We last reported on Lendico refocusing on SME loans instead of consumer loans in Germany. Sinces then there is more negative news. Sources say that Lendico was in talks with Spanish bank BBVA, but failed to close a financing deal. In December several employees left the company. Lendico said that these were normal fluctation and that the Lendico group has more than 100 employees.

Documents accessed by P2P-Banking.com show that the largest (by loan volume) German p2p lending marketplace Auxmoney made an operating loss of 13.1 million EUR in the year 2015 (compared to 8.48M loss in 2014). This was before receiving Series D funding in early 2016.

Funding Circle CE, Berlin, the German division of Funding Circle closed 2015 with an operating loss of 9.45 million EUR (compared to 2.83M loss in 2014).

Germany seems to be a very hard market for p2p lending companies to crack. Interest rate levels for consumer loans are very low compared to other markets. banks are competitive. And there is no significant amount of credit card debt that can be refinanced. P2P Lending marketplaces cannot offer better interest rates, they need to find other competitive advantages. And customer acquistion costs to win borrowers through online marketing channels are high in Germany.

While Lendico never published monthly origination volumes, Auxmoney and Funding Circle CE stopped making monthly figures available early in 2016. The latest publicly accessable figures were 10.6 million EUR new loan originations for Auxmoney in January 2016 (ranking in Top 6 of Europe’s marketplaces) and 0.8 million EUR for Funding Circle CE in June 2016.

Funding Circle has said that it will use part of the funds of the recent 100M US$ round to consolidate its position. It will be interesting to see if this results in higher activity in Germany as they announced to concentrate their continental focus on the Netherlands and Germany while stopping to issue new loans in Spain.

Klear is a Peer to Peer Consumer lending platform. We target Prime Bulgarian Borrowers. We pre-fund the loans, then we list them on the market where investors from EU and EEA can buy parts of them.

Klear has been built by a team of professionals from the consumer credit industry. Almost all of us came from BNP Paribas Personal Finance Bulgaria, the market leader (known as Cetelem in some other countries). For example, Nikolay was the IT development team leader, Lukasz was the CFO then the Chief Risk officer and I myself was the CEO.

Klear is all about building something solid.

What are the three main advantages for investors?

A good net return. 5.5% expected in average, well above the remuneration of deposits, which is close to zero. Klear does not charge fees.

A low risk. We are one of the few platforms in Europe serving good profile borrowers. No subprime or payday loans customers. Such portfolio of credits should be much more resilient in case of economic downturn.

An easy exit option. If an investor sells his loans without premium or discount, all the loans without bad payment history will go on the primary market.

What are the three main advantages for borrowers?

The best interest rates on the market. Cheaper than the banks’. It’s key to attract excellent borrowers.

Full online process. Unique in Bulgaria for prime loans. Authentication is performed through a convenient and efficient video-call. Partial or full early repayments can be done online.

No hidden fees. We have a one-off fee when the loan is disbursed. That’s all.

What ROI can investors expect?

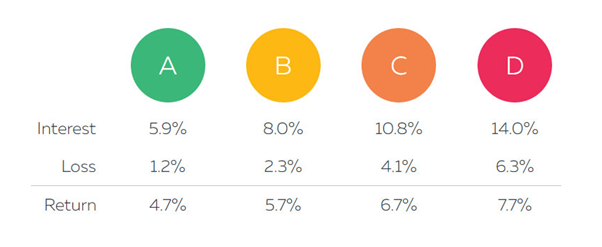

5.5% in average. Thanks to our credit scoring algorithm, we attribute a risk segment to each borrower (from A to D) and determine his interest rate based on it.

Our portfolio is mainly constituted of A and B. But investors can select the segments they want to invest in, according to their risk / return appetite.

Is the technical platform self-developed?

Yes. Everything was developed in-house. The team includes 5 software developers and a designer. Our third co-founder is an IT architect with huge experience in handling core banking systems. We invested a lot of energy building the platform: in the front end to offer a great user experience, and in the back end to ensure a solid setup.

How reliable is the credit rating / credit history data available in Bulgaria?

It’s probably one of the countries with the richest set of available data. The credit bureau registers all the credits financed in Bulgaria, by banks and non-banks, with 5 years of history.

Besides we consult the National Health Insurance database, where we can check the salary and the employment history of any credit applicant. We also consult the Police database to check if the ID card is not stolen.

The founders financed the company by committing 1 million Euro from personal savings and collecting from family and friends. That is amazing – how do you feel about this achievement?

That’s great! It shows trust in the team, in our experience, in the project and common goal. We built something to last. We all have been very successful in our careers in the banking industry and now we want to do things differently, for the better and we believe we can. That’s the main drive for all of us.

What was the greatest challenge so far in the course of launching Klearlending?

To explain that we are NOT a new subprime or payday loan company, like the many other non-bank institutions in Bulgaria. To demonstrate that we are providing something better than banks, for both sides, borrowers and investors.

Can you please describe the market environment and regulation in Bulgaria?

The total consumer credit market is around 5 billion Euros. These loans are issued in the domestic currency, Bulgarian Leva (BGN), but it’s important to know that Bulgaria is in a currency board with the Euro since 1999 (at that time it was with the Deutsche Mark) and the parity has not changed since. So, there is almost no currency exchange risk, when investing in Klear loans in Levas.

Although there is no specific regulation for peer to peer lending, we decided to apply for a non-banking financial institution registration in the National Bank. We have this accreditation and it gives us the possibility to consult the National Credit Bureau.

Which marketing channels do you use to attract investors and borrowers?

Since one year, we have been providing online financial education tools (an online budget management application) and a blog where we regularly publish articles regarding personal finance. That’s an efficient inbound acquisition channel.

We are also very active on social media and we perform online advertising.

Is Klear open to international investors?

Yes, to citizens from the European Union and European Economic Area, who have a bank account opened in a bank from these regions.

Where do you see Klear in 3 years?

Having a visible market share in the consumer credit market in Bulgaria and operations in a few other countries. As we have worked in many before and are familiar with the specificity of their domestic markets.

Being recognized as a fair, transparent and social impact player, also helping people who cannot get a credit by providing them financial advice and support to solve their debt issues.

Linked Finance, an Irish p2p lending marketplace for SME loans active since spring 2013 , announced it has secured backing from French investment group, Eiffel Investment Group, who will contribute up to 20% of funding for new loans listed on the platform. Eiffel’s dedicated online lending team has been involved in the space since 2011. It currently manages close to 200 million EUR on behalf of several multi-billion institutional investors across a range of leading P2P platforms, including Lendix in France and Funding Circle in the UK.

The agreement will further boost liquidity on Linked Finance’s platform, which has already provided loans to more than 700 SME since its launch. With plans to further accelerate lending in 2017, Linked Finance’s ultimate goal is to become the country’s biggest source of non-bank SME finance.

Commenting on the news, Niall Dorrian Chief Executive Officer of Linked Finance, said:

“This agreement with Eiffel is a vote of confidence in Linked Finance’s business model and recognises our strong growth trajectory. Eiffel monitors over 100 lending platforms worldwide. They know the industry well and what it takes to succeed. A diverse funding mix is important for our long-term development. Eiffel’s support will complement our existing lenders, ordinary members of the Irish public, who will still continue to play a crucial role in helping us to fulfil our mission of providing fast and affordable finance for Ireland’s SME sector.â€

Etienne Boillot, CEO and co-founder of Eiffel eCapital, said:

“We are experienced investors in online lending platforms and believe they are transforming borrowing opportunities for small businesses around the world, and reducing reliance on traditional bank financing. In Linked Finance, we have identified a leading player in the Irish market and a business that we are confident will deliver on its ambitious expansion plans. As institutional investors, we not only bring more liquidity to the market, but also more confidence in this method of fundraising, which should help attract more SMEs to borrow and more retail investors to lend, a win-win for all involved.â€

Eiffel’s online lending activity is backed by several large insurance companies including Aviva France, AG2R La Mondiale. One of their key objectives is to finance loans for small and medium sized enterprises (SMEs) via lending platforms in France and Europe; they are one of the leading players in Europe in this market.

Linked Finance recently completed Ireland’s biggest ever P2P loan, raising 250,000 EUR in two tranches for serviced office and flexible workspace provider, Iconic Offices. The loan was funded by Eiffel eCapital alongside more than 400 individual lenders; just some of the over 14,000 investors on the marketplace.

In 2016, Linked Finance saw a 132% increase in lending activity over the second half of the year. In total Linked Finance has funded over 700 loans since launch. Key sectors using the SME loans include retail, food, agriculture, manufacturing, professional services, education, construction and distribution

The P2P lending platform is already in talks with other leading institutional investors, in Ireland and internationally, and they are actively looking for further funding partners who want to deploy capital via the site.

Peter O’Mahony, Linked finance founder and CEO Niall Dorrian

In January 2017, Factor@Work (an Italy based portfolio manager) has completed the purchase of 5 million EUR of corporate receivables through a securitization vehicle. All the assets have been originated by Workinvoice, an Italian invoice trading platform.

A first for Italy’s securitisation market, the deal was arranged by Workinvoice, while Zenith Service acted as SPV provider and master servicer. The receivables being securitised were sold by Italian small and medium sized enterprises (‘SMEs’) through Workinvoice’s invoice trading platform, and were originated by Workinvoice.

As part of this new securitisation model, Italian SMEs utilize the platform offered by Workinvoice to offer for sale some of their trade receivables held against their clients; the investor may then enter into a credit insurance agreement with an insurance company.

Workinvoice states that based on the receivables that have a low default risk and a high turnover, invoices securitization is a multistep process of providing a financing source by transforming illiquid assets into securities, resulting in the liquidation of the assets and the creation of new financing sources. Continue reading →

Funding Circle raised 100 million US$ of equity capital in a round led by Accel Partners. The round also included other existing investors Baillie Gifford, DST Global, Index Ventures, Ribbit Capital, Rocket Internet, Sands Capital Ventures, Temasek and Union Square Ventures.

The company will use the funding to continue to consolidate its position, as well as to continue to invest in technology and talent.

Measured by new origination volume during the last months Funding Circle is the largest p2p lending marketplace in the UK. The company is also present in the US and in continental Europe. Last week the British Business Bank committed to lend 40 million GBP to British SMEs through Funding Circle.

Funding Circle has now raised 373 million US$ in equity capital. The previous round was a 150M US$ in 2015 round led by DST Capital.

For decades buying houses, refurbishing them and selling them at a higher price and moving on to the next property seemed like a popular sport to Brits. Many of them see properties as investments and with house prices mostly moving up lots of them aimed to finance a property while they were young and then build a portfolio. With limited supply of new land with planning permissions this strategy worked well most of the times in the past, except when the market overheated and a real estate bubble popped.

There are downsides to this do-it-yourself approach:

Concentration of risk in one or few properties: if they underperperformed for what ever reason, the yield was sub-average

A lot of money, time and work required. The investor had to do everything itself as a landlord

Selection of new properties usually limited to a small region the investor lives in

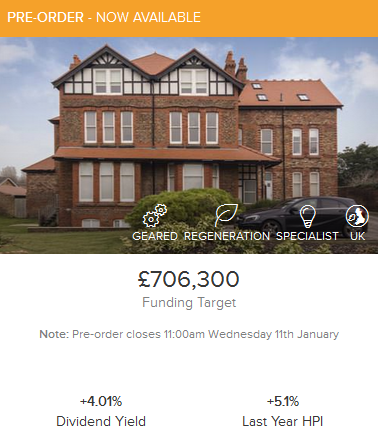

British platform Property Partner allows everyone to invest in British properties from a minimum of 50 GBP. Investors select a listing, invest into a SPV (special purpose vehicle company) that pools the investment in the property. The SPV collects rental income and pays dividends to investors monthly. A useful table of the past achieved rental income can be seen here. In the green marked cases the actual rents are higher than the original forecsts. Potentially investors can also gain, if the value of the property rises.

The time span of an investment is 5 years, however investors can try to sell their parts on the secondary market, which allows discounts and premiums any time.

The platform allows the investor to diversify across multiple properties easily. The fee is 2% for investment (in new listings or buying through the secondary market). For management, advertising and letting Property Partner charges 12.6% of gross rent.

So far Property Partner has funded 311 properties for 43.9 million GBP with 9.100 investors participating.

For new listing there is a pre-order period, where bids are collected. If the listing is oversubscribed then each investor is allocated a lower proportionate amount of shares.

Each listing contains an investment case desctiption, property details, a floor plan, financials, a solicitor’s report and a surveyor’s report as well as the house price index (HPI) information for the area.

For the secondary market there is a ‘data view’ section which lists key indicators for the parts listed for sale.

Investors that do not want to pick listings can set up the auto-invest option which will automatically invest an amount the investor sets each month in 5 properties.

Investing from abroad

Property Partner allows foreigners (except for US residents) and corporations to invest. If you do not live in the UK but see the UK housing market as an investment opportunity Property Partner is a hassle free possibility to invest in british real estate. Non resident investors should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

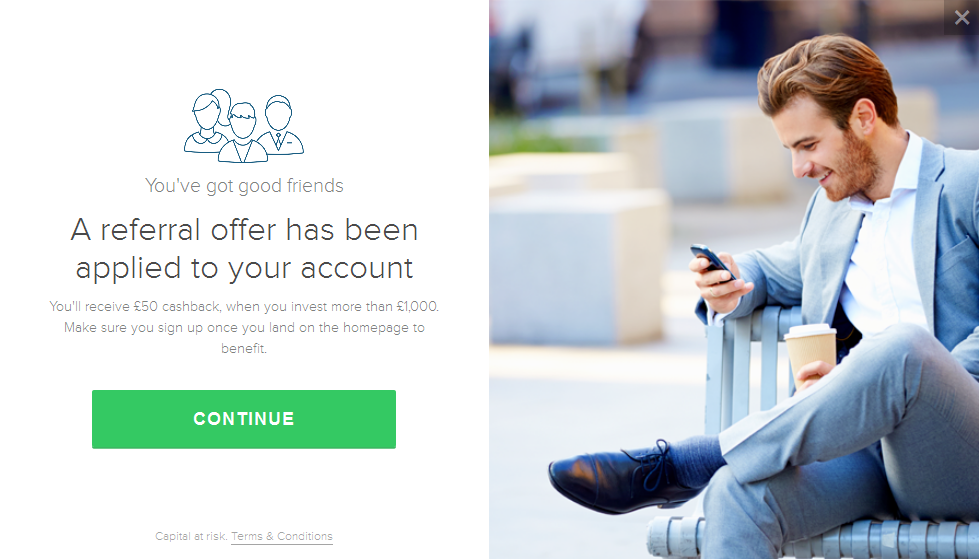

How to get 50 GBP cashback at sign-up

To get 50 GBP referral cashback, when you invest more than 1000 GBP sign up now via this link . To see available promotions by other platforms visit our cashback offer page.

Property Partner cashback confirmation at sign-up. To see it follow this link and sign up.