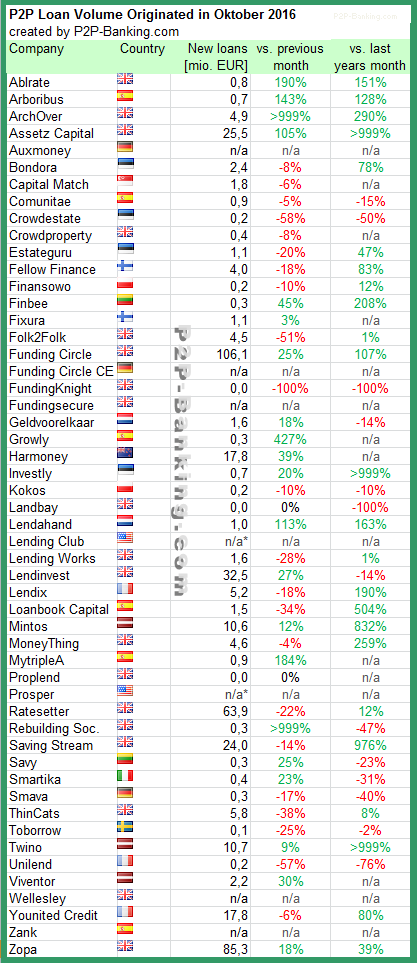

The following chart lists the loan originations of p2p lending marketplaces in October. Funding Circle had a record month ahead of Zopa and Ratesetter. Lendinvest has strong results too and Assetz Capital makes a big leap forward. The total volume for the reported marketplaces adds up to 443 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. Thincats crossed the 200M GBP funded this inception milestone.

Table: P2P Lending Volumes in October 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

BorsadelCredito.it is the first Italian p2p lending platform. We help creditworthy SMEs to obtain credit in just three working days while promising 5-7% return to our investors. So far, we disbursed loans for 4.3M EUR (as reported on our statistics page) boosting the savings of hundreds of lenders.

In a market context where about five million SME’s are facing strong difficulties in approaching traditional credit channels, P2P lending represents a breath of fresh air for both investors and entrepreneurs.

What are the three main advantages for investors?

For investors, accessing a digital marketplace represents an unprecedented way to obtain strong returns while supporting Italian SME’s. Overall, expected average returns range from 5 to 7% and, thanks to a strong diversification level (funds are divided among hundreds of firms) the risk of losses arising from defaults is strongly contained.

With BorsadelCredito.it our lenders invest in the Real Economy. The digital marketplace is the most efficient and attractive way for credit operations in the Italian enterprise framework: loan fund and SMEs financing opportunities represent one of the easiest investment options in the whole market.

What are the three main advantages for borrowers?

For the applying companies, forwarding a request is very easy: as for the lender, the experience is completely digital and way faster than the traditional credit channels. From BorsadelCredito.it it takes only 5 minutes to complete a loan request: in order to be evaluated, firms must have at least one year of activity, 50.000 EUR stream of gross revenue and no sign of adverse events from Credit Bureaus.

Funding requests are handled by our neuronal algorithms in a few hours and then forwarded to an experienced team of credit analysts, who overlook the firm’s statements and overall performance in 24 hours to send a final response: if the evaluation is positive, credit can be disbursed in just two working days, without the need to open a bank account or provide any guarantees.

What ROI can investors expect?

The ROI our investors can expect is very high and it’s around 5/7%.

Currently the average is 5.71% after bad debts and fees, much higher than what they would earn with the other traditional tools for investments. Last but not least we have a credit protection for our investors payed directly by borrowers.

Is the technical platform self-developed?

Yes, the platform is completely self-developed, as for our valuation models. We invest most of our resources (both in terms of time and money) in the development of efficient processes, workflows and credit scoring models (for example, we are now building a more complex Web-scoring model, which uses big data from the internet to give us a clear overview on how the web sees the evaluated company). Continue reading →

Zopa is the first p2p lending marketplace to run a hackathon called Zopathon. Participants a challenged to code something ‘that makes interest rates more interesting’. I have seen several hackathons in the fintech space but usually they are organized by banks, service providers or accelerators and none were p2p lending specific. Zopa says they will introduce APIs, that can be used in the 24 hour event. Sign up for participants is here.

Today Lending Club has unveiled a new product offer. Borrowers in California will be able to refinance auto loans through Lending Club. Lending Club says that the opportunity is huge with currently more than 1 trillion US$ in auto debt outstanding, while just a fraction of that – 40 billion US$ – refinanced annually. The company states this represents huge potential for both Lending Club’s platform and the millions of Americans who could save by refinancing into a more affordable product. Lending Club estimates the average APR for borrowers on new loans through Lending Club will be about 1-3% lower than their current loan, translating into an average savings of up to 1,350 US$ over the life of the loan.

“Tens of millions of Americans borrow over half a trillion dollars every year to buy cars. The practices and processes of the auto lending industry offer consumers limited options and a lack of transparency. This has created a gap between the rates consumers pay and the rates they might otherwise qualify for, unnecessarily driving up debt burdens,” said Scott Sanborn, Lending Club’s President and Chief Executive Officer. “We are excited to leverage our technology and core capabilities to put thousands of dollars back in consumers’ pockets.”. “This is Lending Club’s first offering of access to a secured loan with an overall risk and return profile that’s complementary to the unsecured loans available through our platform. It’s a big step in the evolution of our platform, a win for consumers, and will give our investors access to another proven asset,” Sanborn said.

Loans will be for amounts from 5K to 50K US$ with terms of 24 to 72 months and APRs ranging from 2.49% to 19.99%.

Lending Club strives to offer a much simpler application process than competitors. While the loans are initially limited to borrowers in California it seems likely that Lending Club will expand that. An article with more details is on Lendacademy.

Estonian p2p lending marketplace Bondora will open a new European office in Germany, saying that post brexit London is no longer attractive as a Fintech hub. Bondora formerly planned to move to London but stopped the plan after the brexit vote. ‘There is too much uncertainty, the UK lost its attractiveness as a fintech hub’ explains Bondora CEO Pärtel Tomberg the decision. Now he has Berlin, Frankfurt and Munich on the short-list. The head office will stay in Tallinn

For the Bondora business model very good access to the European market is crucial says Tomberg. He sees uncertainty how long London might be able to provide this.

After informal tals with German regulator Bafin, Bondora CFO Rein Ojavere got a positive view on the perspective for fintechs in Germany: ‘German’s regulators open up more and more to innvations in the financial sector to attract fintechs and seminal start-ups.’. Continue reading →

French Banque Postale makes its first investment into a fintech and takes a 10% stake in Wesharebonds. Wesharebonds was launched in June 2016 after one year work to obtain approval by regulator AMF. The company previously raised 3.8M EUR from 50 business angels (0.6M for its own funding and 3.2M as supply to co-invest into the offerings on the marketplace). Wesharebonds allows indiviudals and companies to invest into bonds (and equity crowdfunding) to SMEs. The valuation was not disclosed.

The parties announced that the capital will be used to expand the product offering.

Cyril Tramon, WeShareBonds CEO expressed that they wanted a partner who shared their vision and could support development.

Banque Postale is a subsidary of La Poste Groupe, which claims ana ctive customer base of 10.8 million.