Estonian p2p lending marketplace Bondora will open a new European office in Germany, saying that post brexit London is no longer attractive as a Fintech hub. Bondora formerly planned to move to London but stopped the plan after the brexit vote. ‘There is too much uncertainty, the UK lost its attractiveness as a fintech hub’ explains Bondora CEO Pärtel Tomberg the decision. Now he has Berlin, Frankfurt and Munich on the short-list. The head office will stay in Tallinn

For the Bondora business model very good access to the European market is crucial says Tomberg. He sees uncertainty how long London might be able to provide this.

After informal tals with German regulator Bafin, Bondora CFO Rein Ojavere got a positive view on the perspective for fintechs in Germany: ‘German’s regulators open up more and more to innvations in the financial sector to attract fintechs and seminal start-ups.’. Continue reading →

French Banque Postale makes its first investment into a fintech and takes a 10% stake in Wesharebonds. Wesharebonds was launched in June 2016 after one year work to obtain approval by regulator AMF. The company previously raised 3.8M EUR from 50 business angels (0.6M for its own funding and 3.2M as supply to co-invest into the offerings on the marketplace). Wesharebonds allows indiviudals and companies to invest into bonds (and equity crowdfunding) to SMEs. The valuation was not disclosed.

The parties announced that the capital will be used to expand the product offering.

Cyril Tramon, WeShareBonds CEO expressed that they wanted a partner who shared their vision and could support development.

Banque Postale is a subsidary of La Poste Groupe, which claims ana ctive customer base of 10.8 million.

Lendico announced today that it will stop originating new consumer loans in the Dutch market and focus on loans to companies.

Lendico biedt vanaf 1 november tijdelijk geen consumentenkrediet meer aan. … Vanaf 1 november kunnen alleen bedrijven nog een lening aanvragen. … Product details zakelijke lening: Kredietbedrag: € 10.000 tot € 250.000 Rente vanaf 3,79% Looptijd 6-60 maanden Een aanvrager is gekwalificeerd als het bedrijf meer dan 2 jaar bestaat en in de afgelopen 2 jaar meer dan € 50.000 omzet had. Waarom stoppen we tijdelijk? Sinds we in september 2014 op de Nederlandse markt actief zijn hebben we een veelheid aan verschillende producten ontwikkeld die op de website of voor geselecteerde partners beschikbaar zijn. We willen ons productaanbod de komende maanden herijken en een beperkt aantal producten verder automatiseren en doorontwikkelen. Om dat in alle rust te doen, hebben we besloten om het consumentenkrediet volledig te pauzeren tot minstens januari 2017.

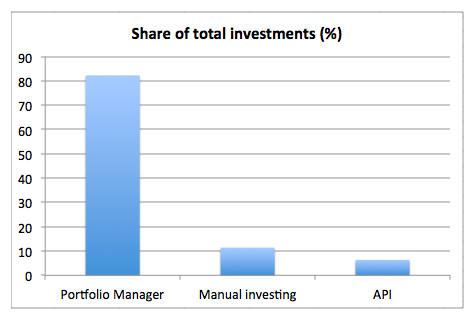

P2P lending marketplace Bondora announced that it will pull the primary marketplace from the user interface effective November 1st. This removes the chance for investors to manually invest on selected loans, leaving the options to either use the automated portfolio manager or to use the API.

Earlier this week Bondora provided this statistic showing that the majority of investments is done through the portfolio manager. This is another of the many changes the Bondora marketplace underwent in the past years.

The announcement email sent today, reads:

On November 1, 2016 we will remove the Primary Market view from the user interface.

What does this mean?

In recent months it has become clear that the Portfolio Manager offers greater efficiency through automation compared to manually investing. The increasing benefits of Portfolio Manager are the result of recent updates to the funding process, which optimize speed. Moving forward we will continue to focus efforts on further improving Portfolio Manager, Bondora API, Secondary Market and the reporting features available on the platform.

Why is Bondora removing the Primary Market from the user interface?

Bondora is removing the Primary Market from the UI because the speed of our popular automated option meets the investing and borrowing needs before manual investing can take effect. Our process improvements have created an environment where almost all loans are funded before they become visible in the UI. As a result, the Primary Market is most of the time empty.

This scarcity is due to the fact that when a loan enters the market it is open to bids for 10 minutes. After the 10 minutes expire the loan is closed. Our internal analysis and reporting shows that almost 100% of loans are funded within this brief window of time. Therefore, there is little reason to hold loans open any longer, as doing so would create unnecessary delays.

What should API users do?

Removing the primary market from the user interface does not change anything for Bondora API users. However, API users should review their settings for polling loans from primary market and reconfigure their settings to match the changes to the current funding process. We recommend that the polling of new loans be set to once a minute. Our API allows for speeds up to one query per second, however such rapid polling is also not recommended.

Finbee is a small p2p lending marketplace for consumer loans in Lithuania (see earlier coverage). I have been using it as an investor for a little over a year now. My strategy on Finbee is different than on other marketplaces. I invest loans mainly with the purpose of trading in mind, that means on Finbee I don’t plan to hold the loan parts to maturity

Finbee secondary market basics

Loans can be offered at a discount, par or premium

Seller pays 1% fee upon successful transaction

Only loans with at least one repayment can be offered. This means I cannot sell loans directly after acquiring them on the primary market (no flipping). I have to hold each loan for at least 30 days.

Late loans and loans in arrears can be offered. Loans that are 60+ days overdue cannot be listed for sale.

Maximum listing duration is 20 days; thereafter seller can relist

Buyers can buy instantly at ‘buy now’ price or make a bid, hoping that no other buyer overbids them in the remaining listing duration (or pays buy now price)

Finbee parameter UI for selling loan parts on secondary market

How I select loans on the primary market

I mostly invest in ‘D’ loans (that is the most risky rating) with long loan durations (>36 months) and high interest rates. The average interest rate in my portfolio is 32%, the maximum 35%. My reasoning for this choice is that these loans allow high markups and still offer an attractive buyer yield (XIRR value). The longer the remaining loan term is, the lower will be the impact of the markup on the calculated yield for the buyer. I mostly buy 40 Euro loan parts, sometimes multiple in the same loan. I selected this amount because larger parts might not appeal to as many buyers, as some investors only invest small amounts.

Why I select different values for the reserve price and the buy now price

Since the XIRR that is displayed to the buyer depends solely on the buynow markup, it would seem logical to set same markup prices for the reserve price and the buy now price, doesn’t it. If in the example above I would set the price to 8.4% for both than I would get 8.4% markup if the sale takes place. With 8% and 8.4% values, I most likely get only 8% (at these markups there are very rarely multiple bidders competing). So why would I forego 0.4% gain? The reason is simple. With buynow the sale takes place instantly. But if I get the buyer to make a bid, the transaction takes place at the end of the listing duration, and all interest accrued during this duration is mine. Note that the buyer can NOT back out. He is commited and the sale will take place if he made a bid. In the above case the 20 days on a 39 Euro loan part at 32% mean I earn an extra 0,68 Euro (39€*32%/365 days*20 days) interest. So in effect if someone bid 8% on this loan my gain is 8%+1.74% accrued interest = 9.74% gain (which is much better than the 8.4% buy now). Of course I have to deduct the 1% seller fee.

BTW, I wondered how Finbee manages the sales with the accrued interest. When the buyer makes the bid, as said he cannot back out. But it is not clear if he will win (another buyer could overbid him) or how much interest will accrue for I as the seller have the right to accept the bid anytime early (which would only make sense if my cash is zero and I urgently want to bid on a new loan with a much better interest rate). But Finbee can’t wait until the time of sale because at that time, there could possibly be not sufficient cash in the buyer’s account. I couldn’t figure it out, therefore I asked Finbee. The answer is Finbee reserves the maximum possible price (principal+premium+maximum possible accrued interest) at time of the bid in the buyer account. Once the sale takes place, if the actual accrued interest is lower than the reserved maximum accrued interest, part of the amount is freed up. Continue reading →

This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction : The Peer-to-peer Lending Industry in Thailand

Peer-to-peer lending which also known as social lending or crowd lending has drastically increased in the recent years in many countries over the world. The volume of peer-to-peer lending activities also has been grown rapidly, for instance, the volume of peer-to-peer lending activities in U.K. has doubled every year in the last four years.

Peer-to-peer lending might be used in many ways if it is properly regulated by the responsible authorities, this is one of the reasons which lead to the issuance of the consultation paper to regulate peer-to-peer lending industry by the Bank of Thailand.

For instance, due to the current situation, poor people and SMEs in Thailand normally face difficulties in accessing finance from banks or traditional financial institutions[i]. This affects the increasing number of informal loans outside the financial institution system which are normally illegal, specifically; the problem of informal loans currently stood at more than 5 trillion baht and covered around 8 million households in Thailand[ii]. Continue reading →