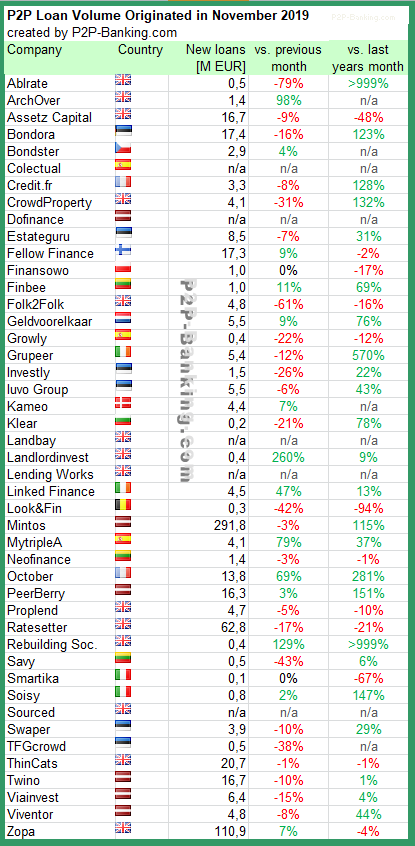

British p2p lending marketplace Thin Cats* announced that it will cease to offer new loans to retail investors. Thin Cats had facilitated about 556 million loans to UK business clients on its marketplace.

UPDATE: The headline has been edited compared to an earlier version to clarify that the company only stopped to offer retail p2p loans. This confusion resulted from the fact that the announcement below made no mention that the company will focus on institutional clients in future.

The Thin Cats announcement reads:

You have probably noticed that the number of new loans for investment

on the P2P platform operated by Business Loan Network Limited (BLN),

one of the ThinCats Group companies, has fallen significantly over the

last two years.Following a thorough review, we have concluded it is no longer cost

effective and practicable to raise funds in this way, so have decided to

close the P2P platform to new business and initiate a run-off process

for existing investors.This proposal has been discussed with the Financial Conduct Authority

(FCA) and we have made a voluntary request to the FCA that the

permissions to operate an electronic platform be closed to new business.Our decision to initiate the ThinCats P2P Platform run-off has had the

following impacts which became effective at 12.01am on 9 December 2019.No new loans will be offered on the ThinCats P2P Platform

The secondary market has closed and any loan parts listed for sale at the time of closure have been cancelled

No new accounts, including ISA accounts, can be opened

No new lender deposits can be acceptedPlease note that investors can continue to log in to their account(s) in

the usual way until such time as their account closes as part of the

run-off process.Crucially all of our existing systems and controls will remain in place

to ensure investors’ interest and capital is collected when due or

otherwise actively recovered. Investors can continue to withdraw any

cash balances to their nominated bank account following the usual lender

withdrawal request process. It is no longer possible to add new funds

to your account(s), although loan repayments collected on your behalf

will continue in the normal way.The effect on different categories of investor is detailed below:

1. Lenders holding performing loans

Lenders with status “A†loans that are performing as expected will

continue to receive interest and capital repayments in line with the

original loan schedule. We would encourage you to withdraw your cash

balances periodically.Following the closure of the secondary market, you can no longer buy or

sell any loan parts and any loan parts currently listed for sale will be

cancelled.For any performing loans that may subsequently become non-performing, these will be treated as described in section 2 below.

2. Lenders holding non-performing loans

For lenders with loans that are not performing in line with the original

loan schedule, we will continue to endeavour to maximise the returns to

lenders through our normal monitoring and recovery process. There will

be no additional impact from the introduction of a run-off period and we

will continue to email you with updates on specific non-performing

loans.Once we have secured the maximum value from non-performing loans,

lenders will be asked to withdraw any remaining cash balances and close

their account.3. Investors in Diversified Loan Portfolios (DLPs)

DLPs have a minimum Target Term, typically two years, during which it is

not possible to sell underlying loan parts. Following the closure of

the secondary market, performing loans within DLPs will no longer be

offered for sale via the secondary market towards the end of the Target

Term. Payments from these loans will, instead, continue until the loan

matures.We will contact you separately with the proposed run off schedule for

each DLP that you hold and you will continue to receive DLP statements

on a quarterly basis.Any non-performing loans within a DLP will be treated as described in section 2 above.

4. Registered investors with funded accounts but not holding loan parts

For investors that have cash balances in their ThinCats account(s) but

do not hold any loan parts, we encourage you to withdraw your cash to

your nominated bank account as soon as possible in the usual manner.Once your account has a zero balance we will close your account. If you

do not withdraw any remaining cash balances, we will contact you again

to remind you of the need to transfer all monies out of your account.5. ISAs

If you hold a loan or DLP within a ThinCats ISA, we will contact you

separately with details of the options open to you. It is no longer

possible to open a ThinCats ISA for the current tax year.6. ThinCats Lending Clubs (“TLCâ€)

All TLCs have now come to the end of their term and those that remain

open are still to receive future realisations from non-performing loans

in each portfolio.Once all possible realisations have been achieved the respective TLC will be closed and you will be notified accordingly.

In summary

The main impact of the platform run-off process is that no new loans

will be offered on the ThinCats P2P Platform and it is no longer

possible to open a new account.In most other aspects, other than the closing of the secondary market,

the platform will continue very much as now: you will continue to

receive interest and capital repayments for performing loans and we will

continue to monitor loans and invoke recovery procedures in the normal

way. You will be able to log in to your account in exactly the same way.We are committed to treating all customers fairly during the run-off

process and recognise it may raise a number of questions with investors.