At registration put WEALTH into the promo code field (was pre-filled when I looked).

Between August 28th and September 30th invest in notes, bonds, property and/or ETFs. The amount you invested on September 30th determines the size of the bonus (see table below).

The money has to stay invested until Dec 31st 2025.

Bonus will be paid out on January 10th, 2026

Full bonus terms are linked on the Mintos* website.

This translates to up to 2% cashback bonus in 4 months time.

I started investing over 10 years ago at Mintos* in January 2015. I am very satisfied with the results I achieved since. You can read all my previous Mintos articles on this blog.

‘Earn rental income starting from €50 investment’. As of today, Mintos* is advertising a new offer that it describes as passive property investing.

In fact, investors are investing in Real Estate Securities, which are an interest-bearing debt security backed by underlying bonds. Purchasing Real Estate Securities entitles the investor to receive interest payments for the Notes whenever net property payments are made on the underlying bonds and repayments when the underlying property is being sold.

So to summarise: If everything goes according to plan there is a monthly interest payment, which is fed from the rent, and at the end a payment for the increase in value, which is estimated but not guaranteed.

The underlying properties are located in Austria and come from the Bambus.io portfolio, which acquired them as part of a partial purchase. The older owners are therefore still living in their homes and are now paying rent for the sold portion (kind of a reverse mortage).

Illustration: The first property offer in the new Mintos product as an example (click for larger view)

Advantages for the investor:

Good opportunity for diversification

These are rented residential properties (and not projects of property developers or commercial properties as with some other platform offers)

Invest from as little as 50 euros

Regulated offer

Disadvantages for the investor:

Very long term (20 years in the example)

rather illiquid (although a sale via the secondary market is possible, it is questionable whether there will be demand)

No information on how the valuation was carried out and how the increase in value was forecast

The property from the first offer was valued at 317,500 euros. Mintos* does not provide any further details. Brief research (e.g. here) shows that the valuation of 2,500 euros/m² is not overpriced. According to the Bambus FAQ, the market value of the partial purchase carried out by Bambus is determined by an independent expert. It can be assumed that the market value determined in this way corresponds to the property value stated on Mintos.

Unfortunately, there are no further details on how the increase in value was forecasted. According to the prospectus, Bambus, which has been operating since 2022, has not yet sold any properties. So there is no experience yet.

Is it worth it? My first impression

In my opinion, the interest rate offered is too low for the very long investment period. It is difficult for me to judge whether the increase in value has been realistically forecasted. After all, it could probably be enough to cover inflation.

Comparison with other investments

The question remains, why should investors use the Mintos* offer instead of alternative offers? I have started to build up a portfolio with Inrento* in the last few weeks. The property loans there offer a significantly higher interest rate of 8-9% p.a., interest payments are also monthly and there is also a payment for appreciation (1.5% p.a.). The advantage is the significantly shorter terms of 1 to 3 years.

Estateguru* also offers significantly higher interest rates of 9-11%. There is also a bonus of up to 2% on top for larger investment amounts. The terms are also often shorter at 12 to 18 months. Even taking into account the usual overdrafts of around one year, the investor is much more liquid than with the Mintos product.

Furthermore there are exchange-traded REITs as an alternative. These are much more liquid and enable broad diversification.

There have been plans at Mintos* for years to add ETFs to the product offering. But with the MiFID II license it seems that Mintos finally has its ducks in a row.

Mintos plans to offer ETFs and bonds later this year. I spoke with Elmars Ciganovics and with Martins Sulte in Riga about the plan. ETFs and bonds are a first step to broaden the product offer beyond loans and other asset classes could be added later.

There are not yet many details disclosed around the ETF and bond offer, here is what I understood:

initially there will be a small selection of ETFs from only one provider

Mintos will not charge investors any fees

the ETFs will not be bought through a stock-exchange but rather through a partner bank

I somewhat struggled to see the target audience for this product given that there are lots of established low cost brokers in many European markets. Martins sees the target audience in those Mintos customers that so far have not invested on the stock market but trust the Mintos brand and will take the first step with them with the benefit of manageing their investments in one place.

Personally I am not convinced that this strategy will succeed e.g. with German investors but maybe there are other markets. In any case it will be most interesting to watch.

So this is clearly a cross-selling strategy by Mintos where it will use the existing 500,000 investors to sell to initially. But further on passporting the license to other European countries will alow Mintos for the first time to aggressively step up marketing efforts there.

Martins pointed out the huge untapped potential he sees with saying that over 60% of American households are directly or indirectly invested on the stock markets whereas for Europeans this number is only over 30%.

And while Mintos* presents its position as market leader with confidence, Martins also pointed out that this volume is small when compared with brokers like TradeRepublic. So this seems to be the liga Mintos is aiming for next.

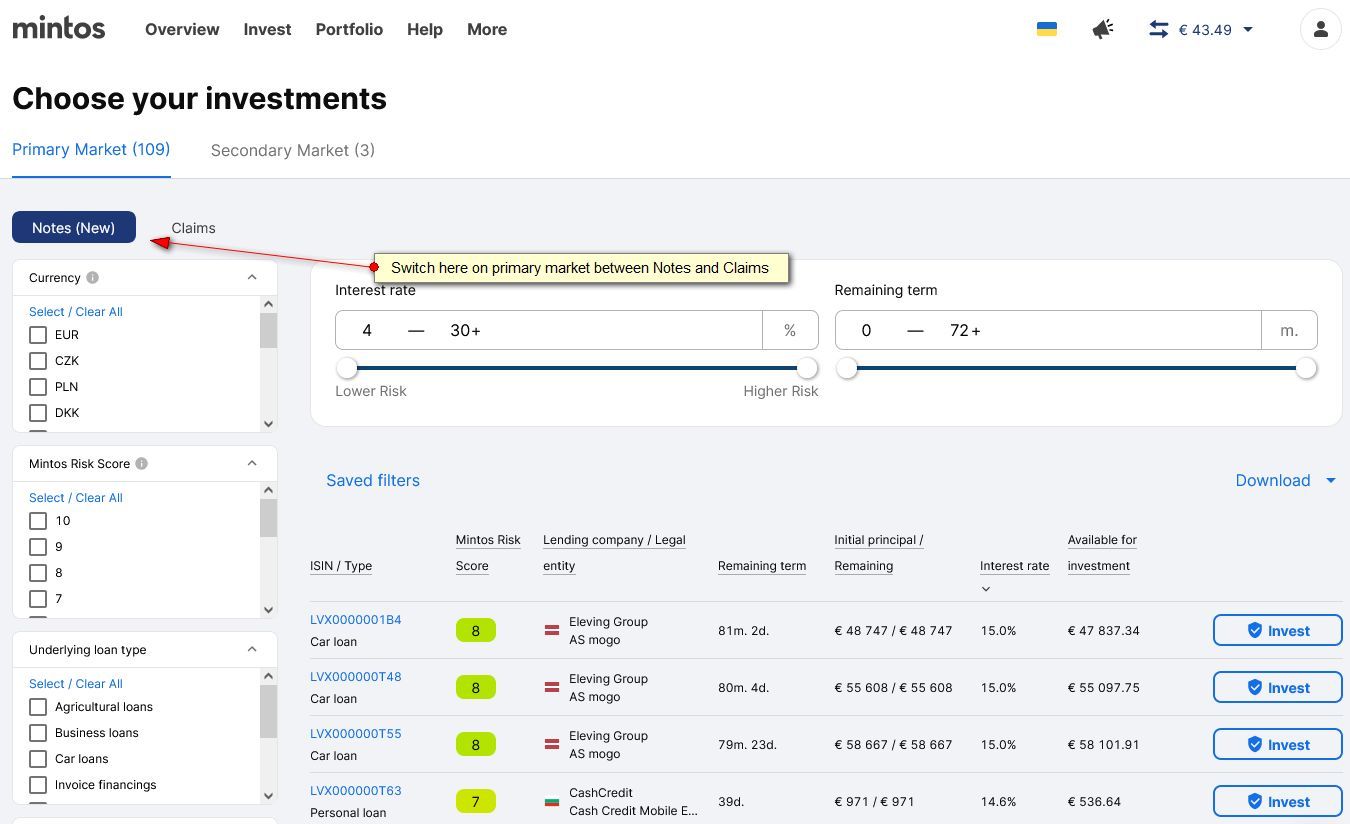

To see the new notes listed on the Mintos primary market, investors can toggle a switch on the upper left side

Screenshot May 25th, 2022, click for larger view

Initially there are notes from the loan originators Eleving Group, CashCredit and Sun Finance listed. Notes for more loan originators will be added as soon as they have published the required prospectus.

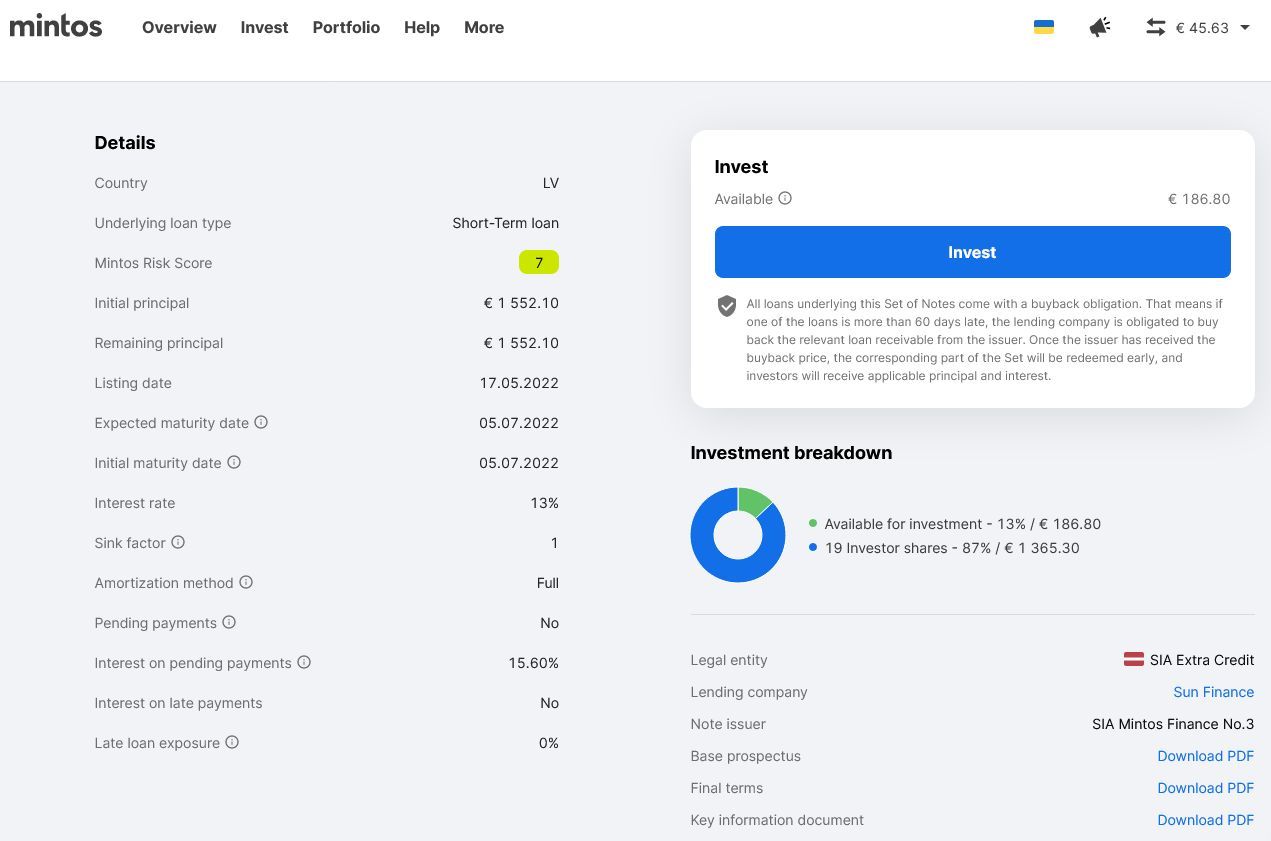

Clicking on an ISIN brings up the detailed information about the loan set. Most of the offered information mirrors that available for claims, but there are some new parameters, e.g. ‘sink factor’

Screenshot May 25th, 2022, click for larger view

Investors have voiced questions and concerns around the shift from the claims to the notes product. Mintos has adressed common questions in this Q&A. One of the most discussed aspects is that Mintos is required to withhold 20% taxes. This amount can be lowered for residents of these countries as soon as they submit a tax residency certifacte from their tax authority to Mintos.

Despite all communication efforts by Mintos it seems an uphill battle. On the German forum in a recent survey 55% of respondents answered that they will stop investing at Mintos as a result of the introduction of the new notes. Another 24% are unsure about it. Similar sentiments can be read on the Czech forum.

If investors will suit the action to the word this might impact Mintos origination volumes in the coming months. Some investors might switch to competing platforms with similar offers, e.g.

Lendermarket* (Creditstar loans, up to 15% interest rate, 1% Cashback when registering through this link)

It will also be interesting to see if there is an impact on the discounts on the secondary market for claims, as investors might try to sell claims before the secondary market sunset for claims on June 30th. If investors do not wish to hold claims to maturity there might be increasing supply outweighting demand and therefore offered YTMs might rise until June 30th.

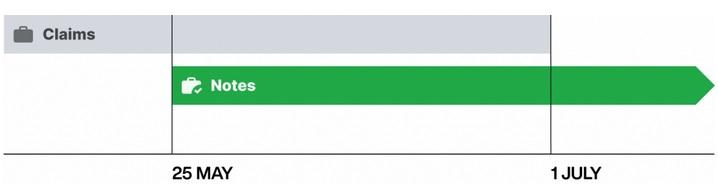

The long announced and several times postponed Mintos Notes product will finally launch on May 25th, Mintos* said yesterday. The notes are financial instruments and issued under the new investment firm license Mintos received last year. For each loan originator there will be a seperate prospectus (see example). Mintos mentions safeguarding of investor funds and notes under MIFID II requirements and increased transparency as investor benefits.

Until 30 June, investors can buy and sell investments via claims on the Secondary Market as usual. Then, from 1 July onwards, investors will be able to buy and sell Notes only, as a result of regulatory requirements.

The transition will mean two key changes for investors:

As the claims cannot be traded from July 1st onwards on the secondary market, investors will have to hold any claims in their portfolio to maturity

Mintos is required to deduct withholding tax depending on the investors country of tax residency and applicable double taxation treaties

My take

The transition will mean a major change for the marketplace that could either stiffle or empower Mintos growth. I expect that many investors will shy away from investing in very long term claims on the primary market in the remaining 7 weeks. Also buyer demand on the secondary market will likely decrease for the claims on long term loans. Potentially this will lead to offers with rising discounts before the trading of claims ends on June 30th.

There is some hesitation voiced among investors regarding the upcoming notes due to the withholding tax and surronding paperwork to claim possible reliefs and reductions (Mintos has announced that it will publish more information on the details). Mintos might try to offer some incentives in order for investors to take the leap and embrace the new product. I also imagine that Mintos will step up investor marketing again, once the notes product has launched. Already Mintos is taking a lot of effort to communicate and explain the coming changes via blog articles and newsletters.

This disruption might also increase the trend of loan originators setting up their own, unregulated investor marketplaces in other jurisdictions than Latvia.

Breaking news: p2p lending platform Mintos* will run an equity crowd on british equity crowdfunding platform Crowdcube. Mintos states ‘As far as startups go, Mintos has raised very little capital so far. We have grown to become the market leader in continental Europe largely fueled by our own revenue. We see a huge market opportunity ahead of us, and to accelerate our growth and develop new products we are raising money. Our fundraising round includes both venture capital and crowdfunding. ‘.

No details regarding the amount to be raised or the valuation have been shared yet. The pitch is set to go live in late November