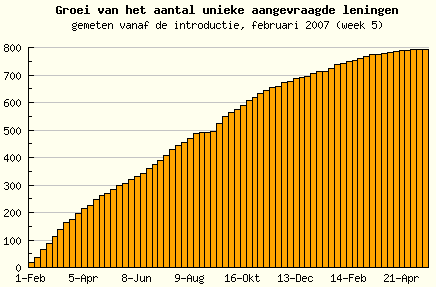

Demand at Boober.nl is slowing. When I checked today only two loan listings were open. The following curve showing unique loan requests definitly shapes in the wrong direction. Boober lenders discus this development in this forum thread.

Since the launch 15 months ago, about 2.4 million Euro (about 3.8M US$) loan volume has been funded through Boober.

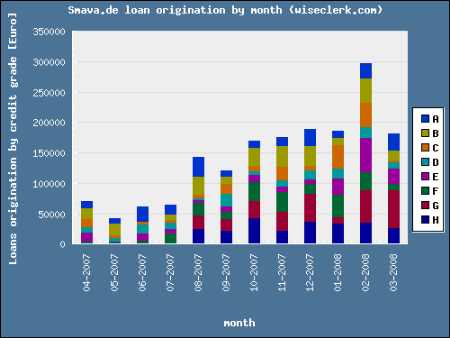

German Smava.de has funded about the same volume (2.3 million Euro) but after a slower start 14 months ago, lately the volume growth accelerated moderately.

German p2p lending service Smava.de made some changes:

Borrowing for business purposes is now allowed. The borrower still is an individual person but is no longer limited on private purposes of the loan

Borrowers may borrow up to 25,000 Euro (approx 39,200 US$), previously the maximum was 10,000 Euro

Maximum amount any lender can invest in the marketplace is raised to 100,000 Euro (previously 25,000 Euro)

Loan terms are now selectable 36 or 60 months (previously only 36 months); the insurance pools (Anleger-Pools) are seperated by credit grade and term. This complicated construct will influence lenders when deciding to bid on loans that are otherwise comparable but differ in loan term, since the level reached in the insurance pools directly impacts each payment rate.

Bad debt sales rates have been lowered for lower credit grades (previously it was 22.5% to 25%, now it is 15% to 25% depending on credit grade)

Since it's launch in February 2007 Smava has funded 457 loans with 2 million Euro (approx 3.14 million US$) loan volume. 8 loans have defaulted and currently 9 loans are late.

German p2p lending service Smava.de launched one year ago. Since the launch of Smava 393 loans were funded for a total loan volume of about 1.7 million Euro (approx. 2.6 million US$).

Lender’s viewpoint

In a february survey 33% of lenders answered to be very satisfied with Smava and 63% were satisfied. 48% said their ROI met expectations while 19% said it exceeded expectations.

So far a 7% ROI is realistic. Only 3 loans have defaulted and 11 are (less then 30 days) late. In the past Smava cured the majority of late loans. The Anleger-Poolmechanism spreads the losses of a default across all loans of a credit grade. Therefore when 1 in 100 loans in credit grade X defaults, the lenders invested in the defaulted loan still receive 99% of the principal, while for lenders in the current loans returns are lowered by 1%.

Technically and on the process level Smava functions as promised.

Borrower’s viewpoint

Provided the borrower has a credit grade of at least ‘H’ (95% of the German population have credit grades between ‘A’ and ‘H’ so about 5% are excluded) and he has a sufficient income, chances for obtaining a loan through Smava are good. About two third of the listings were funded. The fee of 1% of the loan amount that Smava charges borrowers is low.

Marketplace development

Smava’s growth has picked up in the last month (see chart).

So far Smava has not reached a broad appeal. While press release state 25,000 registered users, only 650 have invested money and roughly 450 wrote a loan listing. Looking at the distribution of lenders by amount invested, the top 50 Smava lenders funded about 700,000 Euro (or about 40% of total loan volume). Currently lenders are limited to a maximum of 25,000 Euro investment.

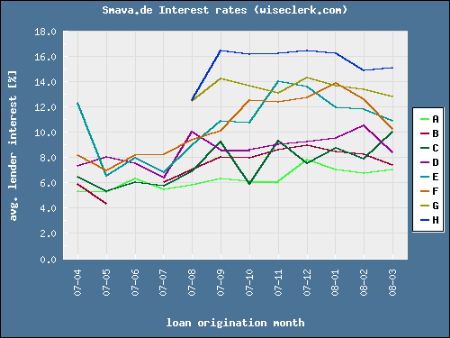

Attracting new borrowers has been the bottleneck for Smava’s growth so far. An increase of money supply by lenders with no matching demacnd increase led to slightly falling average interest rates in the last weeks (see chart). Before rates increased, especially for credit grade ‘F’ caused by sharpened risk awareness following several late payments.

Smava charges borrowers a fee of 1% of the loan amount. There are no fees for lenders. Total revenue of Smava in the first year therefore was 17,000 Euro (1% von 1.7 million Euro). Prosper, Lendingclub and Zopa have much bigger p2p lending volumes per year. Boober‘s loan volume in the Netherlands is about the same size as Smava’s but in a market with only one fifth the size (by inhabitants). First priority of Smava must be to accelerate growth.

German p2p lending service Smava.de yesterday introduced an optional insurance for borrowers. Borrowers can take out an insurance together with their loan. In the case of death, disability or unemployment (through no fault of one's own), the insurance will pay the repayments. To offer the residual debt insurance (see a definition of residual debt insurance), Smava partnered with an insurance company. The costs for the insurance paid by the borrower are:

death hazard only: approx. 0.5% of loan amount

death and disability: approx. 2.5% of loan amount

all three: approx 4.7% of loan amount

It will be interesting to see how many borrowers are willing to opt in to the insurance.

Lenders profit because this lowers the default risk. Unfortunately at the moment lenders can not on a borrower's loan listing whether the borrower selected insurance or not. 11 months after launch defaults at Smava are still rare. Only 3 of 368 loans have defaulted and only 2 are currently late. A chart shows the development of the Smava interest rates since start.

As P2P-Kredite.com reports the first 2 loans at German p2p lending service Smava.de have defaulted. Since the Start in March 2007 a loan volume of 1 million Euro (approx. 1.4 million US$) has been funded at Smava. The amounts of the two defaulted loans are 4,000 and 6,000 Euro resulting in a default rate of about 1%. At Smava loans default 40 days after they are late and are sold in a debt sale for a fixed rate of 25% (22% on lowest credit grades) to a collection agency. 2007 has been a very good year for Smava lenders as defaults (and late payments) have been significantly below expected rates.

Reuters has a video on German p2p lending site Smava.de. This is the first video I saw that's in english language. Features Alexander Artope, co-founder and CEO of Smava.