-a-service” (BaaS) functionality to leading fintechs. In addition, the company offers commercial lending options for businesses, and treasury management services for pension funds, unions, municipalities, and non-profit organizations.

‘This is a transformational transaction that allows us to reimagine banking in a way that is free from legacy practices and systems and where the success of LendingClub is aligned with the success of our customers,’ said Scott Sanborn, CEO of LendingClub. ‘By combining with Radius, we will create a category-defining experience for our members that will dramatically enhance the resilience and earnings trajectory of our business.’

‘LendingClub has always been a fintech innovator, and I look forward to leveraging the strengths of both of our talented teams as we usher in a new era in banking,’ said Mike Butler, Radius’ President and CEO. ‘We are excited for our employees to operate our virtual banking platform with more resources and for our clients to gain access to an industry-leading lending product. This is a perfect marriage, with LendingClub bringing the leading digital asset generation platform, and Radius contributing a leading online deposit gathering platform, to position the combined company for long-term success.’

The combined entity expects to be substantially accretive with a cash payback of the purchase price premium and all costs in two years. The purchase price is subject to certain adjustments set forth in the definitive agreement, and the transaction is subject to regulatory approval and other customary closing conditions and is expected to close in the next twelve to fifteen months with benefits starting to materialize immediately after close.

Further, to facilitate compliance with federal banking regulations and prevent closing of the Radius acquisition being delayed or disrupted, the LendingClub Board of Directors has adopted a Temporary Bank Charter Protection Agreement, also known as a stockholder rights agreement, and approved a dividend distribution of one purchase right for each outstanding share of the Company’s stock as of March 19, 2020. The agreement is intended to deter stock positions in excess of certain thresholds set forth by the Federal Reserve under the Bank Holding Company Act. Specifically, it provides for the dilution of any person or group of persons who acquire:

(i) 25 percent or more equity interest in LendingClub or (ii) 7.5 percent or more of any class of LendingClub’s voting securities. This threshold automatically increases to 10 percent as set forth in the agreement.

Anyone already above such thresholds is grandfathered in at their current levels. The agreement is effective immediately and will automatically expire on either the closing of the Radius acquisition or after 18 months, whichever is earlier.

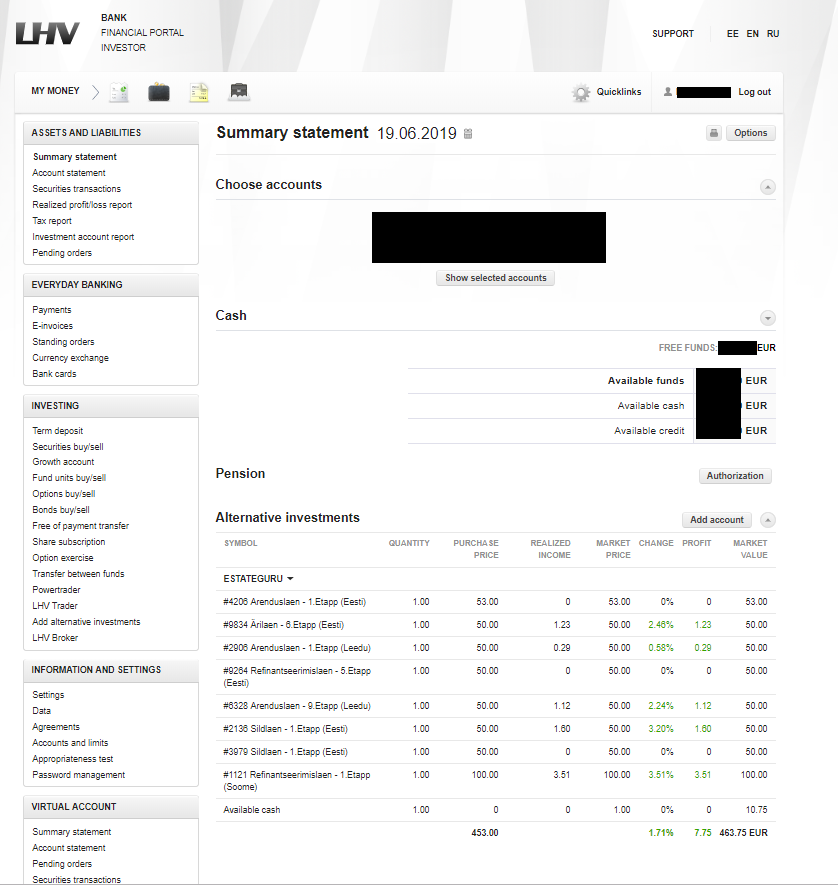

Who? What? You might wonder why that is relevant as most readers are unlikely to be LHV Bank customers. LHV Bank is a bank in Estonia.

I think it is highly interesting, as it is – to my knowledge – the first time a bank has integrated p2p lending investments in its customer interface. So the LHV bank customers, not only see their accounts and stock depots, but also their Estateguru* investments conveniently listed in their online bank dashboard. Much has been talked about what role could banks have in p2p lending (mere transaction banks? providing credit lines?) and also there is a lot of speculation if PSD2 (open banking) will help fintechs to seize the access to the customer from banks because they could control the user interface in the future. But this is actually a first step a bank takes in the opposite direction. By aggregating “non-bank” information inside the dashboard, they aim to make the banking interface more useful for the customers.

(Source: Estateguru)

Press release:

LHV customers can now see their short term property loan investments on LHV internet bank. On the summary view of internet bank, besides public stock exchange investments, one can see also alternative investments like short term property loan investments and cryptocurrencies, thus making it possible to get a quick and comprehensive overview of one’s investment portfolio. EstateGuru and Coinbase are the very first services to be switched on to the platform.

“LHV’s new service is the best example of cooperation between banks and fintech. LHV is most definitely a trendsetter in the banking sector. It is fulfilling to see that short term property lending has become a solid part of investments, and traditional banking has accepted it. EstateGuru has more than 25 000 investors throughout Europe, and the number is rapidly growing among both retail, professional, and institutional investors. We can provide our customers with more added value via interfaces like that of LHV’s “, commented EstateGuru’s COO Mihkel Stamm.

Alternative investments have become a substantial part of the Estonian investment scene, particularly among new investors. There are more than 13 000 people in Estonia who have invested in crowdfunding platforms. The fixed rate of return on debt instruments and access to the new and attractive asset classes have found their well-deserved place in investors’ portfolios. The better the quality of information, the more successful the investors.

“LHV aims to keep pace with its customers’ investment activities and that’s why we decided to take a step closer to the universe of alternative investments. The added value of this new service for our customer is a better and more comprehensive overview of the assets, thus making the portfolio management more successful “, added the Head of Investment Services at LHV, Martin Mets.

About EstateGuru

EstateGuru is the leading European platform connecting an international community of investors and businesses offering the highest diversification options for investors and flexible terms and speed of funding for businesses. The mission of EstateGuru is to provide hassle-free and flexible financing to property developers and entrepreneurs as well as diversified property backed cross-border investment opportunities to its international investor base—from the small individual investors to the institutions and everyone in-between. EstateGuru has more than 25 000 investors from 45 countries and the total money lent to date is more than 122MEUR. …

About LHV

LHV is the largest domestic financial group in Estonia. LHV’s mission is to help to create Estonian capital. According to LHV’s vision, the people and enterprises of Estonia dare to think big, start things and invest in the future. LHV’s values are to be simple, supportive and effective.

Bank ING Diba acquires p2p lending marketplace Lendico. According to Finanz-Szene.de the transaction was reported to the German Federal Cartel Authority last week. The bank has confirmed the acquisition.

Lendico went through hard times. It had to cut back on international activities, never really took off on German home turf and realigned from consumer lending to SME lending. Last year the majority stake was sold from Rocket Internet to Arrowgrass.

Speculation is that the bank acquired Lendico in a make or buy decision to save development time for an own platform, which could have taken over a year. While the price of the acquisition was not disclosed, I suspect Lendico could have come cheap, considering the lingering of the business in the past years.

Banco BNI Europa was launched in July 2014 as a digital-only bank in Portugal. Banco BNI Europa says it aims to challenge the traditional banking sector through strategic partnerships with fast-moving fintech businesses to launch new products allowing the use of the most advanced technology in terms of risk analysis, consumer experience and rapid entry into the market.

Today Banco BNI Europe announced it will start lending on Fellow Finance.

‘Modern banks expand and grow by partnerships. Fellow Finance enables and offers an easy access to invest and lend in Nordic and Central European consumer and SME loans through its platform. Through their investment account at Fellow Finance, Banco BNI Europa is able to diversify their balance sheet investment into Finnish and German loans easily and cost-effectively. This is an example that banks don’t need to set up their own expensive operations on ground but can effectively enter markets through marketplace lending platforms. It is also an example how banks can also utilize the presence of FinTech among their core business’ says Jouni Hintikka, the CEO of Fellow Finance.

‘Investing via Fellow Finance in consumer and SME loans offers us a great opportunity to easily expand our operations and we are very satisfied with the analytical and professional approach of Fellow Finance in credit intermediation’ echoes Pedro Pinto Coelho, Executive Chairman of Banco BNI Europa.

Last week BNI Europe announced it will fund German SME loans through Funding Circle. According to Pedro Pinto Coelho, Executive Chairman of Banco BNI Europa, ‘an investment in German SME – the staple of European economic stability – is a highly attractive asset class. And Funding Circle is the professional partner that convinced us with their risk assessment and credit analysis. …’.

To date Banco BNI Europa has struck fourteen fintech partnerships with European fintech leaders across the continent. The bank had 141 per cent growth by the end of 2017 taking its total assets above €500m, and cited its focus on ‘innovative products’ as an explanation for the improved performance.