I started lending at Ratesetter Australia* in 2018. Read my article I wrote back then about my reasoning for selecting the platform and how I got started: ‘Up to 9% Interest Rate – How To Register as a Non-Resident Investor at Ratesetter Australia‘.

Some key figures on my lending since 2018:

- amount deposited: 6,862 AUD

- interest earned: 1,003 AUD

- less interest margin fee: 88 AUD

- less withholding tax: 88 AUD

- less defaults: 0 AUD (as all loans are covered by the provision fund)

Unlike on other platforms, I did not stop my autoinvest at Ratesetter AUS when the crisis evolved. My main reasons were that the provision fund is quite reasonably filled (>10M AUD) and I did not want to change the funds back to EUR currently, so rather than withdrawing them and storing them in AUD cash without any interest I figured I could just continue to reinvest them.

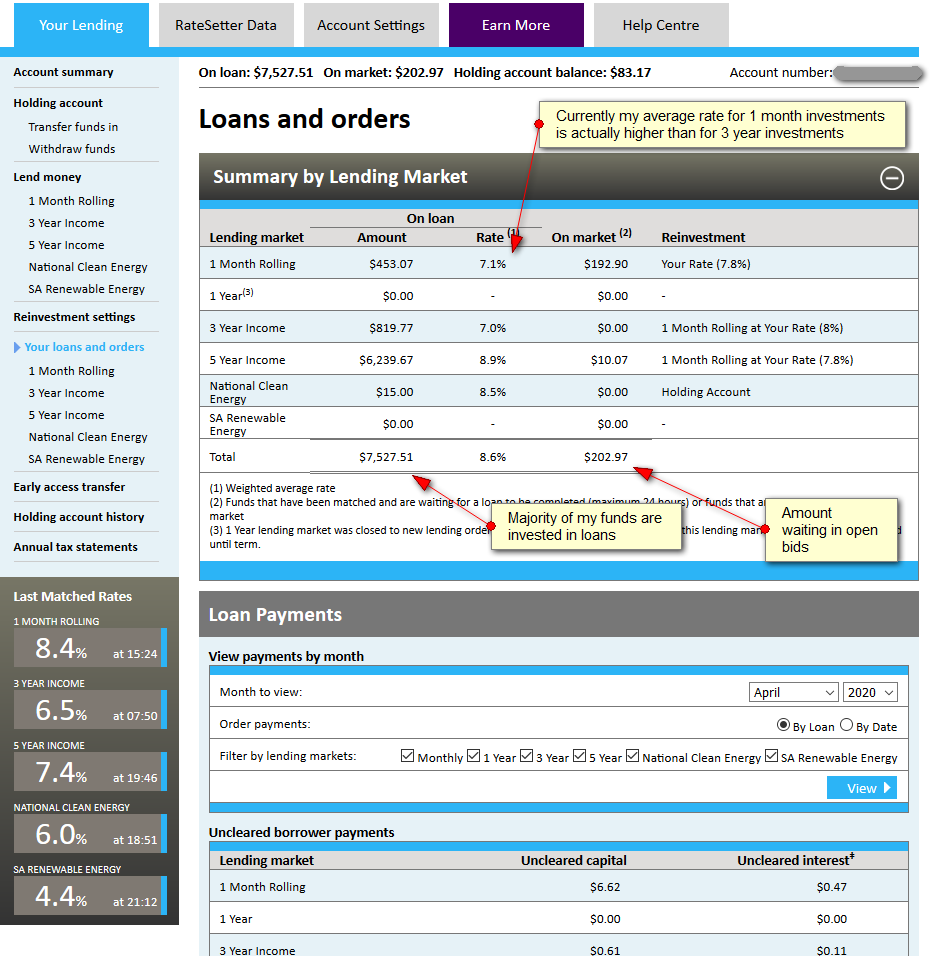

I now reinvest only at the 1 month market as the interest rate there is frequently peaking at higher rates than on the 3 or 5 years market. The following screenshot shows the current allocation of my funds at Ratesetter.

click on image to enlarge screenshot

What measures did Ratetter take in reaction to the pandemic effects on the market

In early March market turmoil caused temporary spikes of interest rate matches up to 19.9%. This was mainly caused by less lender money than usual offered.

Starting on March 23rd, Ratesetter imposed a maximum ceiling of 9.0% for the lending rates on all markets. Older bids that were higher were cancelled.

In the following days investors mostly reallocated remaining funds on offer away from the longer term markets to the 1 month market.

On (or about) March 25th, the remaining funds on the 1 month rolling market must have fallen below the funds replacement buffer of 300K AUD, invoking section 7.7. of the product disclosure section, meaning paybacks on 1 month loans are not return to investors but rather reinvested at the previous rate. While it happend a few time to me since then, it is not really a problem (even so it is relent at pre-crisis interest rates of 3.5%), as I had very little funds on the 1 month market.

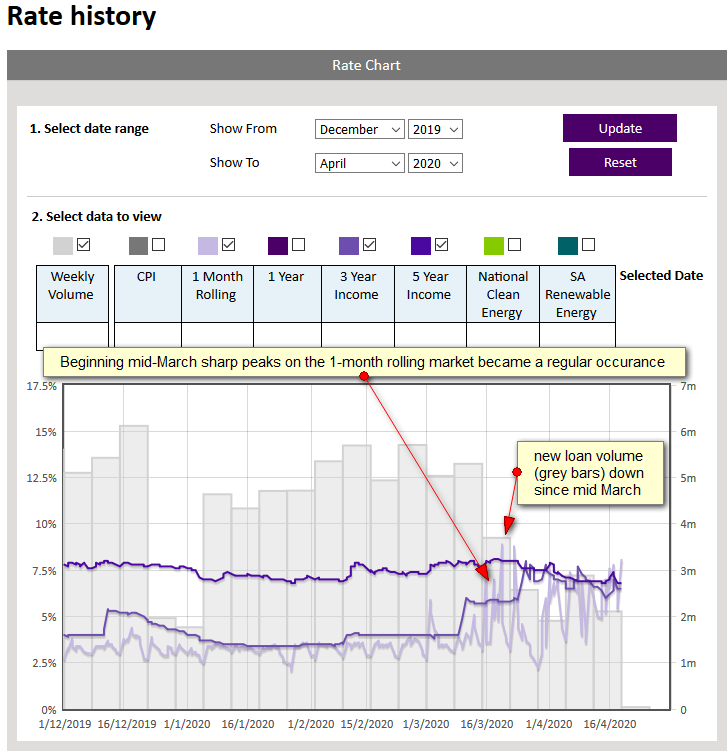

The following chart shows the turbulence starting mid-March, with rates bouncing up and down since then.

Overall the main impact on Ratesetter so far is the drop in new loan volume and the much higher interest rates on the monthly market. As far as I can tell repayments on the loans arrive regulary and if there is an impact on default rates it still lies in the future.

click on image to enlarge screenshot

Another big fallout of the crisis has been the forex impact. My home currency is EUR. Compared to that currency, the Australian dollar abruptly devalued in March. I even considered excahnging additional Euro to gain of the exchnage rate drap, but decided against it. The rate has moved back in the direction of pre-crisis levels since. As I have not withdrawn any money from Ratesetter the exchange rate fluctuations have not impacted me.

Source: XE![]()

Thanks for the analysis. I re-routed some of my EUR idle p2p money (mostly due to cash drag) to Ratesetter Australia in early March when the exchange rate was very favorable. I have also started using the 1-month market (for the first time) since the interest rates of this market have consistently beaten the interest rates of other markets. Overall, I am happy my Ratesetter portfolio, especially given the current chaos with most European (including UK) p2p platforms. Of course, I might be naively optimistic about Ratesetter because the real economic impact of Covid-19 has yet to hit us in the next few months and years. However, compared to the EU P2P platforms, Ratesetter Australia seems to have evaded the chaos so far.

I have been an investor with RateSetters in Australia for many years. As of 14th April data on the Provision Fund page shows $292.4M of loans outstanding of which $276.6M are current, meaning $15.8M of loans show some level of delinquency. The provision fund stood at $10.9M, whilst RateSetters own loan loss estimate is $13.7M. The adequacy of the Provision Fund to cover future losses is highly dependent on new loan flows adding a further $6.7M. The April data incorporates only the starting point loan delinquencies due to the pandemic, whilst new loan lending flows of $10M – $12M per month (see Volume data) since the onset of the pandemic will not replenish the Provision Fund to the tune of $6.7M. So at some point something will need to give.

In the UK RateSetters announced yesterday that the interest rate paid to an Investor would be half the contracted rate, with the other half used to support the Provision Fund. RateSetters argues this compromise is required to prevent a loss of Investor capital whilst still providing a return better than say bank deposits. Expect to see a similar move for RateSetters Australia soon.

I have done a similar analysis recently for those that are interested: https://medium.com/@j.kresling/56-months-of-lending-visualised-d8aee70c688f