There is news today from Estateguru* a marketplace for property backed loans to SMEs in various European countries.

Estateguru has announced that the Estonian Financial Supervision and Resolution Authority (Finantsinspektsioon) has granted the platform its European European Crowdfunding Service Providers for Business (ECSPR) licence, allowing it to operate as a crowdfunding service provider across all European Union (EU) member states under unified rules.

Estateguru was the first crowdfunding platform to be regulated in several markets, including Lithuania, Finland and the United Kingdom. The granting of the new Pan-European licence serves to confirm that the company is fully compliant with all of the recently introduced regulations and that its internal processes and procedures meet the financial standards necessary to operate anywhere in the EU.

‘The ECSPR licence marks a significant milestone for Estateguru, enabling the platform to expand its services and provide investment opportunities to a wider user base throughout the European Union. The recently introduced ECSPR regulations provide for greater transparency for investors and introduce new obligations to ensure consumer protections and safeguard the interests of investors,’ said Mihkel Stamm, CEO of Estateguru.

Estateguru says it has been proactive in preparing for this regulatory change, having already implemented customer checks, complaint-handling protocols, appropriate marketing messages, and other changes in order to fully comply with the ECSPR regulations. The company had previously championed the creation of the regulations and even contributed to their formation in Estonia.

‘As Estateguru becomes among the first ones on our home markets to receive a licence, the company solidifies its position as a trusted and compliant crowdfunding service provider, both in the region and all of Europe,’ – added Mihkel.

EstateGuru*, the pan-European marketplace for short-term, property-backed loans headquartered in Tallinn, Estonia, today announces the successful closure of its Series A funding round, with investments coming from Switzerland, United Kingdom, Czechia, Austria, Germany and Cyprus.

The lead investor for the round is TMT Investments Plc, a UK VC, and a public company that was also an early investor in both Bolt and Pipedrive. Among other VCs, there are the Swiss VCs Verve Ventures and Swiss Immo Lab, and J&T IB and Capital Markets, the investment banking arm of the Czech investment bank J&T.

The total amount raised is €5,8M (ca $7M). This follows a successful equity fundraising round on the Seedrs* platform in May this year. The round exceeded its initial target by 260%. The campaign’s maximum target was achieved within just four days, instead of the initially planned 40-day-campaign. EstateGuru says it has been thriving thanks to retail investors’ support for the business model since the very beginning of the company, with 41% of new investors coming from referrals and 90% of investors doing so repeatedly. One in two borrowers returns to EstateGuru by taking out six loans in ?ve years’ time on average. This was also the reasoning behind the Seedrs round in May. EstateGuru states it believes in the importance and power of the community and considers it extremely important to give them a chance to participate in the equity raise.

‘We have an ambitious technology and expansion roadmap for the next few years, and the success of this fundraising round will position us perfectly to deliver on this and continue providing all investors and borrowers with the very best real estate financing platform. We are developing a modern ecosystem for market participants and believe that very soon, traditional financiers will also prefer to use our platform in order to stay competitive. The fact that the same investors who have invested in two of Estonia’s leading startups, Pipedrive and Bolt, have now chosen to put their faith in EstateGuru is the perfect affirmation that our business model is robust and that we are ready to seriously accelerate our growth,’ says Marek Pärtel, CEO and Co-Founder of EstateGuru.

‘We are happy to support EstateGuru in the new round. It solves important problems – attracting money to real estate and at the same time making it possible to invest investors’ funds at a profit and at the most modern level. According to various estimates, the p2p lending market will grow by 2025 from $ 350 billion to $ 0.5 trillion. We strongly believe in EstateGuru’s prospects’, – says Artyom Inyutin, Co-founder & Head of Investments, TMT Investments.

‘There is a significant SME financing gap in Europe and a strong investor appetite for high-yield investment products. EstateGuru is in a perfect position to take advantage of these two trends and become a global leader in real-estate backed lending.’ added Jo?o Duarte from Verve Ventures / Swiss Immo Lab.

Baltic property lending platform Estateguru* has just launched a round on Seedrs* to raise up to 2 million EUR in new funding at a pre-money valuation of 28.8M EUR . Estateguru was launched in Estonia 6 years ago and has since expanded into the Latvian, Lithuanian, Finnish, Portugeese and German markets. Using the platform 47,000 investors have funded over 1,400 loans with a volume of 202 million EUR for an average return of 11.8% (as per Estateguru statistics page). All loans are secured by mortgages. Estateguru says that so far all recoveries of defaults have returned 100% of the capital and just the length of discovery varied sometimes taking months, sometimes taking years.

Estateguru plans to use the raised capital to further develop the product, especially improving features for institutional investors. Estateguru* can build on the experiences it made in a two-year relationship with German Varengold bank which has provided a credit line to finance loans. A second goal is to expand into further markets. In a recent investor webinar CEO Marek Pärtel named UK as a potential market, stating Estateguru already holds the required licenses since last year. Furthermore Estateguru will implement integration with payment provider Lemonway.

Pärtel said in the webinar that Estateguru has doubled in size every year in the past and expects the fast growth to continue in the future.

European p2p lending services are growing. And yields of 10+% are achievable on some of the platforms. This attracts international investors. But if you are a US resident, you may have made the experience that you cannot register on some marketplaces. This is mainly due to KYC (know-your-customer) and AML (anti-money-laundering) requirements, which get more complicated if the client is outside Europe.

I have asked many of the European p2p lending marketplaces, whether they accecpt US residents and US companies as investors.

Here is an overview of 5 services (sorted aplphabetically) that do allow US investors. I have not provided a review for each of the service as the article would have gotten too long, but you can easily find news and reviews by entering the company name into the search box on the upper right of this blog.

On some platforms you need a bank account in the European Union. In most cases Transferwise* borderless or Revolut* will help (while technically e-money accounts, they function pretty similar to bank accounts) and do not charge any monthly fees. They are both very useful for currency conversion (Revolut is better). On Assetz Capital the currency is GBP. On the other marketplaces it is EUR. Mintos has additional currencies. Transferwise borderless is available in all US states except Hawaii and Nevada. Revolut* is currently rolling out the service in the US.

Mentioned new customer cashbacks were correct at the time of the publication of this article. If you are reading the article at a later time, it may have changed. A current list of cashback offers is here.

Assetz Capital

Assetz Capital* is a marketplace for UK SME and property development loans. The liquid ‘access’ products offer 4.1% to 5.75% interest. Other product types offer higher rates. US investors are welcome. UK bank is account required – see notes above. US companies are eligible, but verification might take longer than for individuals. Expect 1-10 days for company registration.

Assetz Capital cashback for new investors: 50-250 GBP (dependent on investment amount; minimum 1000 GBP). To get it just register using this link: Assetz Capital registration and start lending

Bondora

Bondora* is an Estonian p2p lending marketplace for consumer loans. The highly liquid Go&Grow product offer yields 6.75%. With other products higher yields of 10+% are achievable. US investors need to be accredited investors to use Bondora. A bank account in the European Union is not necessary. US companies are eligible to invest. Bondora recommends that interested US investors and companies contact them at investor@bondora.com or by phone at +44 1568 6300 06 (during business hours, Mo-Fr: 9–17 EET) to check eligibility and clear any questions concerning registration.

Bondora cashback for new investors: 5 EUR, to get it just register using this link: Bondora registration and start lending

Estateguru

Estateguru* is an Estonian marketplace for property loans. Typical interest rates are 10-12%. US residents are eligible, if they have a bank account in the EEA (European Economic Area) – see notes above. US companies can invest, if they have a bank account in the EEA.

Estateguru cashback for new investors: 0.5% (1% in October) cashback on all investments in the first 3 months. To get it just register using this link: Estateguru registration and start lending

Flender

Flender* is an Irish marketplace for SME loans. Typical interest rates are around 10%. US investors and US companies are eligible.

Flender cashback for new investors: 5% on all investments in the first 30 days after signup. Register using this link Flender registration and start lending

Mintos

Mintos* is a Latvian p2p lending market place. A wide range of loan types is offered. The fairly liquid ‘Invest&Access’ product currently promotes around 8% rate. Yields of 10+% are possible with manual and autoinvest.

US investors and US companies are welcome. A bank account in the EEA (European Economic Area is required) – see notes above.

Mintos cashback for new investors: 1% cashback on all investments in the first 90 days. To get it just register using this link: Mintos registration and start lending

The article was updated on Nov. 21st as Estateguru has meanwhile changed its position saying that Revolut or Transferwise are sufficient now to satisfy the requirements on a bank account in the European Union.

P2P lending bears high risks, including total loss of investment. This article is not investment advice.

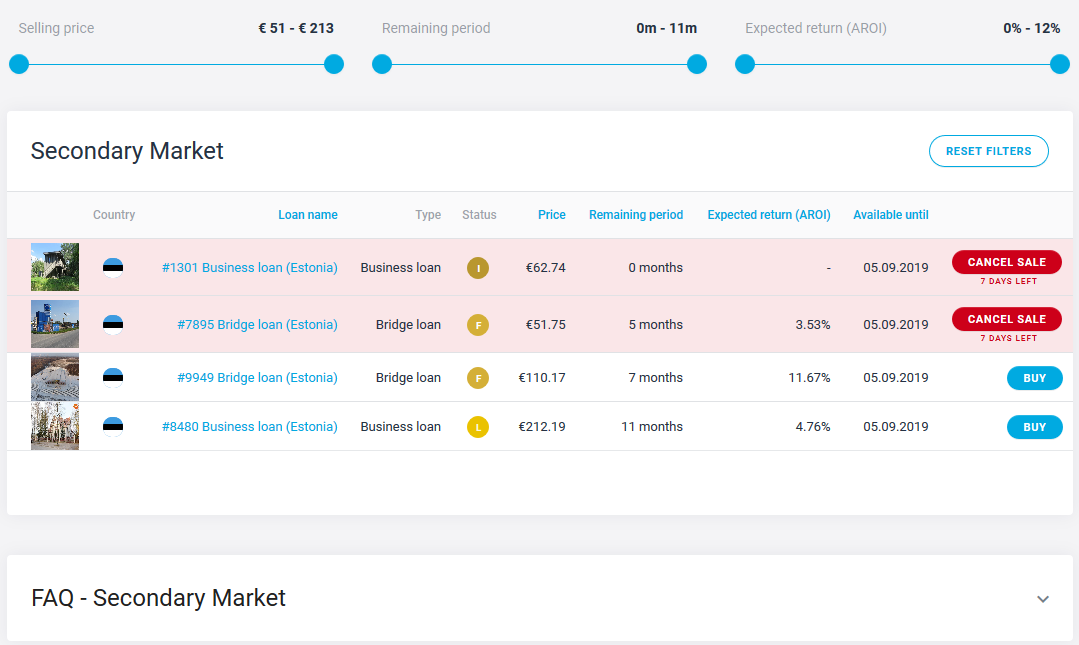

After several month of waiting since the first announcement, the Estateguru* secondary market will now launch. In the past weeks could participate in a closed beta test prior to the coming public launch of the market. Estateguru used this to get some feedback and to fine tune the wording (e.g. in the FAQ).

Overview of important facts about the Estateguru secondary market:

seller pays a 2% transaction fee

loans in all status can be offered, including late and in default

only the total loan part can be offered, it is not possible to split it and sell parts of it

seller can set the price at par or at premium. Discounts are not possible

buyer gets all repayments and interest after the sales transaction date

bought loans can not be resold for the next 30 days

each listing runs for 7 days. Unsold parts will be removed automatically

And now, without further ado, this is how the secondary market looks:

Fig. 1: Estateguru secondary market

On top of fig. 1 you can see the available filters. Also most columns can be used for sorting. The red highlighted loans are parts I listed for sale. I’ll now show you the steps necessary to sell a loan.

First I consented to this notice for activating the secondary market.

Fig. 2: Activating the secondary market

Then I went to my portfolio, selected the loan, I wanted to sell and clicked the “Sell” button on the right. Now I got to this screen:

Fig. 3: Setting the sales price

There is a slider on the upper right for the sales price. It is preset to 2% premium, to recover the sales fee. I set a higher premium here. Below the price the AROI for me (the seller) and the AROI for the buyer is shown. As the AROI is prominently featured in the market overview (see fig. 1) it is an important criteria for the buyer. And 3.56% is probably to low to achieve a sale. In fact this part did not sell in the 7 days (the other listed part #1301 did sell, see Fig 5.).

Here is the Estateguru AROI definition: ‘AROI (annualised return on investment) is an estimated annual return based on the total return on investment’.

After I clicked “Sell my claim” there is a screen for entering the password.And after that a display where Estateguru confirms that the loan is listed for sale

Fig 4.: Email I received notifying me of a successful sale of a loan

I like the overview table of the secondary market. As improvements I suggest to display the premium percentage and to allow filtering by status. Maybe that will be added in the next release. I also asked if they could add the ability to trade at discounts. The reply was that they wanted to offer an easy opportunity to sell loans and not overcomplicate the tool.

My first impression

The secondary market delivers what it aims to do: allow an early exit by selling loans. The 2% fee is relatively high, I expect that will keep the traded volume low. Sellers of late and defaulted loans will have to carefully consider the price set, as I think that with any positive news updates on the recovery status of the loan, the loan part will be bought, before the seller has a chance to read and react to the update.

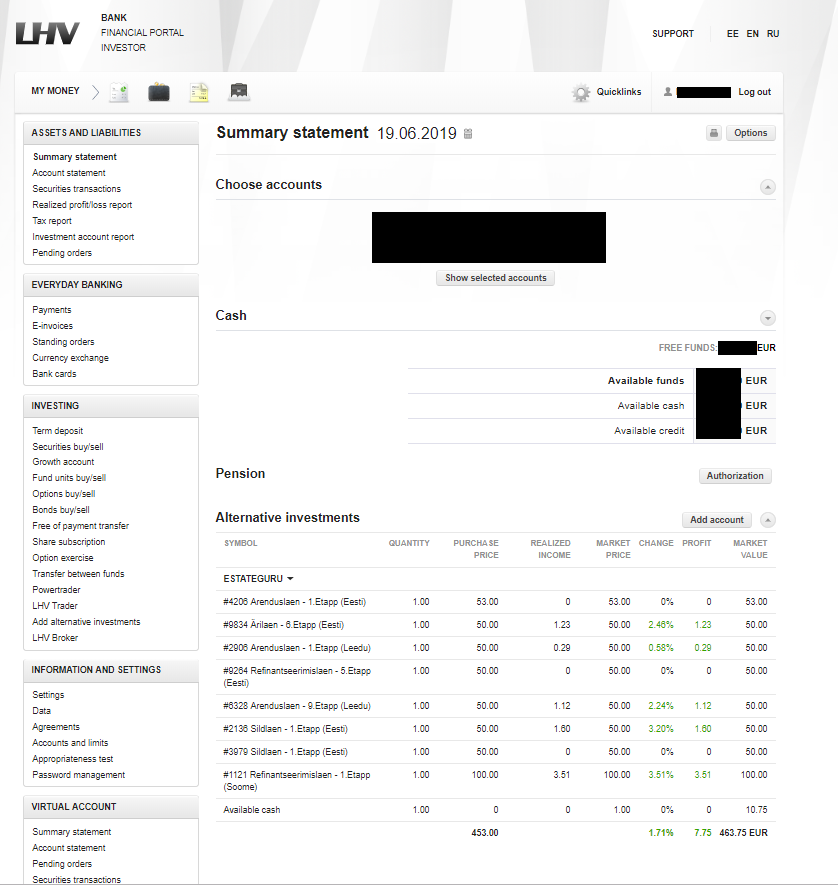

Who? What? You might wonder why that is relevant as most readers are unlikely to be LHV Bank customers. LHV Bank is a bank in Estonia.

I think it is highly interesting, as it is – to my knowledge – the first time a bank has integrated p2p lending investments in its customer interface. So the LHV bank customers, not only see their accounts and stock depots, but also their Estateguru* investments conveniently listed in their online bank dashboard. Much has been talked about what role could banks have in p2p lending (mere transaction banks? providing credit lines?) and also there is a lot of speculation if PSD2 (open banking) will help fintechs to seize the access to the customer from banks because they could control the user interface in the future. But this is actually a first step a bank takes in the opposite direction. By aggregating “non-bank” information inside the dashboard, they aim to make the banking interface more useful for the customers.

(Source: Estateguru)

Press release:

LHV customers can now see their short term property loan investments on LHV internet bank. On the summary view of internet bank, besides public stock exchange investments, one can see also alternative investments like short term property loan investments and cryptocurrencies, thus making it possible to get a quick and comprehensive overview of one’s investment portfolio. EstateGuru and Coinbase are the very first services to be switched on to the platform.

“LHV’s new service is the best example of cooperation between banks and fintech. LHV is most definitely a trendsetter in the banking sector. It is fulfilling to see that short term property lending has become a solid part of investments, and traditional banking has accepted it. EstateGuru has more than 25 000 investors throughout Europe, and the number is rapidly growing among both retail, professional, and institutional investors. We can provide our customers with more added value via interfaces like that of LHV’s “, commented EstateGuru’s COO Mihkel Stamm.

Alternative investments have become a substantial part of the Estonian investment scene, particularly among new investors. There are more than 13 000 people in Estonia who have invested in crowdfunding platforms. The fixed rate of return on debt instruments and access to the new and attractive asset classes have found their well-deserved place in investors’ portfolios. The better the quality of information, the more successful the investors.

“LHV aims to keep pace with its customers’ investment activities and that’s why we decided to take a step closer to the universe of alternative investments. The added value of this new service for our customer is a better and more comprehensive overview of the assets, thus making the portfolio management more successful “, added the Head of Investment Services at LHV, Martin Mets.

About EstateGuru

EstateGuru is the leading European platform connecting an international community of investors and businesses offering the highest diversification options for investors and flexible terms and speed of funding for businesses. The mission of EstateGuru is to provide hassle-free and flexible financing to property developers and entrepreneurs as well as diversified property backed cross-border investment opportunities to its international investor base—from the small individual investors to the institutions and everyone in-between. EstateGuru has more than 25 000 investors from 45 countries and the total money lent to date is more than 122MEUR. …

About LHV

LHV is the largest domestic financial group in Estonia. LHV’s mission is to help to create Estonian capital. According to LHV’s vision, the people and enterprises of Estonia dare to think big, start things and invest in the future. LHV’s values are to be simple, supportive and effective.