Prosper.com announced today, that Prosper founder and CEO Chris Larsen moved from the role of CEO and Chairman to serve exclusively as Chairman. He will be replaced by Dawn Lepore, who previously served as CEO and chairman of Drugstore.com. Lepore will serve as interim CEO. Larsen said:

“As Prosper continues to achieve incredible growth, now is the time to embrace the next phase of the company’s evolution. As Chairman, I look forward to working closely with the executive team to build a truly innovative consumer credit company.”

Lepore led Drugstore.com from 2004 until its successful sale to Walgreens in 2011. During her tenure, Lepore repositioned the company to focus on over-the-counter, beauty, and vision business segments.

Prior to Drugstore.com, Lepore held positions at The Charles Schwab Company. In her 21-year tenure, Lepore played a key role in launching and building the firm’s highly successful e-commerce business. Lepore also served as Schwab’s CIO, a member of Schwab’s Executive Committee, and a trustee of Schwab Funds, among other executive roles.

Lepore currently serves on the board of eBay, Inc., and was appointed on Feb.23rd to Coupons.com Inc. board of directors.

The following video was produced by Elektrischer Reporter for German TV ZDF. The elaborate production is different from most other TV coverage I have seen, as it does not focus on one platform but rather tries to grasp the concept of p2p lending as a whole.

Furthermore it differs by the eye-catching make. But see for yourself:

Unfortunately it is available in German language only.

Prosper.com has reopened – now with the long sought approval of the SEC which was granted last Friday. In his blog statement “We mean it this time!” CEO Chris Larsen sheds light on what was delaying SEC approval. It was auction bidding on loan requests:

… the first Internet auction-based P2P loans marketplace and trading platform to have its SEC registration declared effective, which means the SEC is permitting Prosper to facilitate auctions in a way that has never been done before.

Selling securities by auction is not new and critical to greater efficiency in fair price discovery for both sides of the transaction. However, the SEC has never permitted Wall Street investment banks or any other institution to run a true auction where investors could make an irrevocable bid that committed funds prior to the establishment of a final rate….

Prosper introduces a secondary market. The internet auction priced trading platform for Prosper Notes is operated by FolioFN (like Lending Club’s Note Trading platform). Only loans (‘notes’) issued after July 13th can be traded.

At the moment lenders from California, Colorado, Delaware, Georgia, Illinois, Minnesota, Montana, Nevada, New York, South Carolina, South Dakota, Utah, Wisconsin and Wyoming can use Prosper, if they fulfill state set financial suitability requirements. Prosper is open to borrowers from almost all states.

With the PR Prosper will likely build up a large selection of loan listings again fast (as of now there are 10). The interesting question will be if Prosper lenders will continue to have faith investing via Prosper after extremely high default rates and low collection results in the past. Furthermore disappointed (former) long term lenders are critisizing risks for lenders embedded in the latest SEC filing.

With the likely press coverage of the relaunch all p2p lending companies in the US can expect to see a rise in traffic.

Prosper.com has restarted offering p2p lending to customers after an SEC imposed 6 months stop (quiet period).

Prosper chief executive Chris Larsen said the California Department of Corporations has authorized the company to resume raising money in California and then lending it out under a system that lets borrowers and lenders use bids to set the interest rates on loans. “I hope this leads to wider acceptance of peer-to-peer lending,” said Commissioner of Corporations Preston DuFauchard. He said the state’s experience with Prosper, prior to the SEC intervention, made it “comfortable” that its bidding system gives lenders the information they need to invest in loans wisely.

Prosper hopes to reopen for lenders from other states but it remains uncertain when Prosper will be allowed to do so.

Prosper raises the minimum credit score required to 640 (Grade C under the old rating). This applies only to new borrowers. Borrowers registered before the quiet period that have lower credit grades can still apply for second loans (example: loan listing of a HR borrower).

Besides “direct” p2p loan listings, Prosper offers “Open Market Listings“, which are described as following:

Open Market loans are existing loans that were underwritten by financial institutions that are credit experts in areas such as auto loans, small business loans or social impact loans. The loan seller describes the loan in an Open Market listing, and then sells and assigns the loan to Prosper.

Open Market loans may include existing consumer loans or retail installment sale contracts. They can be secured or unsecured loans, and may include small business loans, where the borrower is a business entity, not an individual.

Open Market listings describe the existing Open Market loan, owned by the loan seller, which is offered for sale on the Prosper marketplace. Each listing displays information to assist the lender in making an informed bidding decision. Lenders can review the sale price for the Open Market loan, the yield percentage that corresponds to the sales price, the remaining principal balance of the loan and the interest rate the borrower is obligated to pay on the loan.

In some instances on auto loans, you can even see the factory where the car was built. This is all part of the transparency Prosper brings to the marketplace so that you can make informed decisions on how to invest your money.

Prosper plans a secondary market which in future will allow lenders to trade notes.

We’ll be using this blog to create a place to find up-to-the-minute news on the latest Prosper enhancements, enlightening and thoughtful Personal Finance opinions, touching Prosper Member Stories, and more. Your contributions are welcome. Please feel free to submit comments to any of the blog posts or send new articles and ideas to us at blog @ prosper.com (please remove spaces before using this email address) or submit a guest post.

We’ll be adding in posts regularly, so please stop back in again soon.

Warmly,

Prosper

The blog has been in preparation for some time. I believe we can look forward to some interesting articles by Prosper staff, borrowers, lenders and other guest writers.

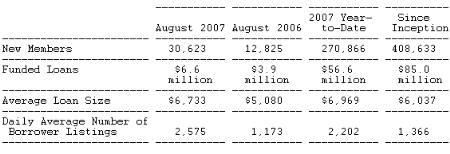

Prosper.com published a "People to People Lending Market Survey" for August. The Survey covers Prosper data and gives a commentary by Chris Larsen, CEO of Prosper.

In the commentary the main point is the focus of lenders on higher credit categories: "…At the same time, lenders on Prosper are exhibiting rational behavior by steering their bids toward borrowers in the higher credit categories and being far more cautious about chasing higher rates offered by subprime borrowers. Evidence of this flight to safety is seen in Prosper's mix of funded borrowers. For example, the subprime category accounted for only 9 percent of loans funded in August 2007, a marked decrease from August 2006 and the 2007 year-to-date average of 25 percent and 14 percent, respectively. What remains to be seen is whether lenders on Prosper will start placing less weight on homeownership as a factor in their bidding strategies…"

When studying the figures careful attention should be given to the definitions. HR loans are completely excluded from the Estimated Annual Return on Prosper Select Index and the Average Borrower Rates on Prosper Select Loans table. Furthermore loans that did not fit criteria on delinquincies, credit inquiries and DTI are also not included in these tables.