P2P lending service Bondora* has announced that in future it will focus completely on its hands-off investing product Go&Grow. From February 27th, the products called Portfolio Pro and Portfolio Manager will be discontinued. These allowed investors to select into which individual loans they wanted to invest. Bondora originally started and grew big with investment into individual loans and only 2018 introduced the simplified Go&Grow product which soon became very popular (read my coverage on the start of the Go&Grow product written 5 years ago). Over the years Go&Grow became more and more important for Bondora as investors seemed to prefer the easy to understand product with a fixed interest rate. Bondora’s marketing was focused on this type of investing and also Bondora made it harder to invest into the Portfolio Pro and Portfolio Manager products in the last years by allocating less available loan amounts for investment to these products. In the last years it was no longer possible to invest relevant amounts via Portfolio Pro as allocated investment pieces were only 1 Euro into each loan.

Therefore it comes as no surprise that today’s announcement by Bondora states that currently 96% of all investments are made via Go&Grow. Bondora points out that Go Grow is very easy to use ‘As portfolio diversification is automated, you can just add money, automatically earn returns, and continue living your life. ‘. The Go&Grow product offers up to 6.75% interest (limited for existing customers) or in the Go&Grow unlimited version 4% interest (unlimited, new and existing customers).

The secondary market will continue to operate beyond Feb. 27th. It will still be possible to sell and buy individual loans just not to invest into new individual loans.

Bondora* is one of the longest operating p2p lending services in Europe. The platform has more than 215,000 investors according to the website. Investments are into the underlying consumer loans, which Bondora originates via its website to borrowers in Estonia, Finland, Sweden and the Netherlands. There are few comparable p2p lending services that offer one fixed rate to investors without any configuration/selection possibilities.

Estonian p2p lending marketplace Bondora* announced today that for new customers the availiable Go&Grow interest rate is 4%. They can invest an unlimited amount in the product called Go&Grow unlimited. The Go&Grow tier with an interest rate at 6.75% will remain available only to existing customers that joined before August 24th, 2022. Currently that tier is limited to adding 400 EUR new investment per customer per month.

Bondora says this change is necessary, since they will prioritize launching new loan markets, new financial products, and newtarget audiences in the coming months.

According to the announcement Bondora has 200000 customers, which invested more than 650 million EUR.

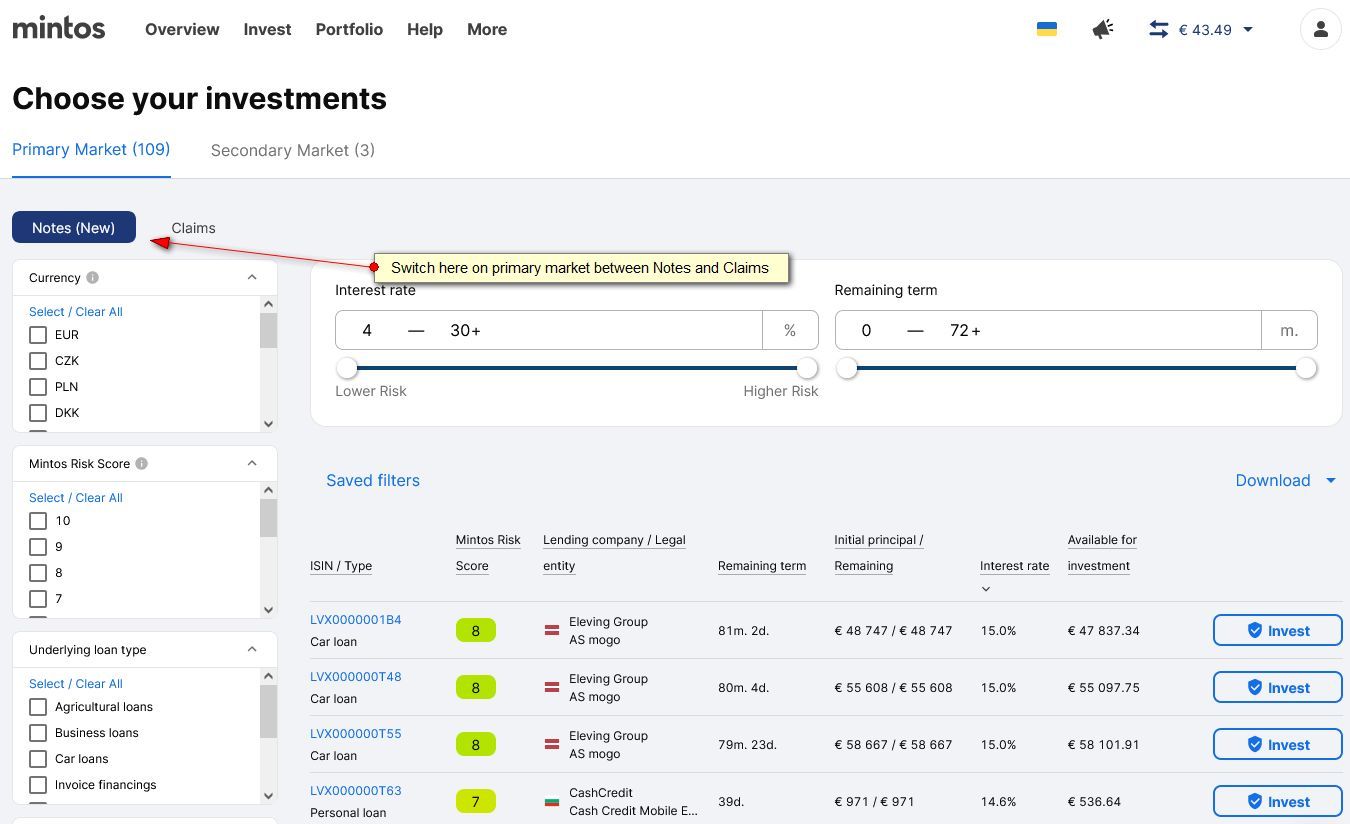

To see the new notes listed on the Mintos primary market, investors can toggle a switch on the upper left side

Screenshot May 25th, 2022, click for larger view

Initially there are notes from the loan originators Eleving Group, CashCredit and Sun Finance listed. Notes for more loan originators will be added as soon as they have published the required prospectus.

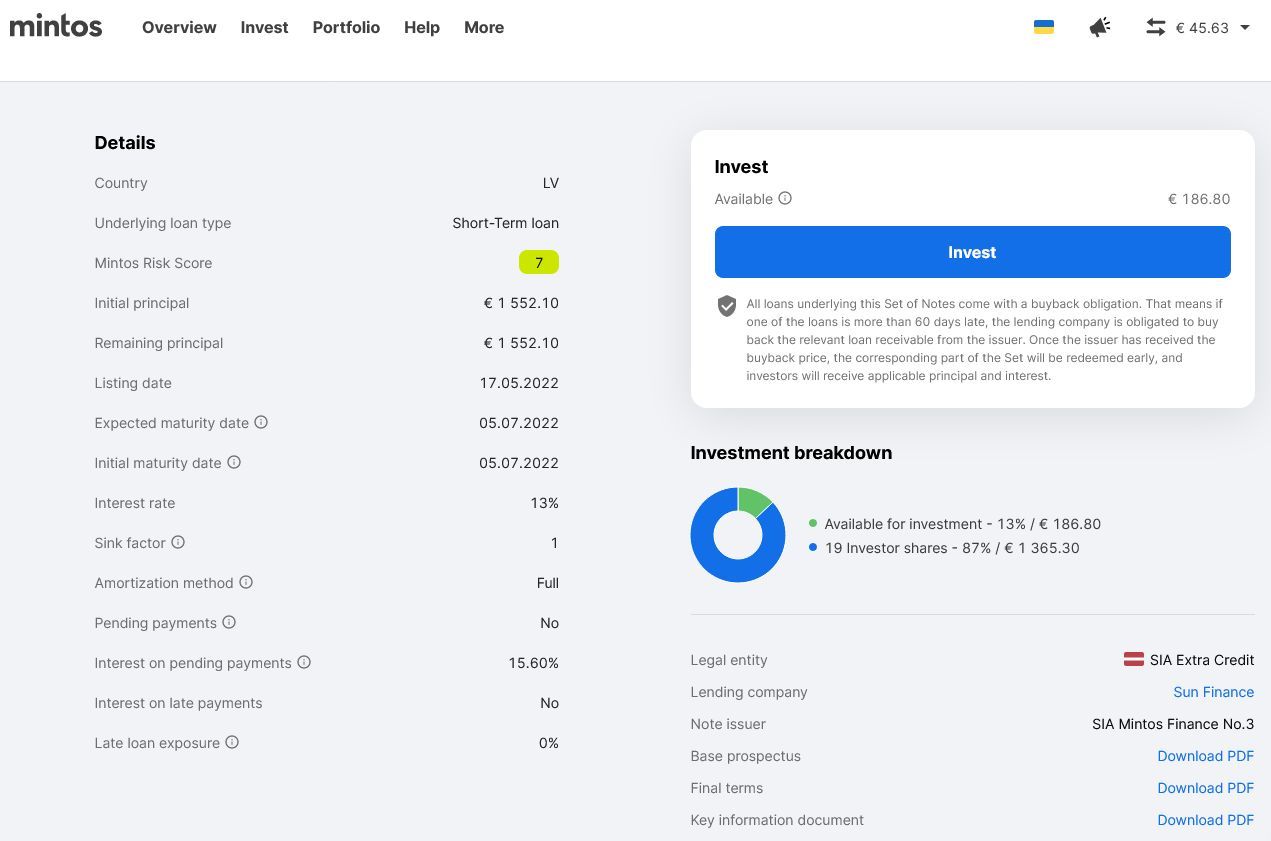

Clicking on an ISIN brings up the detailed information about the loan set. Most of the offered information mirrors that available for claims, but there are some new parameters, e.g. ‘sink factor’

Screenshot May 25th, 2022, click for larger view

Investors have voiced questions and concerns around the shift from the claims to the notes product. Mintos has adressed common questions in this Q&A. One of the most discussed aspects is that Mintos is required to withhold 20% taxes. This amount can be lowered for residents of these countries as soon as they submit a tax residency certifacte from their tax authority to Mintos.

Despite all communication efforts by Mintos it seems an uphill battle. On the German forum in a recent survey 55% of respondents answered that they will stop investing at Mintos as a result of the introduction of the new notes. Another 24% are unsure about it. Similar sentiments can be read on the Czech forum.

If investors will suit the action to the word this might impact Mintos origination volumes in the coming months. Some investors might switch to competing platforms with similar offers, e.g.

Lendermarket* (Creditstar loans, up to 15% interest rate, 1% Cashback when registering through this link)

It will also be interesting to see if there is an impact on the discounts on the secondary market for claims, as investors might try to sell claims before the secondary market sunset for claims on June 30th. If investors do not wish to hold claims to maturity there might be increasing supply outweighting demand and therefore offered YTMs might rise until June 30th.

The long announced and several times postponed Mintos Notes product will finally launch on May 25th, Mintos* said yesterday. The notes are financial instruments and issued under the new investment firm license Mintos received last year. For each loan originator there will be a seperate prospectus (see example). Mintos mentions safeguarding of investor funds and notes under MIFID II requirements and increased transparency as investor benefits.

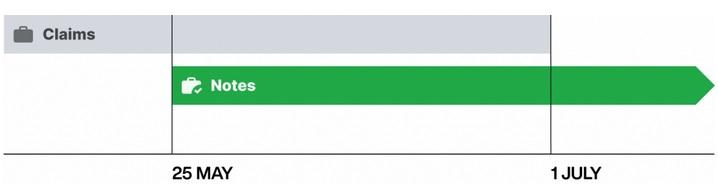

Until 30 June, investors can buy and sell investments via claims on the Secondary Market as usual. Then, from 1 July onwards, investors will be able to buy and sell Notes only, as a result of regulatory requirements.

The transition will mean two key changes for investors:

As the claims cannot be traded from July 1st onwards on the secondary market, investors will have to hold any claims in their portfolio to maturity

Mintos is required to deduct withholding tax depending on the investors country of tax residency and applicable double taxation treaties

My take

The transition will mean a major change for the marketplace that could either stiffle or empower Mintos growth. I expect that many investors will shy away from investing in very long term claims on the primary market in the remaining 7 weeks. Also buyer demand on the secondary market will likely decrease for the claims on long term loans. Potentially this will lead to offers with rising discounts before the trading of claims ends on June 30th.

There is some hesitation voiced among investors regarding the upcoming notes due to the withholding tax and surronding paperwork to claim possible reliefs and reductions (Mintos has announced that it will publish more information on the details). Mintos might try to offer some incentives in order for investors to take the leap and embrace the new product. I also imagine that Mintos will step up investor marketing again, once the notes product has launched. Already Mintos is taking a lot of effort to communicate and explain the coming changes via blog articles and newsletters.

This disruption might also increase the trend of loan originators setting up their own, unregulated investor marketplaces in other jurisdictions than Latvia.

Mintos* will launch a new product offer called Invest & Access tomorrow. It was already unveiled and presented at the P2P Conference in Riga on Friday. Before I write about it watch the video below for about 10 minutes with Mintos CEO Martins Sulte explaining Mintos Invest and Access.

the video should autostart at the right point. If not it is at 2:29:22

The new offer makes it super-easy for investors to invest and automatically diversify through a very wide selection of loans. Mintos does that by investing the money in all loans on the platform that carry a buyback guarantee and are from originators that are at least 6 months on the platform. Mintos promises that investors will be able to cash out easily (subject to market demand) instantly, saying investors don’t need to bother about handling the loan selling on the seondary market. Mintos does that by selling the non-late loans to other investors.

The investor can still see how the portfolio he holds is composed on an overview page. One important aspect for the market dynamics on Mintos marketplace is that Invest & Access will invest before the autoinvests.

Mintos is cleary aiming to make it easy for new investors that don’t want to spend much time thinking about the investment and optmizing yields by giving them the average yield by just one click. The Invest & Acesss page will show the weighted average interest rate, which at the time I saw that page was showed as 11.98%. But the figure will change and update as market conditions fluctate and as the FAQ says it is not guaranteed.

One important point in the FAQ/footnotes is that the ‘instant access’ only applies to current loans. That means if the investors has e.g. 15% late loans, that would mean that he gets only 85% as instant withdrawal and for the remaining 15% has to wait until either the loan is bought back by the buyback or becomes current again (I suppose in that case the investor could trigger another cashout).

Investors can runs both Mintos Invest & Access as well as the existing autoinvests, should they which, but in that case Invest & Access would use any available cash the investor has first, therefore I would guess that there are rarely any funds left for the autoinvests to use.

My Opinion on Mintos Invest and Access

Mintos clearly offers a product that makes it as easy as possible, lowering the entry hurdles especially for new investors. And as Bondora Go&Grow* shows there is a high demand by investors for simplified products. Statistics published by Bondora show that in April 2019 63% of the new investments in that month where conducted via the Go&Grow product, which is constantly gaining over the other investment methods Bondora offers. Other examples are the Access products offered by British Assetz Capital*.

Looking at it from the perspective of an investor that is a little more experienced and willing to spend a little time Invest & Access does not seem an attractive offer. By definition it offers the weighted average interest rate.

By setting up own autoinvests at Mintos, keeping a good diversification and foregoing the highest risk, investors can currently achieve about 13-14% yield on Mintos. So if they would instead use the new product they would have about 2-3% lower yield, and have actually less control on which originators they invest in. An important point to consider, is that the value Mintos shows you, is the average interest rate, NOT the expected average yield. The yield will be significantly lower than the interest rate as Mintos will include buyback loans from originators with long grace periods or originators that do not pay interest income on delayed payment. Excatly those are typically avoided when investors configure their own autoinvests.

And concerning the argument of liquidity. Mintos is very liquid anyway. Without using the new product it is no problem to liquidate a portfolio within a few minutes to a few hours it just depends on the price. Sure you might have to offer a discount. Maybe depending 0.2%-0.6% on average. But that is a small price if you had the higher yields before.

So would I recommend using Invest & Access over the ‘traditional’ way of setting up own autoinvest? There is one use-case I would. If an investor wants to invest very short-time (for whatever reason ‘parking’ money) for less than say 120 days, than it is worth considering.

In my opinion on why Mintos launched the new product, there are actually two reasons:

there is demand for a simplified product and this new product shall satisfy that

the new product will help on the sales site for attracting and onboarding new orignators. Originators that can only offer rates that are below the average interest rate on the Mintos platform so far were hard to sell. With Invest & Access they will be just part of the bundle and automatically sold (once the originator has been on the platform 6 month)

That brings us to an interesting point. How will Mintos Invest & Access the market dynamics? The big factor here is that Mintos Invest & Access happens BEFORE autoinvest and manual investment. There are already (even before launch) speculations and fears of investors that it might bring down interest rates or ‘force’ them to use the new product to avoid cash drag, but I think it is much to early to make any prediction what might be the outcome. But I sure am curious what this will do to the activity on the Mintos marketplace.

What are your opinions on the new product? Please share them in the comments. Thx.

P.S.: The following interview with the Mintos CEO was recorded just before the announcement of the new product, therefore it does not cover Invest and Access – but it has a lot of information on the current state of Mintos.

Everybody talks about the win-win situation p2p lending offers for lenders and borrowers. By cutting out the large spread a bank takes when making a loan, the lender can get a higher interest rate, than he might in a savings account and the borrower may get a lower interest rate, than using his credit card. But who does actually decide what the interest rate for a p2p loan will be?

Several market mechanisms have developed. P2P lending services use combinations of these to built their platforms. I’ll describe some of the elements:

Individual Loan Listings vs Markets: With Listings (e.g. Prosper, Lending Club, Auxmoney, Isepankur) lenders can look at individual loan listings and see multiple parameters (e.g. credit grade, income, DTI, occupation, location,…). The lender can select (“filter”) loans based on his strategy. This is not necessarily a manual process as he can opt to use automatic bidding tools that make the selection for him based on criteria he set in advance. Other p2p lending services use Markets (e.g. Zopa, Ratesetter) which combine loans based on broader criteria (e.g. loan term, or credit grade). Here a lender can only decide which market to invest into, but does not pick individual loans.

Close at Funding vs Auctions: Some p2p lending services close loan listings once they are 100% funded. The loan is then originated. Others uses an auction process where the listing is open for bidding for a set time. If the loan amount is 100% funded then the bidding continues for the remaining auction period. New bids at lower interest rates push out old bids at higher interest rates, thereby lowering the final interest rate for the borrower. Some p2p lending services allow loan listings of both types or let the borrower prematurely end an auction (e.g. Rebuildingsociety, Isepankur, Assetz Capital).

Uniform vs Mixed Lender Rates: After an auction the interest rate for the borrower can be set at the rate of the highest successful bid. In this case all lenders on the same loan get the same uniform interest rate (e.g. Isepankur). Another option is to calculate the interest rate as an aggregate of all successful auction bids. In this case each lender gets the rate he did bid – there will be a wide mix of lender interest rates on the same loan (e.g. Rebuildingsociety).

Who does decide what the interest rate will be on a p2p loan

I. Borrower sets interest rate

The borrower decides, what (maximum) interest rate he is willing to pay (e.g. Smava, Auxmoney, Isepankur). The lenders can then decide, if they want to fund this specific loan at that rate or not. If there is an auction and lender demand is strong, then the borrower may get the loan for a lower interest rate then specified. Obviously lenders will fund loans with most attractive rates first and other loans will go unfunded. These borrowers can react by relisting at a higher interest rate. Continue reading →