Breaking news: p2p lending platform Mintos* will run an equity crowd on british equity crowdfunding platform Crowdcube. Mintos states ‘As far as startups go, Mintos has raised very little capital so far. We have grown to become the market leader in continental Europe largely fueled by our own revenue. We see a huge market opportunity ahead of us, and to accelerate our growth and develop new products we are raising money. Our fundraising round includes both venture capital and crowdfunding. ‘.

No details regarding the amount to be raised or the valuation have been shared yet. The pitch is set to go live in late November

Orca Money is currently running an equity crowdfunding campaign on Seedrs to raise 500K GBP at a premoney valuation of 1.7M GBP. Anybody can invest in Orca Money shares with a minimum investment amount of 10 GBP applicable. I interviewed the Orca CEO Iain Niblock

What is Orca Money about?

Orca is an aggregation platform, allowing investors to invest across a range of peer to peer lending (P2P) platforms, lending sub sectors and a large number of borrowers. We further offer independent investment research, providing confidence to investors when making decisions.

Currently investors are investing directly on P2P platforms. This makes building and managing a diversified portfolio frustrating. We centralise this process by allowing investors to research, build and manage their portfolio from the Orca platform. We provide the P2P platforms with a source of retail investors.

Investors can review the performance of their portfolio, diversify their risk and earn the attractive returns that the sector offers.

What are the three main advantages for investors?

Risk adjusted returns: We offer an investment return to our users which is reduced in risk through diversification. By allowing investors to invest across multiple P2P platforms, lending sectors and a large number of borrowers, we facilitate easy diversification.

Reduced admin burden: Orca manages all fund deployment, email communication and performance data aggregation. Investors can login to their personal Orca dashboard and view a breakdown of their portfolio, as well as an aggregated view of their investment performance.

Automatic portfolio build: Orca has been producing independent analysis on the market for the past three years. We have conducted due diligence in the market and curated a portfolio for investors to invest through. This removes the hassle from P2P investing.

You are currently raising money. Who are you raising from and what do you plan to use the capital for?

Our investment is open to the public on the Seedrs equity crowdfunding platform. Investors across the EU can register and invest in the Orca business. The proceeds will allow us to expand our userbase, integrate with more lenders and to further develop the functionality of our platform.

Prior to launching the crowdfunding campaign, we secured a portion of this investment from two institutional funds based in Northern Ireland and a number of leading angel investors. It’s great to be combining these investors with crowd investors.

Why have you selected Seedrs for your equity crowdfunding campaign?

A number of our customers mentioned that they would like to invest in Orca’s business. We’ve gained incredibly valuable feedback from these customers and, ultimately, we wanted to give them an opportunity to own shares in the business. We hope that this campaign will attract further investors and customers to do the same.

Personally, I’ve tracked the equity crowdfunding market closely for many years and I’m now genuinely excited to be leading a campaign. Seedrs was an obvious choice as they have facilitated funding for a number of other P2P platforms.

One benefit of Seedrs is that investors invest through a nominee structure. The Seedrs nominee structure holds and manages the shares on the behalf of the underlying investor. For the investor, this means the nominee can track and monitor shareholder rights as a collective. For the company, this reduces the administrative burden of having a large shareholder base.

Where do you see Orca Money in 3 years?

We aim to evolve into the hub for P2P investment research, investing and portfolio management. Investors will be given access to credit investments across the EU, originated by P2P platforms and other non-bank lenders. The functionality of our platform will increase, delivering a fully functioning investment aggregation platform.

Orca is a differentiated product in a rapidly growing market.

Name one fact that makes your pitch a better investment than any other pitch on Seedrs.

In comparison to other Seedrs pitches we believe our valuation is very good value. This was set by institutional investors based in Northern Ireland where valuations are generally lower than other parts of the UK and in particular London. I’d expect the valuation to rise substantially during any subsequent rounds.

Investly is an invoice financing platform which helps businesses from the UK and Estonia release cash from their long payment term invoices. We’re a marketplace that connects investors to companies that need short term capital, which we issue against their receivables. We have offices in London and Tallinn.

What are the three main advantages when investing in the invoices?

Liquidity – Investly is quite different compared to most platforms because the investment period is only 30 to 40 days on average. This means you can convert your investments into cash within a month by simply halting further investments.

Return – Historically investors have earned 11-12% annually on invoices. I believe every investor should have a portion of their funds allocated to P2P investing because of the higher return and additional diversification.

Added value – Invoice finance is helping small businesses who are growing fast but fail to get the support they need from local banks. The direct impact is clear – invoice finance has helped our customers grow faster and create more jobs. This would not be possible without investors.

What are the three main advantages for companies selling the invoices?

Most of all, faster business growth. We discovered that Estonian customers who are leveraging access to working capital are able to grow their turnover by 18.3%, while turnover growth benchmark equals 7.6% (Investly internal analysis, growth benchmark from Statistics Estonia report 2017) But access to working capital is not just numbers in spreadsheet, but most of all it’s opportunities that business can take: hire more staff and win new contracts, get better supplier payment terms by offering early or up-front payment, ensure prompt payment for employees and subcontractors.

What ROI have investors made on average on the platform in the past?

On average investors have earned double digit returns in both markets. The net return on Estonian invoices has been 11.2% annually and in the UK it’s been 12.6% annually.

What is the procedure, if a company is late in repaying the invoice?

To ensure collection is as fast as possible, we rely on early action and automating notifications to debtors. If the debtor doesn’t pay within 30 days of the due date, we have the right to ask the seller to repurchase the invoice from investors. We also ask for a personal guarantee from one or several of the directors of the seller company. This means that if the company cannot pay, we can ask for payment from the directors.

Investly is the biggest p2p lending marketplace for invoice financing in Estonia. How did you achieve this position?

We use personal approach and always try to find the best solution for our customers and investors. That professional customer service constantly provides us a leverage over banks and competitors. Also, quick decision – we present an offer within one working day. This is something that many of small businesses can’t expect from traditional lenders. On top of that, we have flexible pricing, which we’re able to use thanks to loyal and engaged investors community.

Investly is also operating in the UK. Is it complicated to operate in two different markets simultaneously and which of the two markets is more attractive for future growth?

UK is the largest factoring market in Europe with €327b worth of invoices financed every year. For comparison, France is second with €268b/year and Germany is third with €217b/year. This is where the biggest potential is. However, traditional sales and marketing channels towards our target customers are extremely crowded with thousands of B2B service providers trying to sell them products. We have to be more clever about acquiring customers there. Open Banking enables us to do that.

Estonian businesses finance only €2.5b/year, but due to the connected infrastructure of public and private registries, we can reach our customers much more easily. Also, there’s fewer providers in Estonia and we’re creating a lot of the market ourselves as factoring hasn’t been available for them in the past.

Having built Investly for four years, what do you deem the biggest assets of the company?

We have gained a detailed understanding about the problem we’re solving. It’s not specific to any geography. Businesses across Europe and elsewhere in the world are struggling with the lack of working capital. It seems that our product offering helps to solve that problem more simply than traditional lenders.

Four years is typically a good time to become an expert at something. We have also build a strong team to execute our mission. We’re experts at invoice financing.

Also, we’ve managed to get a good set of advisors on board to help us build the marketplace and secure future rounds of financing if needed.

What role does ‘Open Banking’ play in the near future for Investly’s further development?

Open Banking is a technical enabler. Businesses can now choose freely between their bank and 3rd party providers to solve their specific financial needs. It’s done in a secure and easy-to-use way.

This has gotten banks looking into how they can continue to be profitable in this new environment. Completely new types of business models are emerging and we’re proud that Investly is one of the early pioneers to set the path for others. Being part of the Open Banking sandbox in UK helped us to be one of the first ones to integrate with banks like Barclays, HSBC, RBS, Lloyds and Santander.

We’re going to use these integrations to form partnerships with traditional lenders so we can serve our customer without them necessarily having to change their provider.

You want to raise new funding on Seedrs. Why did you decide to use crowdfunding for equity rather than traditional routes?

Throughout the years we’ve received multiple requests from our marketplace investors to participate in our equity financing round. They’ve been giving us a lot of valuable feedback when we’ve developed our product and directed our credit model. We’d like them to get a chance to be part of Investly mission as we continue to grow.

With traditional equity financing, we’d be overwhelmed by administrative work to get the round closed and to manage those relationships later on. Seedrs has provided a good platform on which we can do that efficiently.

What is the value proposition for investors? Do you aim for a stock market listing? What is the likely time horizon?

Get to participate in our valuation growth. The interest you earn on the marketplace is quite stable, but the potential upside on the equity investment is much higher.

UK based investors can take advantage of the EIS scheme. It’s quite a big incentive on the tax side.

Seedrs provides a secondary market, which helps to create liquidity for our shareholders. This way, you don’t have to wait for years until the startup makes an exit or files for IPO.

Is Investly profitable? If not, when do you expect to reach breakeven on cash flow.

Operationally, we’re quite close to breakeven. The target is to get profitable in core activities in the next 6 months after fundraising round closes. But on a company level we will still be investing heavily into building out the integrations with banks to execute the momentum we’ve managed to build up.

For which activities does Investly intend to raise the used funds?

Partnerships and further automation. Few years ago, all the banks would turn us down when we approached them with suggestion of cooperation. But with Open Banking, this is window of opportunity for both of us: Investly provides working solution with better experience and price for customers, banks acquire competitive leverage on the market and are part of this fintech revolution. Therefore, funds from this round will be used on product developments which will allow us integrate with banks infrastructure and automate our processes even more with the increase in volume.

Where do you see Investly in 3 years?

Investly will be the major provider of invoice finance to businesses across Europe. It’ll be partly through partnerships (invoice finance powered by Investly) and partly through building out our own brand by continuing to deliver superior customer experience.

With that scale, we will have had enough data to build up a narrow AI for credit decisions. We have followed our roadmap for getting there. We’ll be better able to score companies and collect payments than competitors.

Investors will have access to debtors across Europe, which enables them to achieve a good diversification of currencies, countries and sectors.

Once we’ve received that scale, we will be able to deliver the best financing rate to businesses with our marketplace model, where banks are lending alongside with our investor community.

The Crowdproperty marketplace was launched in 2014 and the company has since funded 10.7 million GBP in property loans. All loans are secured by a first legal charge against the property. The company says no investor has incurred any losses so far. The company received full FCA authorization in October 2017.

Crowdproperty states it has unique proprietary access to the largest property network in the UK, the Property Investors Network (pin), which provides competitive advantage in terms of high quality deal origination and has enabled the proof of the business with limited marketing investment to date.

Crowdproperty claims that it’ is already profitable with more favourable economics than peer to peer platforms in consumer and SME marketplaces owing to shorter average loan lengths, higher average loan sizes, borrower frequency/retention and achievability/sustainability of fee levels. With a gulf now emerging between property-based peer to peer lenders that are gaining traction versus those struggling at the sub-£5m level, the team aims to become the market leader in project-based finance direct to SME property professionals whilst simultaneously providing competitive first-charge secured returns to its retail pool of lenders. ‘

CEO Simon Zutschi told P2P-Banking: ‘I am delighted that we have now proven this model of helping successful property developers to fund their projects, whilst helping investors gain a secured return on their money. All of the recent project launches have been quickly funded up by our eager and loyal base of lenders, which clearly demonstrates the traction we have built in our brand. Over the last year, we have focused on our platform technology and processes, and now we are ready to scale this business to its full potential. This will not only benefit our lenders, but also help and support SME developers, who often struggle to raise funds from hesitant banks, to access the essential funding they need to help reduce the UK housing crisis’.

Plum is another fintech that makes use of Ratesetter’s products through a cooperation. Plum is bot on Facebook messenger designed to automate savings for the user and to invest money on his behalf. Savings can currently be invested in Ratesetters rolling market. Plum is currently pitching to raise 700K GBP through a convertible with a valuation cap of 5M GBP on Seedrs. Watch the video for more information on the Plum product and pitch. The minimum investment for this equity crowdfunding campaign is 10 GBP. The pitch is EIS eligible (UK residents). Other investors include 200K US$ invested by VC 500 Startups. This pitch is not yet officially launched on Seedrs, but already open for investments. You can use P2P-Banking’s free notification service to be alerted of upcoming Seedrs pitches early and review them ahead of the crowd.

Competitors of Plum include Digit, Qapital, Clarity, Albert, Squirrel, Cleo and Savedroid.

The Plum pitch deck is informative reading. To request that, login, click on ‘Documents’ in the pitch, and send a message to request the pitch deck.

Another example of an innovative cooperative cooperation making use of products of a p2p lending service is Commuterclub.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

For decades buying houses, refurbishing them and selling them at a higher price and moving on to the next property seemed like a popular sport to Brits. Many of them see properties as investments and with house prices mostly moving up lots of them aimed to finance a property while they were young and then build a portfolio. With limited supply of new land with planning permissions this strategy worked well most of the times in the past, except when the market overheated and a real estate bubble popped.

There are downsides to this do-it-yourself approach:

Concentration of risk in one or few properties: if they underperperformed for what ever reason, the yield was sub-average

A lot of money, time and work required. The investor had to do everything itself as a landlord

Selection of new properties usually limited to a small region the investor lives in

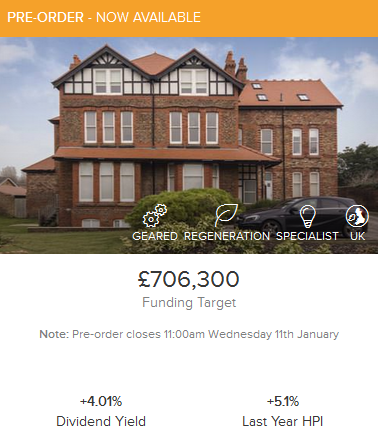

British platform Property Partner allows everyone to invest in British properties from a minimum of 50 GBP. Investors select a listing, invest into a SPV (special purpose vehicle company) that pools the investment in the property. The SPV collects rental income and pays dividends to investors monthly. A useful table of the past achieved rental income can be seen here. In the green marked cases the actual rents are higher than the original forecsts. Potentially investors can also gain, if the value of the property rises.

The time span of an investment is 5 years, however investors can try to sell their parts on the secondary market, which allows discounts and premiums any time.

The platform allows the investor to diversify across multiple properties easily. The fee is 2% for investment (in new listings or buying through the secondary market). For management, advertising and letting Property Partner charges 12.6% of gross rent.

So far Property Partner has funded 311 properties for 43.9 million GBP with 9.100 investors participating.

For new listing there is a pre-order period, where bids are collected. If the listing is oversubscribed then each investor is allocated a lower proportionate amount of shares.

Each listing contains an investment case desctiption, property details, a floor plan, financials, a solicitor’s report and a surveyor’s report as well as the house price index (HPI) information for the area.

For the secondary market there is a ‘data view’ section which lists key indicators for the parts listed for sale.

Investors that do not want to pick listings can set up the auto-invest option which will automatically invest an amount the investor sets each month in 5 properties.

Investing from abroad

Property Partner allows foreigners (except for US residents) and corporations to invest. If you do not live in the UK but see the UK housing market as an investment opportunity Property Partner is a hassle free possibility to invest in british real estate. Non resident investors should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

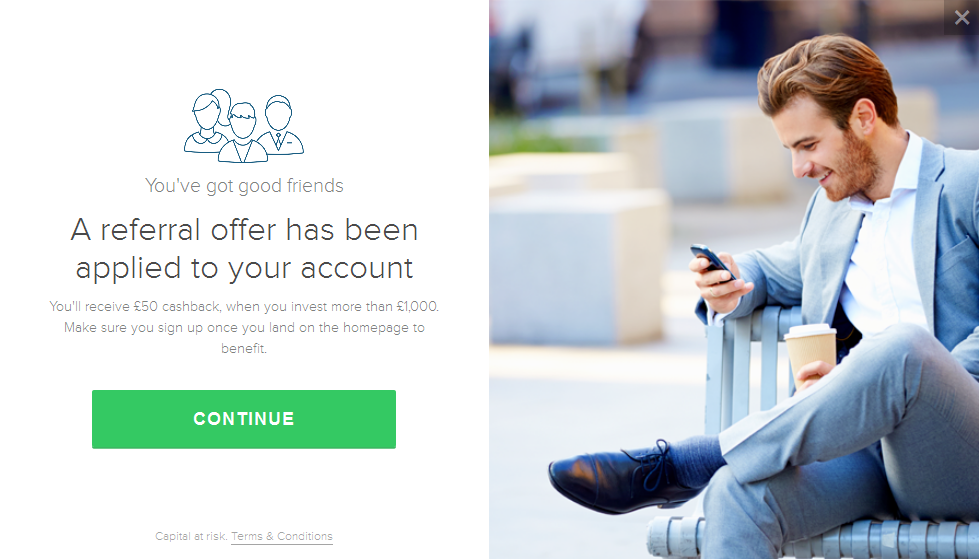

How to get 50 GBP cashback at sign-up

To get 50 GBP referral cashback, when you invest more than 1000 GBP sign up now via this link . To see available promotions by other platforms visit our cashback offer page.

Property Partner cashback confirmation at sign-up. To see it follow this link and sign up.