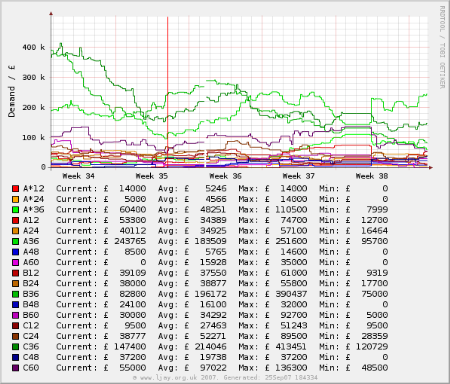

Zopa UK has announced that it will remove the options to lend for 12, 24 or 48 months and concentrate on lending terms of 36 and 60 months. The changes apply only to money lend through Zopa markets not to Zopa listings.

Why are we making these changes?

– Since Zopa began more than three years ago, more than 95% of your loans have been taken for a period of 3 years or less.

– The popularity of larger loans repaid over 5 years is increasing, particularly since we introduced the new fixed borrower fee.

– Almost half of our new lenders who sign up to Zopa do not become active and our hypothesis is that it is just too time consuming for them to make offers to all of our markets.

– This allows us to simplify the marketplace considerably, while still allowing borrowers to repay their loan early with no penalty.

– Because listings still enables all loan terms from 1 to 5 years, Zopa will continue to offer a wide variety of borrowing and lending options.

– By structuring repayments over at least 36 months, we aim to encourage fewer borrowers to repay their loan early, maximising the interest you earn from each loan and reducing the period your money might spend in your holding account. This is because the loans that have been repaid early to date were mostly taken for 12 and 24 months in the first instance, so that borrowers had paid back a good proportion of their loan after just a few months.

– We’re not envisaging that there will be any significant financial impact for Zopa from these changes. At most, we would earn 0.5% of the outstanding capital for a little longer if we can dissuade early repayment, but since we would hope that lenders would relend any funds repaid early anyway, we’re unlikely to earn anything more significant. These changes are purely aimed at simplifying our offer.

Lender reactions in the forums (19 pages of comments) are mostly negative.

Some lenders speculate that this move is a necessary result of the new flat fee which was introduced earlier. Borrowers pay 94.25 GBP of the loan amount. For short term loans the impact of this fee on the APR is higher then for long term loans.