Baltic property lending platform Estateguru* has just launched a round on Seedrs* to raise up to 2 million EUR in new funding at a pre-money valuation of 28.8M EUR . Estateguru was launched in Estonia 6 years ago and has since expanded into the Latvian, Lithuanian, Finnish, Portugeese and German markets. Using the platform 47,000 investors have funded over 1,400 loans with a volume of 202 million EUR for an average return of 11.8% (as per Estateguru statistics page). All loans are secured by mortgages. Estateguru says that so far all recoveries of defaults have returned 100% of the capital and just the length of discovery varied sometimes taking months, sometimes taking years.

Estateguru plans to use the raised capital to further develop the product, especially improving features for institutional investors. Estateguru* can build on the experiences it made in a two-year relationship with German Varengold bank which has provided a credit line to finance loans. A second goal is to expand into further markets. In a recent investor webinar CEO Marek Pärtel named UK as a potential market, stating Estateguru already holds the required licenses since last year. Furthermore Estateguru will implement integration with payment provider Lemonway.

Pärtel said in the webinar that Estateguru has doubled in size every year in the past and expects the fast growth to continue in the future.

less defaults: 0 AUD (as all loans are covered by the provision fund)

Unlike on other platforms, I did not stop my autoinvest at Ratesetter AUS when the crisis evolved. My main reasons were that the provision fund is quite reasonably filled (>10M AUD) and I did not want to change the funds back to EUR currently, so rather than withdrawing them and storing them in AUD cash without any interest I figured I could just continue to reinvest them.

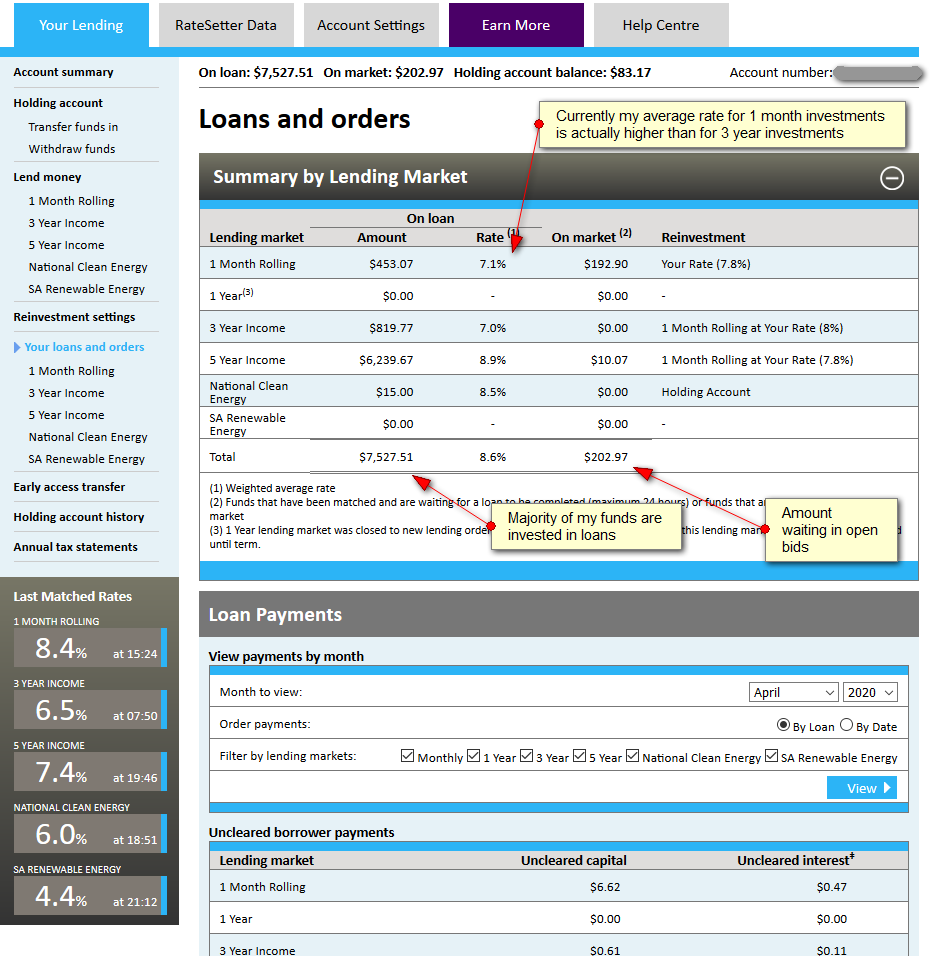

I now reinvest only at the 1 month market as the interest rate there is frequently peaking at higher rates than on the 3 or 5 years market. The following screenshot shows the current allocation of my funds at Ratesetter.

click on image to enlarge screenshot

What measures did Ratetter take in reaction to the pandemic effects on the market

In early March market turmoil caused temporary spikes of interest rate matches up to 19.9%. This was mainly caused by less lender money than usual offered. Starting on March 23rd, Ratesetter imposed a maximum ceiling of 9.0% for the lending rates on all markets. Older bids that were higher were cancelled.

In the following days investors mostly reallocated remaining funds on offer away from the longer term markets to the 1 month market.

On (or about) March 25th, the remaining funds on the 1 month rolling market must have fallen below the funds replacement buffer of 300K AUD, invoking section 7.7. of the product disclosure section, meaning paybacks on 1 month loans are not return to investors but rather reinvested at the previous rate. While it happend a few time to me since then, it is not really a problem (even so it is relent at pre-crisis interest rates of 3.5%), as I had very little funds on the 1 month market.

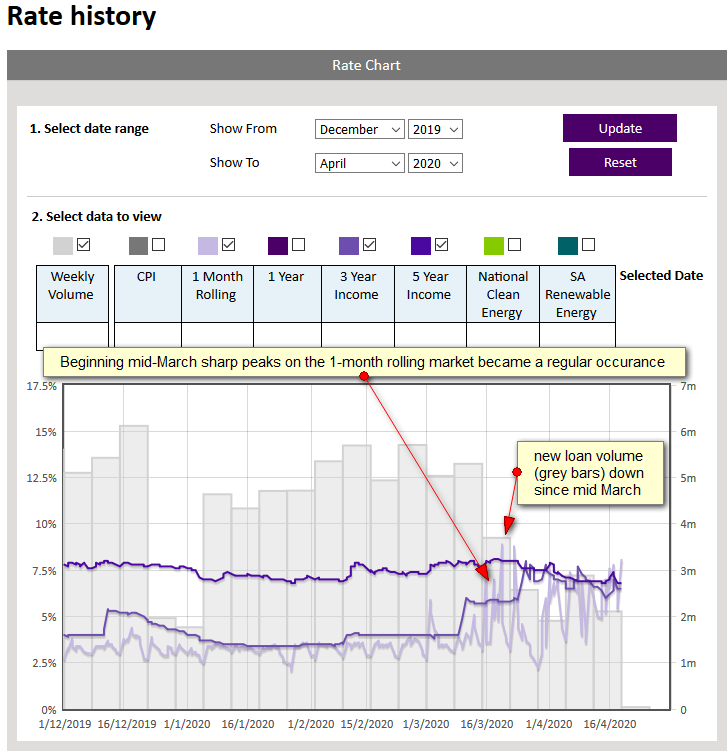

The following chart shows the turbulence starting mid-March, with rates bouncing up and down since then.

Overall the main impact on Ratesetter so far is the drop in new loan volume and the much higher interest rates on the monthly market. As far as I can tell repayments on the loans arrive regulary and if there is an impact on default rates it still lies in the future.

click on image to enlarge screenshot

Another big fallout of the crisis has been the forex impact. My home currency is EUR. Compared to that currency, the Australian dollar abruptly devalued in March. I even considered excahnging additional Euro to gain of the exchnage rate drap, but decided against it. The rate has moved back in the direction of pre-crisis levels since. As I have not withdrawn any money from Ratesetter the exchange rate fluctuations have not impacted me.

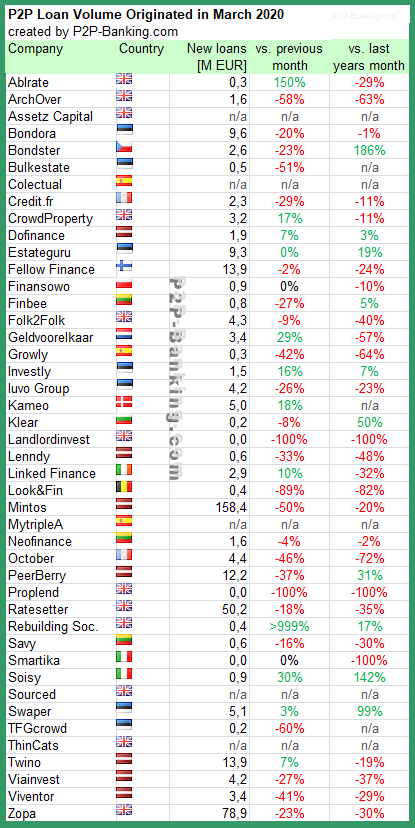

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 397 million Euro, down 40% to the previous month. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Lenndy*.

Milestones achieved:

Mintos* crossed 5 billion EUR originated loan volume since inception

The effect of the current crisis is impacting nearly all marketplaces significantly in the second half of March. Read my previous article ‘Hunger for Liquidity – State of P2P Lending in Times of the Coronavirus‘ for further observations on this. To counter the effect the sinking volumes has on revenues of the marketplace company, Mintos* and Assetz Capital* announced the introduction of new fees for investors.