Startup Heavyfinance* has launched a platform for lor loans backed by heavy machinery, the first of this kind in the p2p environment as far as we know. The loans are backed by machinery in Lithuania (currently, the company plans to add Latvia, Portugal, Spain and Bulgaria and other EU countries), but the platform is open to investors internationally.

CEO and co-founder Laimonas Noreika told P2P-Banking: “First of all, every farmer, lumberjack and construction company has some heavy-duty vehicles that usually are not taken into account when traditional financial institutions evaluate their risk level. Consequently, those small and medium businesses cannot get loans, even though they have many assets to use as collateral in case of a default. Furthermore, prices of heavy equipment are extremely stable due to the nature of this highly international market. Used combine harvesters, tractors, excavators and other heavy-duty vehicles can easily be exported to foreign countries and transportation costs are relatively low compared to the size of the transaction. ”

Lainmonas has a lot of experience in the p2p environment as he co-founded Finbee* in 2015, a Lithuanian platform for consumer and business loans.

machinery is insured and serves as security for the loans

Investors can choose to invest in loans depending on the risk they are willing to take. Risk levels are indicated by letters A (lower risk), B (medium risk) and C (higher risk). Consequently, while you could earn up to 14% interest rate by investing in C risk level loan, A risk level loan would bring you around 10-12% interest rate depending on the amount you’ll invest.

Talking about the risk assessment in more detail, these are the main criterias the platform looks at:

Financial statement for past 2 years;

Balance sheet;

Cash flow statement;

Reputation of business owner;

Loan-to-value ratio

Regarding the COVID-19 pandemic situation Laimonas stated: “It is safe to say that the agricultural sector was one of the least negatively affected. One of the challenges we noted was a limited supply of heavy-duty vehicles and farm equipment parts due to the shutdown of some production facilities and the disruption of supply chains. …”

HeavyFinance is supervised by The Central Bank of Lithuania under the track of crowdfunding platform operators.

Bondora has been rolling out a new product called Bondora Go & Grow to select users since March. It will be officially launched in June, but existing users can contact support and ask for the product to be made selectable in their accounts.

Go & Grow is designed for the passive investors as hands off p2p lending. One of the main advantages is that Bondora says it is tax optimised.

The Bondora Go & Grow product features a target interest rate of 6.75% which will accrue daily. It runs completly on autoinvest. The investor just needs to join it and pay money into the Go & Grow account (or transfer it from the normal Bondora account). The Go & Grow account promises daily liquidity. There is a 1 EUR withdrawal fee making small withdrawals expensive but for portfolios of 1000 EUR or more and usual investment horizons this fee is negligible.

How does Bondora Go & Grow work?

Simplified it is an autoinvest tool where Bondora invests the deposited money in loans on the Bondora marketplace (the investor does not see the individual loans). The investor automatically sells any claims for repayments and interests from these loans to Bondora which in return agrees to pay the 6.75% interest to the investor. Note that the 6.75% are not guaranteed but Bondora is very confident (based on their over 10 years experience) that they can achieve this yield. So basically Bondora invests the money on the market’s interest rates which are higher than 6.75 and the results influenced by defaults, late payments and cash drag, but Bondora is confident they are higher than 6.75%. Bondora pays the 6.75% to the investor and uses the surplus as reserve, which will be kept separate from Bondora’s funds.

What does tax optimized mean?

Bondora mentions two advantages:

The product is net of any defaults. This can be advantageous for investors in countries where it is not possible to offset default losses againts interest earned for tax purposes.

Interest accrues and is only credited at (final) withdrawal. This delays the point in time where interest is taxable according to Bondora.

So is this better than the ‘traditional’ Bondora product?

In my opinion this product is only the better choice, if the investor really does not want to be bothered with making minimal choices the Portfolio Pro requires and some monitoring. As described Bondora invests the money in the very same loans that are available in the traditional product and expects a higher yield than 6.75%.

For that very same reason I would caution investors to carefully consider, if they do want to take up the offered option to sell out their existing ‘traditional’ portfolio when opening/funding a Bondora Go & Grow account. I assume that investors are very likely better off keeping that portfolio than selling it to Bondora at the price Bondora offers. However for an investor that really wants to sell an exitsing portfolio completly this offers a way to cash out (edit: see reader comment below) as the cash is than in the Bondora Go & Grow account and can be withdrawn instantly.

One caveat of course is that according to the T&C the liquidity for Bondora Go & Grow is subject to market conditions and not guaranteed. It reads a bit like the ‘normal market conditions’ wording that Assetz Capital uses for its Quick Access Account.

Flender, which recently soft launched a p2p lending marketplace in Ireland, received full FCA authorisation last week, saying it took two years of consultation with the FCA and the legal team to achieve approval. This will be needed for the launch in UK, planned for later this year.

Limited time offer: Cashback: 10% cashback on any investment over 1,000 GBP for P2P-Banking reader. Sign up to use. (Update Aug. 2017: the cashback offer has been extended to August 31st, the minimum investment requirement is now 2,500 EUR)

Flender offers both SME and consumer loans on the marketplace. The main points for investors are:

no fees for investors

50 Euro minimum bid

open to international investors (prerequisite is a bank account in the European Union)

interest rates of the currently listed loans range from 8.1% to 10.4%

reverse auction bidding (though at the moment, loan supply outstrips lender demand, therefore I don’t expect any underbidding soon). currently no autoinvest

Flender charges origination fees for business loans from the borrower. While there are no origination fees for borrowers for consumer loans, Flender does have a margin income on those (same with business loans).

Once the UK operation launches, investments can be made cross-border. An interesting aspect is that the borrower will take the FX charges.

Flender does have big plans. On the list are an IFISA offer, several features for investors and borrowers to customize the experience and mid term a secondary market. Flender currently has a team of 7 employees.

I published an interview with the CEO of Flender in the end of 2016, when they raised 500K GBP through equity crowdfunding on Seedrs. Flender will likely be back on Seedrs to raise another round later this year.

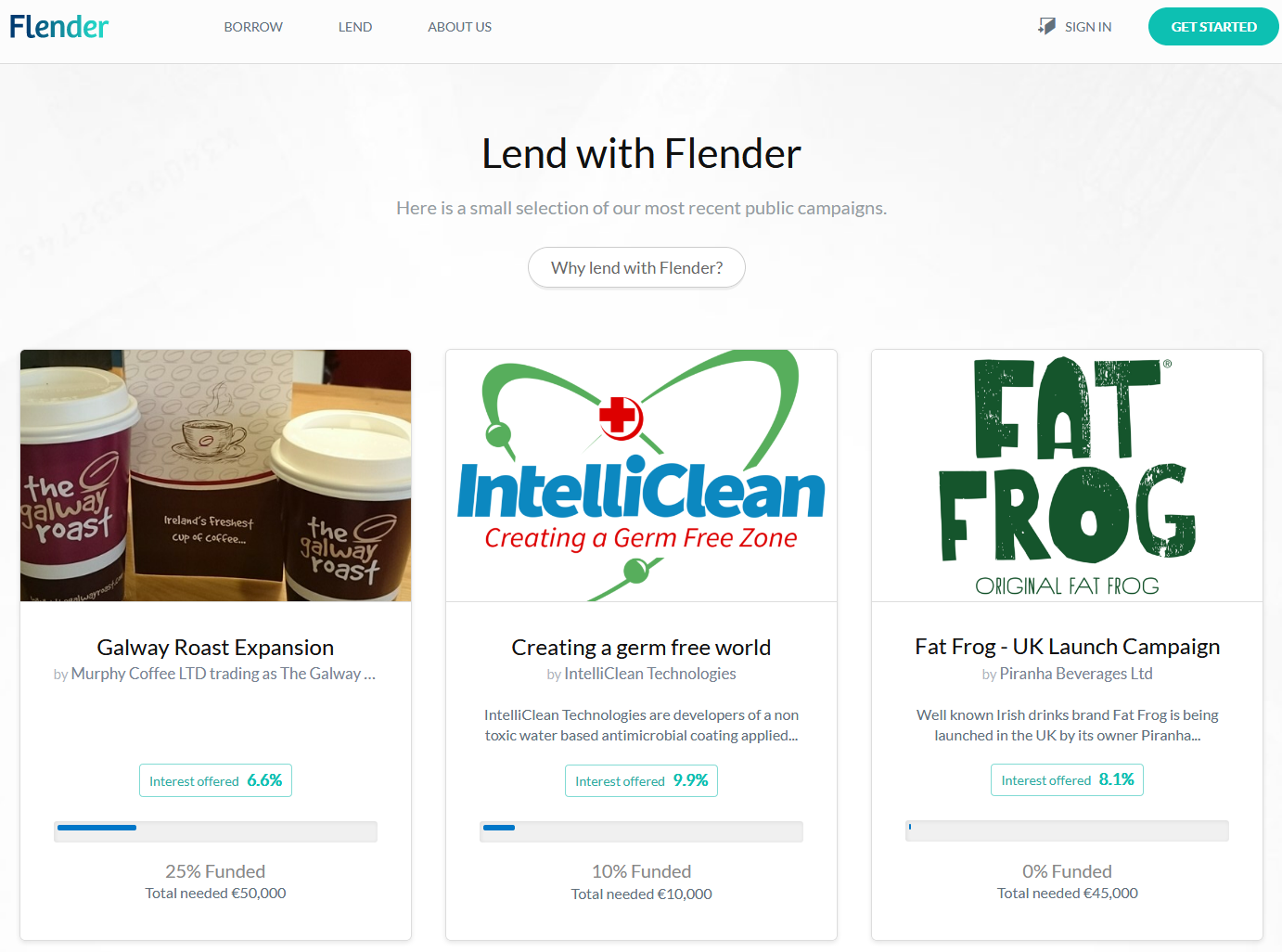

As my experiences with another Irish p2p lending marketplace are good so far (it has low default rates), I registered on Flender too. There are currently 4 business loans listed seeking a total amount of about 150K Euro.

Screenshot of Flender marketplace loan listings (excerpt)

mozzeno is a Belgian fintech founded in December 2015. We have just launched the first digital platform to enable private individuals to participate indirectly in the funding of loans to other private individuals. Loans are granted by mozzeno, acting as a regulated lender. mozzeno then finances or refinances these loans thanks to the issuance of Notes (financial instruments).

What are the three main advantages for investors?

Investors can expect higher returns compared to deposits or saving accounts in Belgium (currently close to 0%).

mozzeno performs a strict selection of borrowers and eases the diversification of investor’s portfolios.

Investors can benefit from a ‘PROTECT guarantee’, covering between 60% and 100% of the loan outstanding amount and up to 3 unpaid instalments, in case of default.

Investors can choose between manual or automated (re-)investments, with very granular selection criteria to match their risk appetite and investment preferences.

What are the three main advantages for borrowers?

Borrowers can benefit from competitive market rates, proposed dynamically based on their assessed risk profile. This cost of credit can also be further reduced, thanks to a specific incentive we put in place. Borrowers repaying systematically on time over the loan period are getting a part of the origination fee back on their bank account at the end of the loan term.

Interests paid by the borrowers are benefitting to other people like them, not to banks or other financial institutions. An increasing number of people are sensitive to these sharing economy principles or simply open or looking to financial solutions outside of the traditional banking system.

The loan application process can be completed fully online and digital. Even the loan agreement can be signed digitally thanks to eID. If the borrower chooses the proposed digital options, the whole process can be done without any paper on any side (borrower and mozzeno).

What ROI can investors expect?

Investors are building their portfolio of Notes themselves, picking up underlying loans manually or thanks to automated investment profiles. The selection can be made based on criteria like the loan purpose, the risk class, the maturity, or more advanced criteria like net income, housing status, professional status… Hence, the return an investor can expect really depends on the type of investment strategy he will follow. As an average we target to provide 3% before tax, the maximum expected return is about 5,79%.

Is the technical platform self-developed?

Absolutely, we started the development of the platform internally in November 2015, in parallel of the regulatory track. From the beginning, the ambition has been to develop a highly modular, scalable and multi-lingual platform that can be leveraged for other sharing economy use cases, under our own brand or through white-labelling. mozzeno services, mother company of mozzeno, develops such a B2B business model, and can provide a range of existing modules (eKYC, digital boarding, transaction orchestration, scoring…) to other financial players, as well as co-develop complementary modules with them.

What credit rating / credit history data is available on Belgian consumers and how reliable is it?

There is a very high concern for the risk of over-indebtedness and for retail consumer protection in Belgium compared to other EU countries. There is no developed pay day loan or subprime business, as the interest rates and maturity are capped and the lending activity restricted to regulated lenders. These regulated lenders have the obligation to register all granted loans (mortgages, personal loans, credit cards, credit lines, overdrafts…) to the Central Individual Credit Register managed by the National Bank. This database also includes information on defaults. As a regulated lender, mozzeno is contributing to this CICR and has access to this market-wide credit history database (positive and negative sides).

As a consequence of this market specific, there is no other established credit bureau. With regards to credit rating, we have developed our own scorecard with a specialised company, we continue to further develop it, and we also benefit from the well trained scoring of our credit insurer.

How is the company financed? What background does your team have?

The company has been initially founded and funded by my partner, Xavier Laoureux, and me. Xavier has a master in Law, has worked more than 10 years in digital marketing strategy for agencies like TBWA. I have been working 15 years in the online payment business, namely for Ogone and then for Ingenico ePayments. Tom Olinger, former CFO of a mid-size Belgian bank, has joined the management team in April 2016.

Some fintech business angels and W.IN.G (a Belgian seed fund) have taken part to a seed round in Q2 2016. A further funding round should take place in the course of 2017.

Can you please describe the p2p lending regulation in Belgium?

Well, actually p2p lending as such is forbidden by law in Belgium. On one hand, the European prospectus law has been adapted locally very strictly, preventing individuals to raise funds publicly, even through an intermediary platform. This means that a borrower candidate cannot invite other people publicly to lend him money. On the other hand, one needs to be a regulated lender to grant loans and to get access to the Central Individual Credit Register. There is a new regulation as from November 2015, this regulated lender status now being supervised by FSMA.

Our regulatory model is then two-sided. We were the first Belgian regulated lender approved by the FSMA as per the new regulation, and this allows us to grant loans for Belgian residents. We also published a base prospectus, also approved by the regulator, allowing us to issue Notes on a continuous basis. These Notes are the financial instruments subscribed by the investors, similar to bonds, and mimicking the repayment behaviour of the underlying loan.

mozzeno is the first p2p lending service in Belgium. Compared to other European countries Belgium had to wait long for a p2p lending marketplace. Is regulation the cause for this, or are there other reasons?

The complexity of Belgian regulation is obviously the main reason. This so called banking monopoly made a ‘simple’ direct model for peer2peer lending completely impossible in Belgium and a few previous attempts have failed for that main reason. Our indirect model copes with this complex regulation and the operational model of the platform has been thought to be as close as possible to p2p lending from a user experience perspective.

Having said that, Belgium also remains typically a complex market due to the different languages and cultures as well the limited size.

What is the reaction / the viewpoint of banks, if you talk to them about p2p lending?

We have discussed with the main Belgian banks over the past 2 years, and the initial reaction was scepticism due to the complex regulation and the required regulator green light still ahead of us at that time. Now that we have the required regulatory agreements and that we are live, we are seeing diverse reactions, either enthusiastic or defensive. This is of course too early to draw any conclusion on this. We are, on our side, convinced that both models are complementary, and open to share views and discuss with banks and other lenders. We have applied to the relevant industry associations to foster such exchanges.

What was the greatest challenge so far in the course of launching mozzeno?

Certainly the complexity of Belgian regulation, with regards to p2p lending, and the time needed to define and set-up the required structure, with first discussions with the regulator as from March 2015. While we understand and agree with each of the requirements, questions and challenges we have faced so far, it is fair to say that this is not always compliant with a startup agenda.

Which marketing channels do you use to attract investors and borrowers?

For borrowers, we are planning to use mainly digital channels, with the best mix possible between natural, earned and paid traffic sources. For investors, beside the same digital channels, we plan to organise roadshows and meet investors physically to build trust in the platform. We will respectively orchestrate the marketing effort based on the demand/supply balance.

On both sides we also intend to set-up member-get-member programs.

Is mozzeno open to international investors? Do you plan an international expansion?

As most businesses starting from Belgium, an international expansion is integrated in the plan from day 1, due to the limited size of the domestic market. On the investor side, our main commercial focus at launch is on Belgian retail investors, but we can technically accept retail and professional investors from EU today. Our prospectus can also benefit from an EU passport, for countries in which we will target a real commercial focus on retail investors. On the lending side, regulations are not harmonized at EU level, so our internationalisation strategy will be a mix of partnerships with assets originators and own expansion, based on opportunities.

Where do you see mozzeno in 3 years?

We see mozzeno as becoming a trusted and representative player in Belgium, having a footprint in some other EU markets, either through partnerships or under our own brand. With mozzenoservices, white-labelling our technology has also a great place in our plans (innovative scoring systems, platforms for the sharing economy, seamless digital boarding processes…), with expectations to partner with the most ambitious fintech, insurtech or traditional players, helping them in their launch or digitalisation roadmaps.

Giromatch promises its customers “Better Banking Together”. We are a Direct Lending platform and offer our prime retail borrowers a complete digitized loan process at top rates. For investors we offer in this low yield environment a complete new asset class, namely the Deutschlandportfolio. What previously has only been accessible by banks, is now available to everyone – investing into a diversified prime loan portfolio and achieving an attractive return while keeping risks at a manageable level.

What are the three main advantages for investors?

The first great advantage for investors is that they get access to this new asset class at no costs. Secondly, the investment into the Deutschlandportfolio is automatically diversified. This is being achieved by a matching algorithm that optimizes each investment. The third advantage is the security-pool. Giromatch deposits a certain amount of each earned euro into the security pool in order to build up a security cushion for investors.

What are the three main advantages for borrowers?

The advantages for our borrowers result from the digitized loan application process. The loan application can be finished online in less than 10 minutes, no matter if you access Giromatch from home or mobile. A second advantage is the instant loan term confirmation without registration. After one enters all credit relevant facts, we show a customized rate, which we try to stick to as long as the input data was correct. A registration is not necessary in order to get a customized quote. A third advantage is our technology driven approach during the data verification process. A borrower does not need to send us documents proving the credit history. All we need from the borrower is a temporarily login into his/her current account, such that we can instantly confirm the credibility. Nevertheless, we think the most important advantage are the low rates we offer, which is only possible due to our digitized and cost-saving structure.

What ROI can investors expect?

The ROI depends on the portfolio the investor chooses. We provide two different maturities. The shorter-term Deutschlandportfolio runs for three years and has an estimated gross return of 3.60 % p.a. Investors who choose the portfolio with the investment period of five years can expect a gross return of 4.00 % p.a. Due to our strong credit checks we anticipate no more than approximately 1% losses p.a. post recovery due to expected defaults.

How is your company funded?

We were able to inspire several business angels from the financial industry for our seed funding round. Hence, we were able to not only fund the company but also to win many important contacts in the financial industry. Prior to the seed round we invested our own money and money from friends and family. And we were granted an EXIST scholarship by the Bundesministerium für Wirtschaft und Energie (BMWi).Continue reading →

Kameo is a Scandinavian marketplace for SME loans. It was established to meet two clear challenges in the Scandinavian markets: SMEs do not get loans; investors do not get good returns. By directly connecting them, we hope to make the situation better for both. Kameo’s vision is to include more people in the financial markets.

Note from editor: Kameo will launch around next week.

What are the three main advantages for investors?

Better expected returns

Support SMEs, the most important employer in Scandinavia

Possibility to create diversified portfolios

What are the three main advantages for borrowers?

Access to (more) funding

Quick and easy loan application

Flexible security & collateral structures

What ROI can investors expect?

Loans will be offered at 5 – 15 % per annum. At first, there will be no fees for investing through Kameo. We expect low default rates, based on historical data for Scandinavia and our thorough credit assessment. We can conservatively assume it to be around 1 – 3 % (naturally dependent on risk profile).

What is the background of the Kameo team? As some of you are Norwegian, why did you select the Swedish market for launch rather than Norway?

The team currently consists of five persons, of which only I am Norwegian. We have various backgrounds, but the same optimistic view of the future: alternative finance will transform Scandinavian banking, and it will become better for more people – it is the social democracy model, of which we Scandinavians are so proud.

We have a credit analyst with 20 years of SME analysis experience, a CTO that previously co-founded Avanza and developed its platform (Sweden’s largest net broker) as well as a marketing specialist and a business developer with backgrounds from digital marketing and corporate finance, respectively. My background is also from corporate finance at Norway’s largest bank, DNB.

And because we expect to grow, we will be looking to further strengthen the team next year.

While the largest owners are Norwegians, we chose to start in Sweden because the market is larger, it is a well-developed fintech-hub (#2 in Europe after London), and Kameo’s largest owner has a successful startup history in Sweden. In addition, the regulatory regime was easier when we started working with the idea (but this has since changed). We have, though, a clear ambition to cover Norway and Denmark next year, thus creating a Scandinavian marketplace (investors can create portfolios of Scandinavian loans.)

How is the company financed?

Two rounds of equity investments from co-founders, board members and angel investors. And I have sold my apartment and invested everything (except what I intend to lend through the platform in order to fund my daughter’s driver’s license in 16 years).

We will also be looking to raise more capital sometime next year, when we roll out in Norway and Denmark. Continue reading →