The following table lists the loan originations for July. Zopa originated 52M GBP and takes the lead for that month in Europe. Prosper reached 4 billion US$ in loan origination since inception. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in July 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

UK platform Crowdcube today announced that it has raised 6M GBP of investment to further accelerate its growth. The investment is led by Numis, a UK stockbroker and corporate advisor. Tim Draper and London-based Draper Esprit have also joined this new funding round alongside existing backers Balderton Capital, one of Europe’s largest venture firms.

The investment will enable Crowdcube to accelerate growth, continue the expansion of its team, ramp up new product development including the creation of a new solution for companies going public, and invest further in its acclaimed marketing activities.

‘We’re on a mission to help more businesses raise the finance they need to grow, create jobs and deliver returns to investors. We’ve dominated the democratisation of seed-stage equity investment since we launched in 2011 and we’re determined to do the same for larger businesses. We want to put the Public back into IPO.’ commented Darren Westlake, CEO and co-founder of Crowdcube.

This round puts the Crowdcube at 51M GBP post investment. Continue reading →

UK platform Seedrs has raised a 10 million GBP series A round led by Woodford Patient Capital Trust plc and Augmentum Capital. The capital raised will be used to launch Seedrs in the US market.

Furthermore, Seedrs is to launch a 2.5 million GBP crowd funding campaign to give existing shareholders and new investors the opportunity to participate in the round. The details will be announced later.

Seedrs plans to expand its marketing efforts in the UK and Europe, increase platform development activities and launch its business in the United States.

UK p2p lending marketplace Rebuildingsociety currently offers a promotion where one business will receive 25,000 GBP of their loan interest free. Loan applications received until 31 August 2015 will enter into the promotion.

Daniel Rajkumar, CEO of Rebuildingsociety.com, said: ‘Companies seeking loans now have peer-to-peer platforms as a mainstream alternative to the banks and I’m delighted to be giving a 25,000 GBP interest free loan to a business. Businesses seeking loan finance can approach us either through commercial finance brokers or directly and our platform will typically enable viable applications to get finance within 4 weeks.’

TARYA is the largest Israeli P2P lending platform built from the ground up, whose aim is to provide an online (24/7), financially beneficial experience for both borrowers and lenders. At the foundation of the platform is an advanced credit-scoring model relying on big data underwriting algorithms based on fraud prevention procedures

The platform founders have previously worked in both technology and regulation, and observing the state of the economic environment – local and global events and trends, we sense that conditions are ripe for fresh, more beneficial financial offerings to be accepted by the general public.

TARYA is headed by experts in fraud prevention technology and regulation, and has become a major player in the Israeli Crowdfunding transformation in order to supply consumer credit without bias. We are tackling regulatory, business and cultural challenges and – being the leading company – are excited and satisfied of the progress made so far.

What are the three main advantages for investors?

Diversification, diversification and diversification. The key to successful investments in P2P is diversifying the investor’s portfolio by offering:

Automated Investing and Reinvesting – the Investor defines risk and return preferences, while the platforms algorithm allows for a hands-free experience.

Varied borrower types – TARYA continues to develop partnerships with employers and social projects across the nation, thus providing both solid and risky borrowers, from different sectors of the Israeli economy.

Low minimum participation amount in loans – The minimum amount for investing in a loan starts at only 50 NIS (equivalent to 10 Euro).

What are the three main advantages for borrowers?

TARYA being an online financial service, provides borrowers an efficient and up-to-date approach for loan application:

Transparency – The process is performed online, without having to “wait-in-line” at the bank. Payments, interest rates and terms are presented up-front with an emphasis on “consumer protection”.

A FinTech Experience – TARYA is a unique and pioneering initiative that facilitates the direct connection between borrowers and lenders, using an online platform. This platform bypasses existing credit entities – banks and credit card companies, and allows borrowers to obtain credit at significantly lower costs. Interest rates range from 3.5%-8.0% depending on the borrower’s credit rank. Of note, non-banking (credit cards) interest rates for borrowers average 11%.

Business Partnerships – TARYA’s unique model grants upgraded loan terms for borrowers whose personal details are authenticated by their employers. This practice benefits all employees of the organization, who can receive loans at rates above their personal credit rating.

What ROI can investors expect?

Lenders investing in diversified and micro-financed portfolios average between 5%-6% returns after fees. Lenders pay a fee of 1.0% on returns.

How did you start Tarya? Is the company funded with venture capital?

We believe the venture has the potential to change the structure of the credit market in Israel: It is widely accepted that the Israeli banking sector is concentrated and not competitive, especially in regard to the household and small businesses sectors. Since setting up shop in May 2014, TARYA has been growing in borrowers, lenders and partner organizations.

TARYA is funded by private equity. Since establishment, we’ve received several applications from VC and institutional investors.

Is the technical platform self-developed?

The platform is developed internally, built from the ground up with underwriting and credit rating processes that combine banking know-how, statistical modeling and technology professionals with extensive expertise in online fraud and information collection from social networks and other sources.

The diverse expertise of our team and the advanced technology is giving us a competitive advantage and will enable us to confront upcoming challenges head on. Continue reading →

This is part 4 of a series of guest posts by British Bondora p2p lending investor ‘ParisinGOC’. In part 1, part 2 and part 3 published in December 2014 you could read how he used the data to built decision trees to identify lending opportunities. Now you can read how that strategy worked out.

Introduction

In August 2014, I realised my portfolio of P2P loans at Bondora was not performing as I would wish. There was an urgent need to change the way I selected loans in which to invest the money I had at my disposal. My search for a better way of selecting loans lead me to use Decision Trees to analyse the loan data available from Bondora using “RapidMiner†– software available to download for free.

It is now over 6 months since I described my original work to construct the Trees. This follow-up article chronicles what I believe is the success of my efforts to date whilst also describing the multiple factors, both within and beyond my control, that mean that, whilst I feel very comfortable with the progress made to date, others may feel that I have just been lucky!

The journey since I created my first Decision Tree and started to make purchasing decisions based almost totally on their outputs has been one of constant change. Detailing the changes to elements over which I have no control has shown me how they contribute to what I believe is success as much as my own efforts to improve the selection processes. Describing the change in the Decision Trees as well as their use in the dynamic Bondora environment has left me feeling that, without constant monitoring and review of both the process of creating the Trees as well as their use, it may still be very easy to snatch defeat from the jaws of victory.

Key to ensuring the veracity of my protestations of success has been the maintenance of a consistent approach to my selection and lending process. To this end, I will describe those changes to my process that I can control and explain how and why such changes have taken place. In short, I have maintained a restricted buying policy, investing only the minimum amount (5 Euros) at any one time and, latterly, only buying a maximum of 2 loan parts (of 5 Euros each) in any one loan, depending on the outputs from the Decision Trees and my own mood at the moment of purchase. I realise that this last phrase is not at all scientific, but the fact that my Portfolio of c.12000 Euros was not performing as expected was for me, a non-trivial affair and some emotional response has to be accommodated.

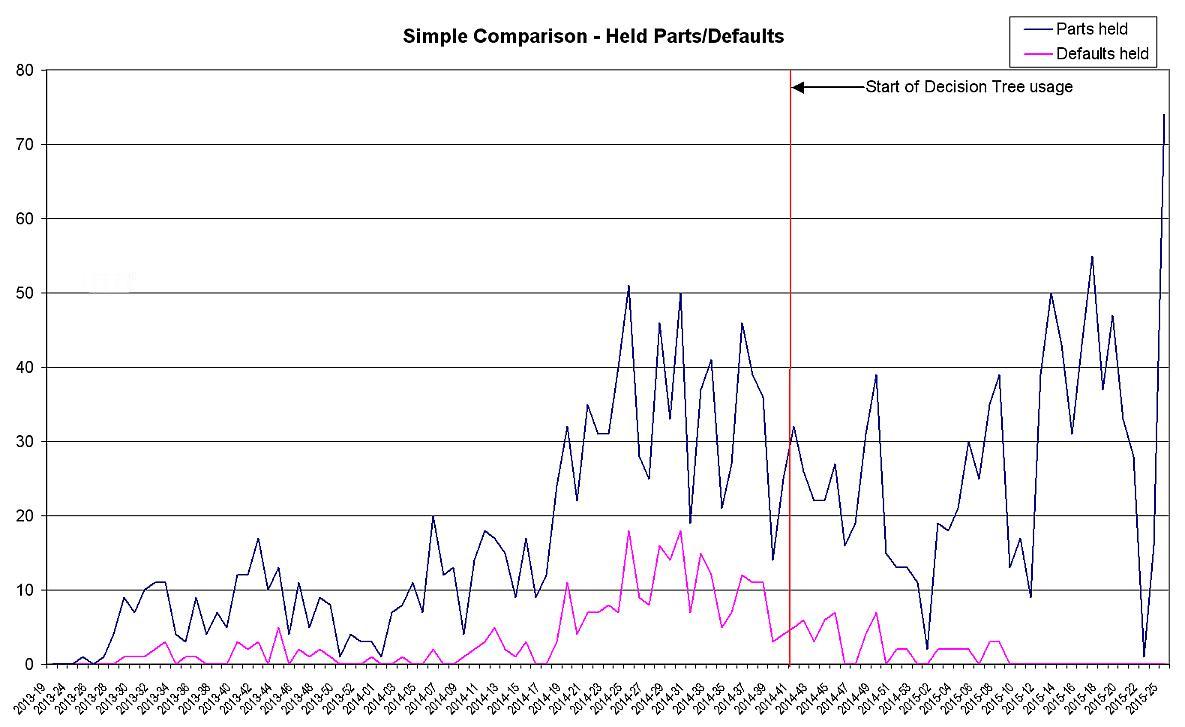

I have already stated that I believe my efforts have been successful. This is based on the fact that the rate of default (Once a loan principal has been overdue for 60+ days, it is labelled as “defaulted†– Bondora FAQ) in my portfolio has returned to historical, pre-2014 levels. Up to this time, even though I had come to realise that I needed to actively manage my portfolio, my selection of loans was done almost entirely using the “Portfolio Manager†– an automated, parameter-driven purchasing function provided by Bondora and supplemented by instinctual analysis of the descriptions of the Loan Applications available to invest in.

Looking at the simple chart of Held Parts/Defaults, the number of defaults in held loans rose significantly over the summer of 2014, coinciding with a big increase in both the number and value of investments on my part. Referring to the same chart, it can be seen that, even though the number of investments remains close to summer 2014 levels, my defaults have fallen to the numbers experienced earlier, at much lower volumes.

With my new-found confidence that I have a process for selection and management that appears to be sound, I have started to increase the volume of Loan Parts purchased so that the value is now approaching Summer 2014 levels of investment.

Progress to date

Graphical representation of Progress

I will use a more detailed graph showing the volume of Loan Parts purchased, those subsequently sold, those “Overdue†and those in default (still held by me as well as sold) to hopefully illustrate the performance of my selection and management processes. Continue reading →