Estonian property marketplace Reinvest24* will launch its secondary market (buying and selling among investors) next week. On Reinvest24 investors can invest into the equity of property and then participate on monthly rental payments and potentially capital gains at exit (if the property is sold). The secondary market feature had been first announced more than a year ago, but has been postponed several times. Now I was given access to the demo system, where I could try out the feature with a test account. Main parameters of the secondary market are:

seller can list parts with discounts, premiums or at par

buyer pays 1% transaction fee

seller can list any shares they own (including those where payment is overdue or in default)

rental payments go to the investor holding the share at the time of payment (no split between seller/buyer)

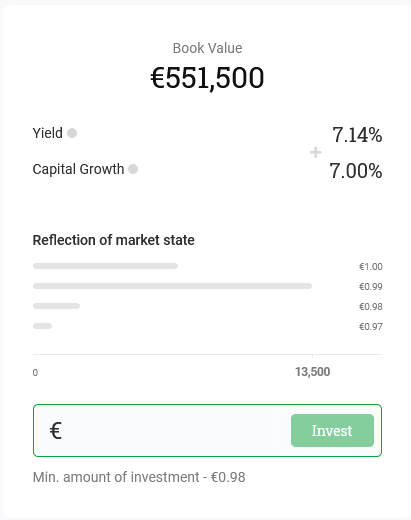

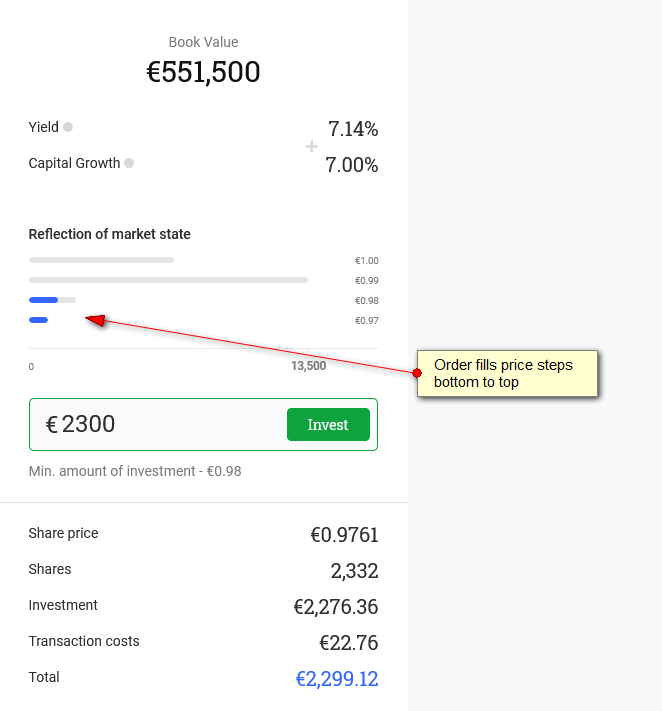

In the buying process the investor gets visualized the shares on offer (‘reflection of the market state) for a project at different prices by horizontal grey bars:

If the investor then decides to buy parts it looks like this:

At the time of my test, the demo version lacked filters, but Reinvest24* will add the ability to filter soon. The concrete launch date has not yet been set, but Reinvest24 expects it to be in the second half of next week.

I only have a small investment amount at Reinvest24 to gain first-hand experience with the marketplace. My investments there have performed satisfactorily so far through the pandemic.

While the features for the market are very basic it allows for increased liquidity for those investors that want it.

After several month of waiting since the first announcement, the Estateguru* secondary market will now launch. In the past weeks could participate in a closed beta test prior to the coming public launch of the market. Estateguru used this to get some feedback and to fine tune the wording (e.g. in the FAQ).

Overview of important facts about the Estateguru secondary market:

seller pays a 2% transaction fee

loans in all status can be offered, including late and in default

only the total loan part can be offered, it is not possible to split it and sell parts of it

seller can set the price at par or at premium. Discounts are not possible

buyer gets all repayments and interest after the sales transaction date

bought loans can not be resold for the next 30 days

each listing runs for 7 days. Unsold parts will be removed automatically

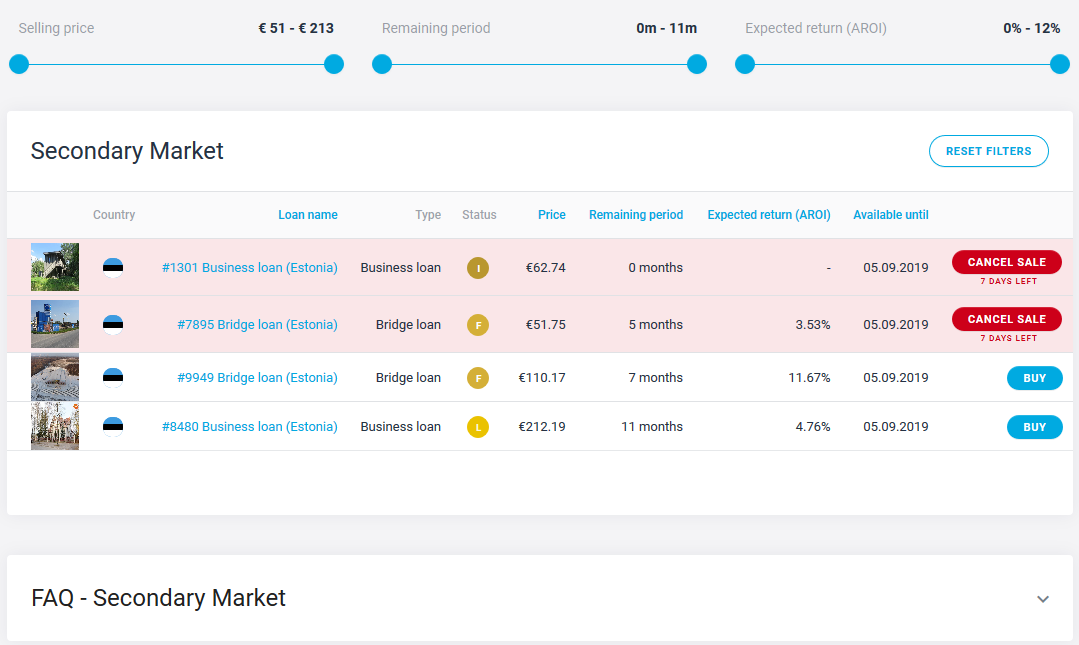

And now, without further ado, this is how the secondary market looks:

Fig. 1: Estateguru secondary market

On top of fig. 1 you can see the available filters. Also most columns can be used for sorting. The red highlighted loans are parts I listed for sale. I’ll now show you the steps necessary to sell a loan.

First I consented to this notice for activating the secondary market.

Fig. 2: Activating the secondary market

Then I went to my portfolio, selected the loan, I wanted to sell and clicked the “Sell” button on the right. Now I got to this screen:

Fig. 3: Setting the sales price

There is a slider on the upper right for the sales price. It is preset to 2% premium, to recover the sales fee. I set a higher premium here. Below the price the AROI for me (the seller) and the AROI for the buyer is shown. As the AROI is prominently featured in the market overview (see fig. 1) it is an important criteria for the buyer. And 3.56% is probably to low to achieve a sale. In fact this part did not sell in the 7 days (the other listed part #1301 did sell, see Fig 5.).

Here is the Estateguru AROI definition: ‘AROI (annualised return on investment) is an estimated annual return based on the total return on investment’.

After I clicked “Sell my claim” there is a screen for entering the password.And after that a display where Estateguru confirms that the loan is listed for sale

Fig 4.: Email I received notifying me of a successful sale of a loan

I like the overview table of the secondary market. As improvements I suggest to display the premium percentage and to allow filtering by status. Maybe that will be added in the next release. I also asked if they could add the ability to trade at discounts. The reply was that they wanted to offer an easy opportunity to sell loans and not overcomplicate the tool.

My first impression

The secondary market delivers what it aims to do: allow an early exit by selling loans. The 2% fee is relatively high, I expect that will keep the traded volume low. Sellers of late and defaulted loans will have to carefully consider the price set, as I think that with any positive news updates on the recovery status of the loan, the loan part will be bought, before the seller has a chance to read and react to the update.

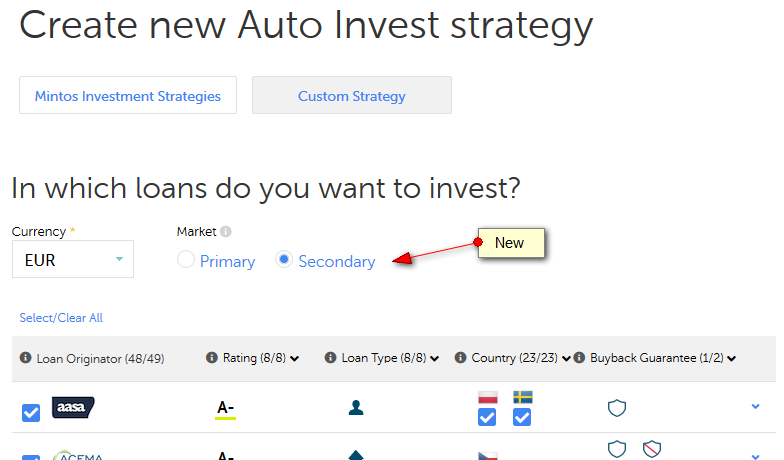

Mintos* has announced a new feature – the autoinvest can now be used to buy loan parts on the secondary market too. I am setting up a new autoinvest to test it and am curious how many loan parts I will be able to acquire with this new feature. Just like on the primary market there are many selections adjustable.

Screenshot Mintos Auto Invest Secondary Market

Mintos will roll out the new feature to all investors on Dec. 3rd. Only selected investors will be unlocked earlier. Mintos* says investors can deposit an additional 5,000 EUR to add to their balance to get early access. Also investorswhich have invested at least 50,000 EUR will have early access.

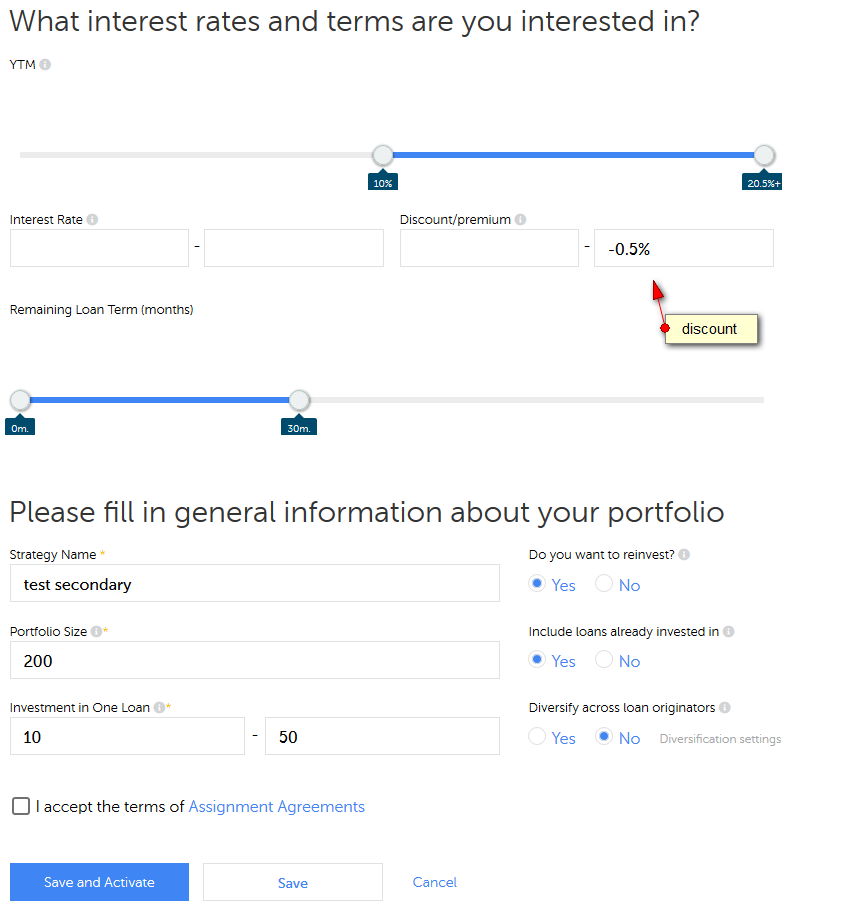

Screenshot: Further details of Mintos Auto Invest Secondary Market

For the further details of the test, I set the secondary market auto invest to buy loans with at least 10% YTM, a maximum loan term of 30 month and at least 0.5% discount. I left the interest rate open, as the restriction is not really necessary for me in this case in conjunction with the YTM and the discount.. For ‘Do you want to reinvest’ and ‘Include loans already invested in’ I choose ‘Yes’. I deselected ‘Diversify across loan originators’ as I want to buy all loans that match these conditions.

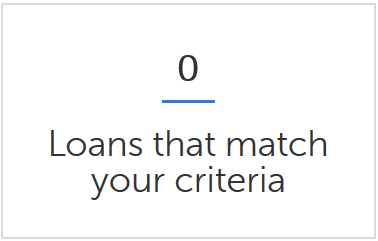

No surprise – no loans match my selection. Loans with these criteria selected by me have been bought up fast in the past, even before the introduction of this new autoinvest. I do wonder, which investor will get priority in case there will be autoinvests of multiple investors matching a new loan up for sale. I expect this new autoinvest will be a popular feature amongst Mintos* investors.

Not many but a few other p2p lending platforms offer autoinvests for their secondary markets too.

Crowdestate is an Estonian p2p lending market place focussing on property. It is somewhat compareable to Estateguru or Lendy, the difference is that Crowdestate has a wider mix of offers, including unsecured debts or equity. I published an interview with the Crowdestate CEO last year.

The projects usually come with a term of 1 to 2 years, occassionally a bit long or shorter. There were not that many projects in the past . Often only 1 or 2 a month. Recently the pace has been picking up. Investor demand strongly outweights supply. Often the autoinvest bids fill a new offer instantly, if not then it is often filled within a hour of coming on the plattform. There are no fees for investors. Only a few offers pay interest during term, with most accruing interest to be paid at the end of the term. There are no fees for investors.

I only invested in a handful of projects to gain some experience. Today Crowdestate launched a new look for the website. This is how my small Crowdestate portfolio is displayed:

My Crowdestate portfolio – click for larger view.

Crowdestate secondary market

Today Crowdestate launched a secondary market. There is a “Sell Shares” button besides each of my active investments. To test it, I just offered one of my loans at a markup. The marketplace allows sellers to set markups or discounts.

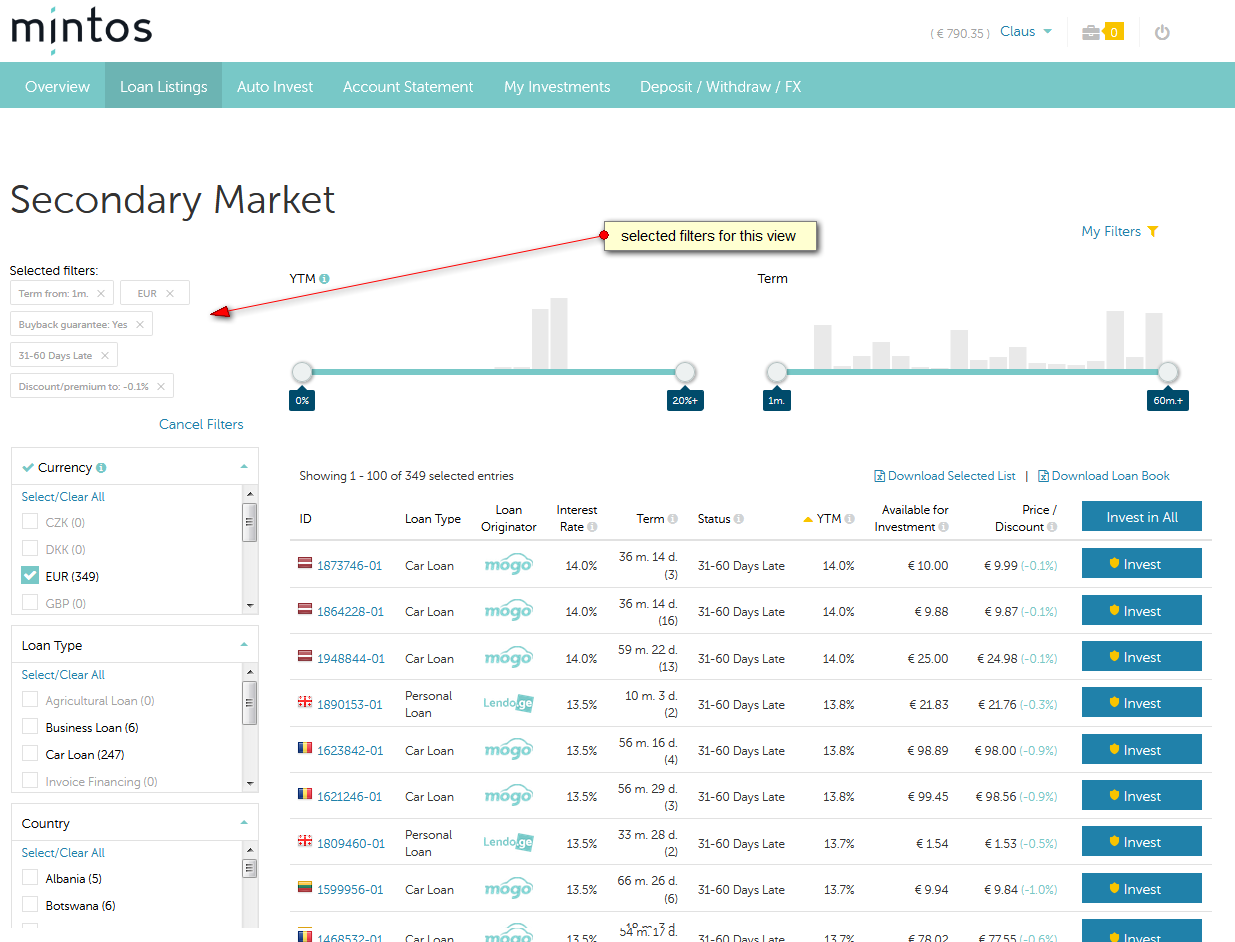

On the p2p lending marketplace Mintos there is a very large and active secondary market. In my previous article I described that the YTM calculation shown on the secondary market is based on the assumption that the buyer holds the loan part till regular end of term and the buyer will achieve a higher yield, if he buys at discount and the loan is repaid prematurily.

In the article I will look into a possible strategy on the Mintos secondary market: buying overdue loans at discount.

In a first step I sort/filter the buyback loans to only have those at discount that are very late (31-60 days overdue).

Click on image for larger view

I get a result of 349 loans with various discounts and an YTM of up to 14%. Not surprising for me, many of the loans listed at the top are Mogo loans. These are less attractive for buyers with this strategy. Why? Because they actually have a lower probability of defaulting. The paradox of this strategy is that the buying investor actually wants a high probability that the loans he buys default because that will boost his yield.

So in the next step I sort/filter to exclude Mogo loans. I also exclude loans that have a low YTM. This, because there is a chance that they do payup and then the buyer might be stuck with the loans for longer than 30 days.

Click for larger view

Finally let’s change the filter to require a minimum discount of 0.3% and there are 21 results:

Click for larger image

What would a buyer get?

If these loans do pay up and then run till regular maturity date, then he recieves a yield of 12.4% to 13.8%. Decent, but not very high compared to other Mintos loans.

However there is a chance of at least 50% that these loans will default and are bought back within the next 30 days. If that happens to a loan, that a buyer bought at 0.3% discount, it will boost his yield very roughly by more 3.6% (0.3% for 30 days multiplied by 12 to get annual effect). Likely it is more because the next payment date will be less than 30 days away. But even taking 3.6% the yield will be around 17%.

Looking at it, it is obvious that discounts as high as possible are preferable. The loan with the 0.6% discount would mean a boost of very rougly 7.2% yield on top (0.6*12). So that could lead to about 20% yield.

I have taken the screenshots for this article just at a random point in time. Higher discounts do happen and discounts of around 1% are not a rarity.

This is certainly not a strategy for a beginner at Mintos and it requires time and monitoring, but it is a frequently used strategy when investing on the Mintos secondary market.

Not yet investing on Mintos? Get cashback!

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

On the Mintos p2p lending marketplace the majority of investors invest on the primary market into loans, either manually or via autoinvest. But for the 29% of investors that do invest on the secondary market picking loans presents them with a huge choice of about 125,000 offers (no typo, really 125K loan parts on offer!).

Main characteristics of the Mintos secondary market:

no transaction fees

selling at discount, par or premium, adjustable in 0.1% increments

no minimum amount for buying, a buyer could make a partial buy of 0.01

seller and buyer each get credited interest for the amount of days they hold the loan; that means seller continues to accrue interest for an offered loan until the part is sold

good filtering

Sorting on the secondary market is preset to YTM (yield to maturity). This figure shows the yield the buyer would make (taking into account the discount or premium), if he would buy the loan and hold it to regular (!) maturity. Emphasizing regular is important since many of the buyback loans end prematurily, which would result in a higher than shown yield for loans listed at discount or lower than shown yield for loans offered at premium.

Generally YTM is a very good criterion for sorting an filtering on Mintos the secondary market and it is my most important criterion.

However there are exceptions, when taking the shown YTM at face value is not advisable.

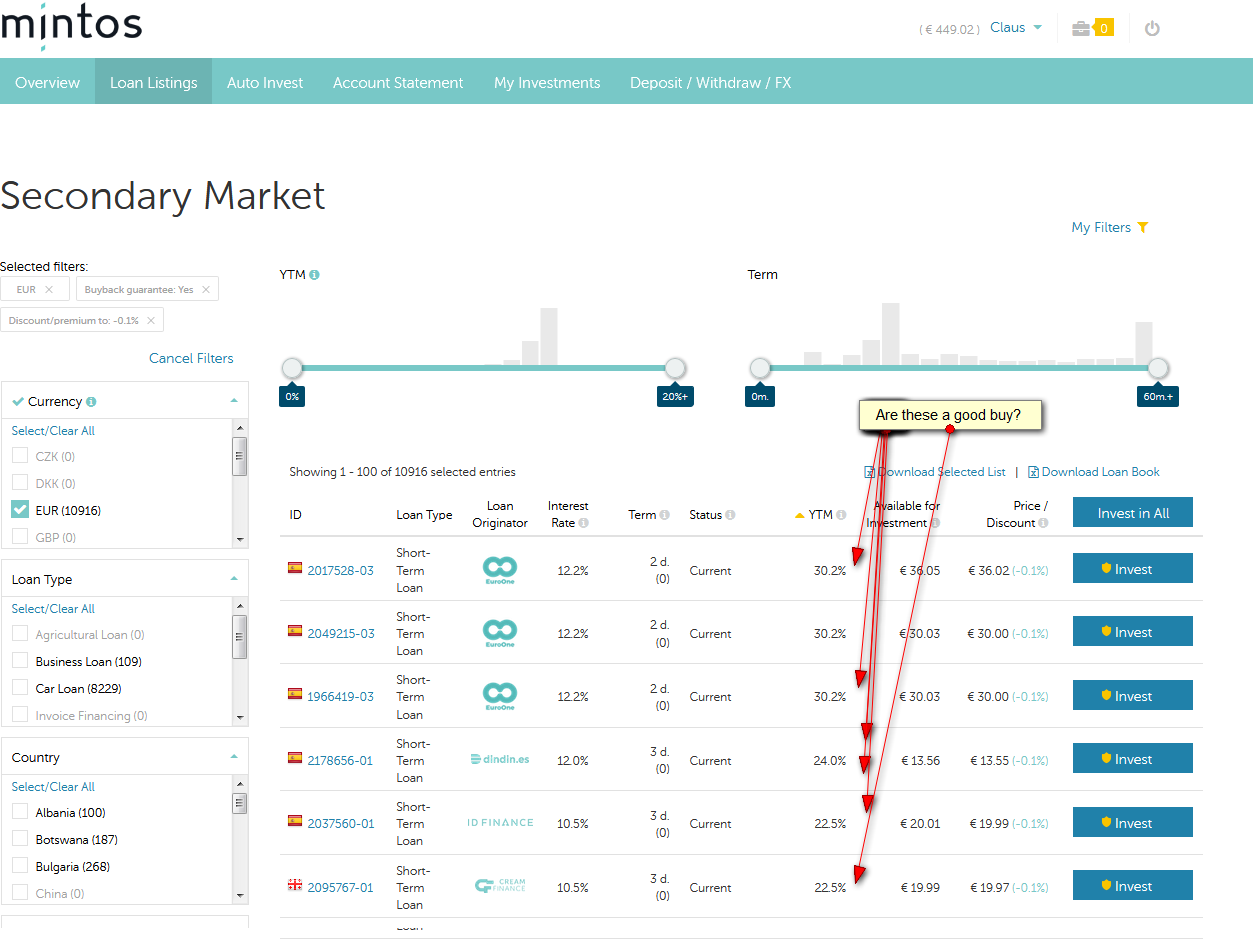

Click on image for larger view

Look on the loan offers in the screenshot above. All are offered at 0.1% discount and the YTM is very high with 22.5% to 30.2% Let’s neglect for the moment that picking these loans would cost the seller time, which if he puts a price tag on time spent would not be worthwhile as these loans are very close to maturity and he would only earn interest for a few days.

The high YTM is caused by the discount in combination with the fact that there are only 2 or 3 days left to regular end date of loan (term is 2d or 3d). The calculation is correct, but there is one caveat. For the shown loans there is a very high probability that they will miss the payment and therefore run an additional 60 days until they are repaid under the buyback guarantee. If that happens the remaining actual loan duration would be 62 or 63 days and the impact of the 0.1% discount on the YTM would be much smaller. The resulting YTM would be somewhere around 11 to 13%. So they would not be a good buy and there are much better offers on the secondary market.

Another example to look at:

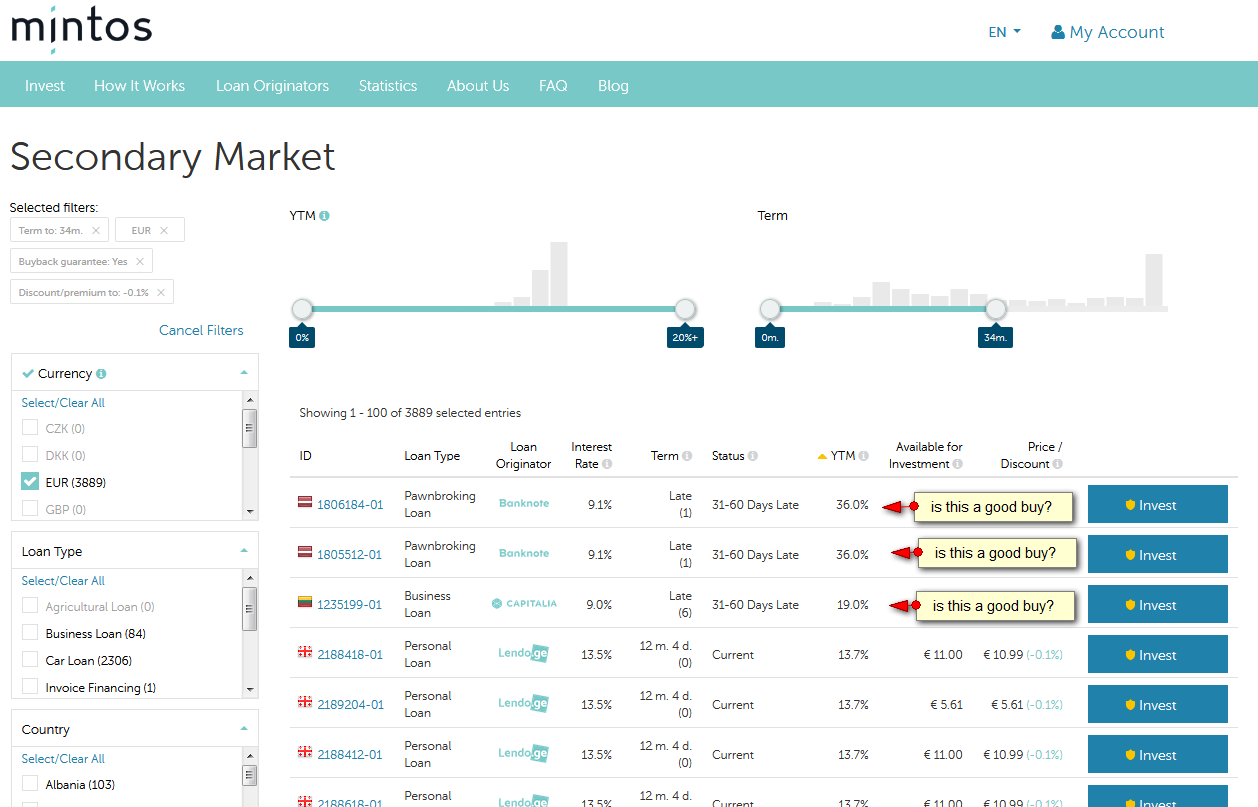

Click on image for larger view

These loans are shown with an even higher YTM of 36% and offered at a discount of 0.1%. They are late, but with a buyback guarantee, so aside from the originator risk there is no default loss risk. But for these late loans Mintos calculates the duration to the regular end of maturity with only one day, which in combination with the 0.1% discount results in the high YTM (simplified: 0.1% per days * 360 days results in 36% yield)

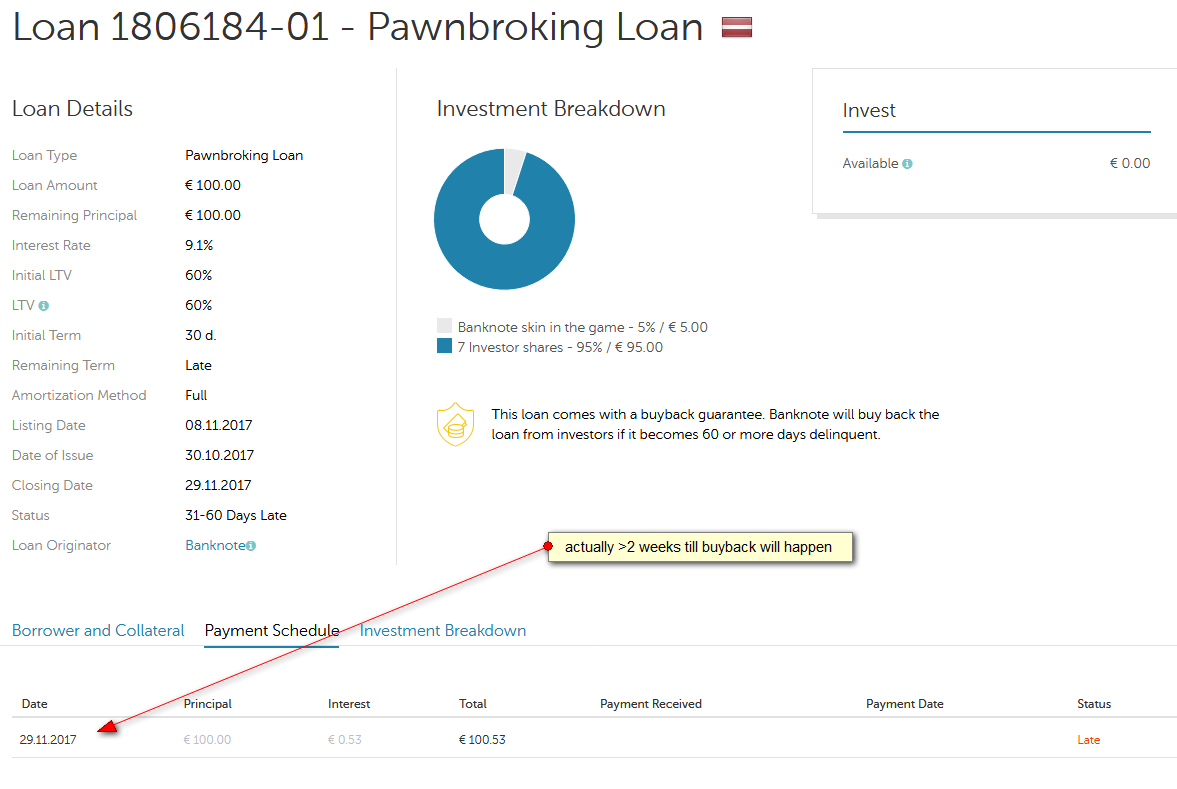

If I look into the details of one of these loans, I see that the next payment is actually scheduled in two weeks. So the loan will be repaid then since it is already in the status of 31-60 days late (there is a very low probability that it will repay earlier if the borrower repays).

Click on image for larger view

With two weeks remaining the effective YTM for a buyer is not 36% but rather around 12%. Again there are offers with better YTMs on the secondary market.

Conclusion

On the Mintos secondary market YTM is an important figure to regard for buyers. However, while it is calculated correctly under the definition, there are a few cases where the shown figure alone might be misleading especially in case of loans that have less than 1 month remaining loan duration. The shown YTM always applies to the case that the buyer would hold to the loan to the regular maturity date.

Not yet investing on Mintos? Get cashback.

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.